|

시장보고서

상품코드

1685179

죽상 절제술 기기 시장 : 기회, 성장 촉진요인, 산업 동향 분석(2025-2034년)Atherectomy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

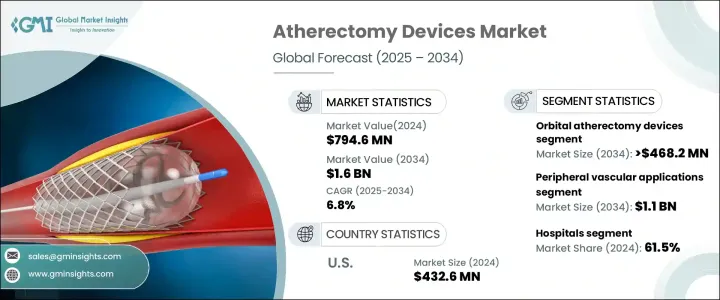

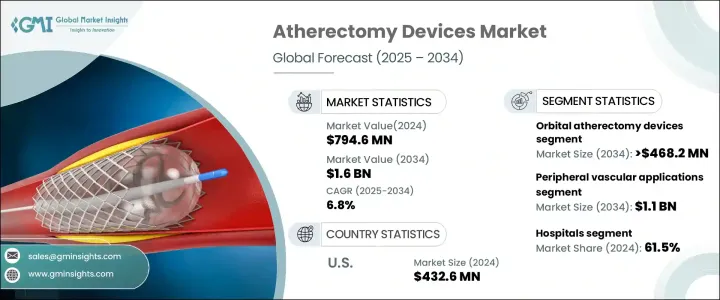

세계의 죽상 절제술 기기 시장은 2024년에 7억 9,460만 달러에 이르렀으며, 2025년부터 2034년까지 연평균 성장률(CAGR) 6.8%로 성장할 것으로 예측됩니다.

말초동맥질환(PAD)과 관상동맥질환(CAD)의 유병률이 증가함에 따라 첨단 치료 솔루션에 대한 수요가 증가하고 있습니다. 고령화 인구가 증가하고 앉아서 생활하는 라이프스타일이 보편화되면서 당뇨병과 비만 환자가 급증하고 있어 최소 침습 시술에 대한 필요성이 더욱 커지고 있습니다. 의료 서비스 제공업체는 플라크 제거를 강화하는 동시에 합병증을 최소화할 수 있는 정밀한 솔루션을 찾고 있으며, 죽상 절제술 기기는 심혈관 치료의 필수 도구가 되고 있습니다.

환자 중심의 의료 서비스로의 전환이 증가함에 따라 병원과 의료 센터는 임상 결과를 개선하는 기술을 채택하고 있습니다. 최소 침습적 죽상 절제술은 기존 치료 방법에 비해 회복 시간이 빠르고 입원 기간이 짧으며 수술 후 합병증 위험이 낮습니다. 이러한 변화는 의사와 환자들 사이에서 더 많은 채택률을 높이고 있습니다. 지속적인 기술 발전, 규제 승인, 진행 중인 임상시험으로 인해 이러한 기기에 대한 신뢰가 강화되고 있으며, 더 폭넓게 도입될 수 있는 기반을 마련하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 9,460만 달러 |

| 예측 금액 | 16억 달러 |

| CAGR | 6.8% |

또한 연구 개발에 대한 투자가 증가하면서 시장이 확대되고 있습니다. 기업들은 뛰어난 효율성, 정밀성, 안전성을 제공하는 혁신적인 죽상 절제 시스템을 도입하고 있습니다. 임상의가 시술 시간을 줄이면서 치료 방법을 최적화할 수 있는 자동화 및 AI 통합 기기가 등장하고 있습니다. 우호적인 환급 정책과 외래 환자 심혈관 시술의 증가는 시장 성장을 더욱 촉진하고 있습니다. 의료 기관이 높은 성공률을 제공하는 비용 효율적인 솔루션을 우선시함에 따라 죽상 절제술 기기는 계속해서 탄력을 받고 있습니다.

