|

시장보고서

상품코드

1685090

의료 기기 검사 서비스 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Medical Devices Testing Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

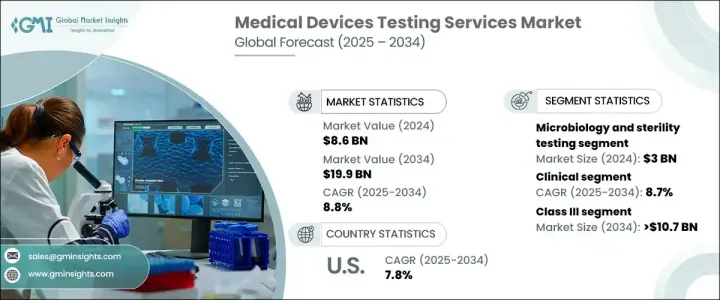

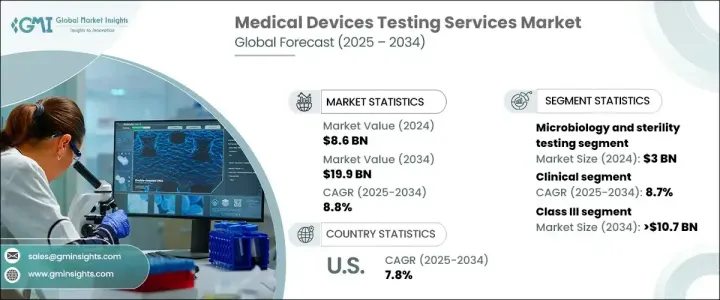

의료 기기 검사 서비스 세계 시장은 2024년에 86억 달러로 평가되었으며, 2025년부터 2034년에 걸쳐 8.8%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측되고 있습니다.

이러한 성장은 의료기기의 안전성, 성능 및 효능을 보장하는 엄격한 규제 요건을 충족할 필요성이 증가하는 것이 주요 요인입니다. 헬스케어 기술의 끊임없는 혁신과 함께 종합적이고 엄격한 테스트 서비스에 대한 수요는 그 어느 때보다도 필수적입니다. 의료기기 제조업체는 국제 규제 기준을 준수하고 비용이 많이 드는 제품 리콜 및 안전 문제를 피하기 위해 시험을 선호합니다. 웨어러블, 임베디드 기술, 진단 도구 등 의료기기의 복잡성이 증가함에 따라 고급 테스트 방법에 대한 필요성도 커지고 있습니다. 임상시험이나 전임상시험, 미생물검사를 통해 안전성과 유효성을 확보할 필요성은 앞으로도 시장의 미래를 형성해 나갈 것으로 보입니다.

다양한 검사 서비스 중 미생물 검사와 무균 검사가 2024년 시장을 독점하여 30억 달러를 창출했습니다. 이 서비스는 미생물 오염 감지 및 멸균 기술 검증에 필수적이며 장비가 안전 기준을 충족하는지 확인하는 데 매우 중요합니다. 의료시설에서의 감염 관리의 중시의 고조가 이러한 서비스 수요를 더욱 끌어 올리고 있습니다. 건강관리 관련 감염이 여전히 가장 큰 관심사임을 감안할 때, 무균 검사의 요구는 앞으로도 상승 기조를 계속할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 86억 달러 |

| 예측 금액 | 199억 달러 |

| CAGR | 8.8% |

의료 기기 검사 서비스 시장은 임상시험과 전임상시험에도 구분됩니다. CAGR 8.7%로 성장이 예상되는 임상시험 분야는 2034년까지 131억 달러에 달할 것으로 예측되고 있습니다. 임상시험은 의료기기의 안전성과 유효성을 실제 조건 하에서 검증하고 규제와 시장 기대를 모두 충족시키는 데 필수적입니다. 의료 기술이 발전함에 따라 임상시험은 웨어러블 및 임플란트와 같은 장비의 사용 편의성, 생체 적합성 및 전반적인 안전성을 평가하는 데 더욱 중요해지고 있습니다. 이러한 장비의 복잡성이 증가함에 따라, 특히 인체에 원활하게 통합되는 새로운 기술 혁신에서는 임상 평가에 보다 상세한 접근이 요구됩니다.

미국의 의료 기기 검사 서비스 시장은 2024년에 22억 달러의 수익을 올렸으며, 2025년부터 2034년에 걸쳐 CAGR 7.8%로 성장할 것으로 예상되고 있습니다. 북미는 첨단 건강 관리 인프라와 강력한 규제 체제를 배경으로 세계 시장에서 우위를 유지하고 있습니다. 이 지역은 FDA와 같은 규제기관의 네트워크가 확립되어 있어 의료기기의 최고의 안전성과 품질기준을 확보하기 위해 종합적인 시험 프로토콜을 실시했습니다. 이 엄격한 규제 상황과 연구 개발 및 시험 서비스에 대한 상당한 투자가 결합되어 북미는 의료기기 시험의 중심지가 되었습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 엄격한 승인 기준에 대한 주목 증가