제품 유형별로 시장은 궤도, 레이저, 방향성 및 회전식 죽상 절제술 기기로 세분화됩니다. 궤도형 죽상 절제술 기기는 상당한 성장세를 보이며 2034년까지 시장 가치가 6.6%의 연평균 성장률로 4억 6,820만 달러에 달할 것으로 예상됩니다. 이러한 장치는 고속 회전 크라운 또는 버를 사용하여 동맥의 완전성을 보존하면서 플라그를 제거함으로써 시술 정확도를 향상시킵니다. 말초 및 관상동맥 치료에서 일관된 성공을 거두면서 복잡한 케이스를 관리하는 의료 전문가들 사이에서 선호되는 선택으로 자리 잡았습니다. 병원과 수술 센터가 혁신적이고 효율적인 치료 옵션을 우선시함에 따라 궤도 동맥 절제술 기기에 대한 수요는 계속 증가하고 있습니다.

용도별로 보면 시장은 말초 혈관 및 관상동맥 시술로 나뉩니다. 말초 혈관 부문은 크게 확대될 것으로 예상되며, 2034년까지 6.3%의 연평균 성장률로 11억 달러에 달할 것으로 예상됩니다. 말초동맥 질환은 이동성과 삶의 질에 심각한 영향을 미치기 때문에 효과적인 치료 대안이 절실히 필요합니다. 죽상 절제술은 기존 수술에 비해 회복 기간 단축, 합병증 감소, 입원 기간 단축 등 주목할 만한 이점을 제공합니다. 이러한 이점에 대한 인식이 높아지면서 더 많은 환자와 의료진이 최소 침습적 시술을 선택하고 있으며, 이에 따라 죽종 절제술 기기에 대한 수요도 증가하고 있습니다.

미국의 죽상 절제술 기기 시장은 2024년에 4억 3,260만 달러를 차지하며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 6.2%로 성장할 것으로 예측됩니다. PAD 및 CAD를 포함한 심혈관 질환의 부담이 증가함에 따라 첨단 치료 솔루션에 대한 수요가 증가하고 있습니다. 노인 인구의 증가와 높은 비만 및 당뇨병 비율은 시장 성장을 더욱 가속화하고 있습니다. 의료 기관에서는 시술의 정밀도를 높이고 환자의 안전을 개선하며 빠른 회복을 보장하는 최첨단 죽상 절제술 기기를 점점 더 많이 도입하고 있습니다. 최소 침습적 심혈관 시술에 대한 수요가 증가함에 따라 미국 시장은 전 세계에서 지배적인 위치를 유지할 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 최소 침습 시술에 대한 선호도 증가

- 대상 환자 인구 증가

- 최근 기술 발전

- 말초 동맥 질환의 유병률 증가

- 업계의 잠재적 위험 및 과제

- 제품의 높은 비용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 상환 시나리오

- 기술 상황

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

- 밸류체인 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 궤도 죽상 절제술 기기

- 레이저 죽상 절제술 기기

- 방향성 죽상 절제술 기기

- 회전식 죽상 절제술 기기

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 말초 혈관

- 관상 동맥

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 최종 사용자

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott

- angiodynamics

- AVINGER

- B. Braun

- BD(Becton, Dickinson and Company)

- BIOMERICS

- Boston Scientific

- Cardinal Health

- Cardiovascular Systems

- Cordis

- Philips

- Medtronic

- Nipro

- Rex Medical

- TERUMO

The Global Atherectomy Devices Market reached USD 794.6 million in 2024 and is projected to grow at a CAGR of 6.8% between 2025 and 2034. The rising prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD) is fueling demand for advanced treatment solutions. As aging populations increase and sedentary lifestyles become more common, cases of diabetes and obesity are surging, further driving the need for minimally invasive procedures. Healthcare providers are seeking precision-driven solutions to enhance plaque removal while minimizing complications, making atherectomy devices an essential tool in cardiovascular treatment.