- 의료기술의 일관된 급속한 진보

- 의료기기의 검증과 타당성 확인에 대한 요구 증가

- 업계의 잠재적 위험 및 과제

- 숙련된 전문가와 시험시설의 부족

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

- 밸류체인 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 서비스별, 2021년-2034년

- 주요 동향

- 미생물 검사와 무균 검사

- 항균 시험

- 파이로젠 및 엔도톡신 시험

- 무균시험과 밸리데이션

- 바이오바덴 측정

- 기타 미생물학 및 무균시험

- 생체 적합성 시험

- 화학시험

- 패키지 밸리데이션

제6장 시장 추정 및 예측 : 페이즈별, 2021년-2034년

- 주요 동향

- 임상시험

- 전임상

제7장 시장 추정 및 예측 : 디바이스 클래스별, 2021년-2034년

- 주요 동향

- 클래스 III

- 클래스 II

- 클래스 I

제8장 시장 추정 및 예측 : 모드별, 2021년-2034년

- 주요 동향

- 아웃소싱

- 인하우스

제9장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 의료기기 제조업체

- 임상연구기관(CRO)

- 학술기관 및 연구기관

- 기타 최종 사용자

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- charles river

- element

- eurofins

- intertek

- labcorp

- NAMSA

- Pace

- SGS

- Sterigenics

- TUV SUD

- WuXiAppTec

The Global Medical Devices Testing Services Market, valued at USD 8.6 billion in 2024, is projected to grow at a robust CAGR of 8.8% from 2025 to 2034. This growth is largely driven by an increasing need to meet stringent regulatory requirements that ensure medical devices' safety, performance, and efficacy. With continuous innovations in healthcare technology, the demand for comprehensive and rigorous testing services is more essential than ever. Medical device manufacturers are prioritizing testing to comply with international regulatory standards and avoid costly product recalls or safety issues. As the complexity of medical devices such as wearables, implantable technologies, and diagnostic tools rises, so does the need for advanced testing methods. The need to ensure safety and effectiveness through clinical and preclinical trials, as well as microbiological testing, will continue to shape the future of the market.

Among the various testing services, microbiology and sterility testing dominated the market in 2024, generating USD 3 billion. This service is critical in detecting microbial contamination and validating sterilization techniques, which is crucial for ensuring that devices meet safety standards. The growing emphasis on infection control in healthcare facilities further drives the demand for these services. Given that healthcare-associated infections remain a top concern, the need for sterility testing is expected to continue its upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.6 Billion |

| Forecast Value | $19.9 Billion |

| CAGR | 8.8% |

The medical devices testing services market is also segmented into clinical and preclinical testing. The clinical testing segment, which is expected to grow at a CAGR of 8.7%, is projected to reach USD 13.1 billion by 2034. Clinical trials are essential for validating the safety and efficacy of medical devices under real-world conditions, ensuring they meet both regulatory and market expectations. As medical technology advances, clinical testing is becoming even more critical in assessing the usability, biocompatibility, and overall safety of devices like wearables and implants. The increasing complexity of these devices requires a more detailed approach to clinical evaluations, especially with newer innovations that integrate seamlessly into the human body.

The U.S. medical devices testing services market garnered USD 2.2 billion in 2024 and is expected to grow at a CAGR of 7.8% from 2025 to 2034. North America, driven by its advanced healthcare infrastructure and strong regulatory framework, remains a dominant player in the global market. The region benefits from a well-established network of regulatory bodies, such as the FDA, that enforce comprehensive testing protocols to ensure the highest safety and quality standards for medical devices. This rigorous regulatory landscape, combined with considerable investments in R&D and testing services, makes North America a hub for medical devices testing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing focus on strict approval norms

- 3.2.1.2 Consistent and rapid advancements in medical technologies

- 3.2.1.3 Rising need for verification and validation of medical devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals and testing facilities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Services, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Microbiology and sterility testing

- 5.2.1 Antimicrobial testing

- 5.2.2 Pyrogen and endotoxin testing

- 5.2.3 Sterility test and validation

- 5.2.4 Bioburden determination

- 5.2.5 Other microbiology and sterility testings

- 5.3 Biocompatibility tests

- 5.4 Chemistry test

- 5.5 Package validation

Chapter 6 Market Estimates and Forecast, By Phase, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical

- 6.3 Preclinical

Chapter 7 Market Estimates and Forecast, By Device Class, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Class III

- 7.3 Class II

- 7.4 Class I

Chapter 8 Market Estimates and Forecast, By Mode, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Outsourced

- 8.3 In-house

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Medical device manufacturers

- 9.3 Clinical research organizations (CROs)

- 9.4 Academic and research institutions

- 9.5 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 charles river

- 11.2 element

- 11.3 eurofins

- 11.4 intertek

- 11.5 labcorp

- 11.6 NAMSA

- 11.7 Pace

- 11.8 SGS

- 11.9 Sterigenics

- 11.10 TUV SUD

- 11.11 WuXiAppTec