The increasing shift toward patient-centric healthcare is pushing hospitals and medical centers to adopt technologies that improve clinical outcomes. Minimally invasive atherectomy procedures offer faster recovery times, reduced hospital stays, and lower risks of post-surgical complications compared to traditional treatment methods. This shift is encouraging higher adoption rates among physicians and patients. Continuous technological advancements, regulatory approvals, and ongoing clinical trials are strengthening confidence in these devices, paving the way for their broader implementation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $ 794.6 Million |

| Forecast Value | $ 1.6 Billion |

| CAGR | 6.8% |

Market expansion is also being driven by growing investment in research and development. Companies are introducing innovative atherectomy systems that provide superior efficiency, precision, and safety. Automated and AI-integrated devices are emerging, allowing clinicians to optimize treatment approaches while reducing procedure times. Favorable reimbursement policies and an increasing number of outpatient cardiovascular procedures are further propelling market growth. As medical institutions prioritize cost-effective solutions that deliver high success rates, atherectomy devices continue to gain momentum.

By product type, the market is segmented into orbital, laser, directional, and rotational atherectomy devices. Orbital atherectomy devices are set to experience substantial growth, with market value expected to reach USD 468.2 million by 2034 at a CAGR of 6.6%. These devices improve procedural accuracy by utilizing a high-speed spinning crown or burr to remove plaque while preserving arterial integrity. Their consistent success in treating both peripheral and coronary arteries has positioned them as a preferred choice among healthcare professionals managing complex cases. As hospitals and surgical centers prioritize innovative and efficient treatment options, the demand for orbital atherectomy devices continues to rise.

Based on application, the market is divided into peripheral vascular and coronary procedures. The peripheral vascular segment is expected to expand significantly, projected to reach USD 1.1 billion by 2034 at a CAGR of 6.3%. Peripheral artery disease severely impacts mobility and quality of life, creating an urgent need for effective treatment alternatives. Atherectomy procedures offer notable advantages, including reduced recovery periods, fewer complications, and shorter hospital stays compared to traditional surgery. As awareness of these benefits grows, more patients and healthcare providers are opting for minimally invasive interventions, boosting the demand for atherectomy devices.

The U.S. atherectomy devices market accounted for USD 432.6 million in 2024 and is anticipated to grow at a CAGR of 6.2% from 2025 to 2034. The country's increasing burden of cardiovascular diseases, including PAD and CAD, is driving demand for advanced treatment solutions. A growing elderly population, coupled with high obesity and diabetes rates, is further accelerating market growth. Medical institutions are increasingly adopting cutting-edge atherectomy devices that enhance procedural precision, improve patient safety, and ensure faster recoveries. As the demand for minimally invasive cardiovascular procedures rises, the U.S. market is expected to maintain its dominant position in the global landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in preference for minimally invasive procedures

- 3.2.1.2 Growing target patient population

- 3.2.1.3 Recent technological advancements

- 3.2.1.4 Rising prevalence of peripheral arterial diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Orbital atherectomy devices

- 5.3 Laser atherectomy devices

- 5.4 Directional atherectomy devices

- 5.5 Rotational atherectomy devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Peripheral vascular applications

- 6.3 Coronary applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 angiodynamics

- 9.3 AVINGER

- 9.4 B. Braun

- 9.5 BD (Becton, Dickinson and Company)

- 9.6 BIOMERICS

- 9.7 Boston Scientific

- 9.8 Cardinal Health

- 9.9 Cardiovascular Systems

- 9.10 Cordis

- 9.11 Philips

- 9.12 Medtronic

- 9.13 Nipro

- 9.14 Rex Medical

- 9.15 TERUMO