|

시장보고서

상품코드

1685209

태키파이어 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Tackifier Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

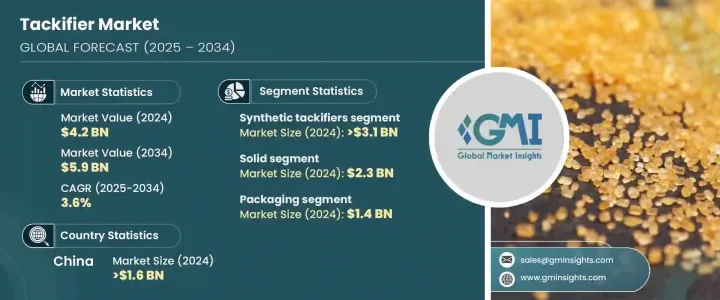

세계의 태키파이어 시장은 2024년에 42억 달러로 평가되었고, 2025-2034년 CAGR 3.6%로 확대될 것으로 예측되며 꾸준한 성장이 전망되고 있습니다.

태키파이어(점착부여제)는 점착성을 높이고 다양한 산업에서 접착성을 향상시킴으로써 접착제 배합에 중요한 역할을 하고 있습니다. 특히 패키징, 자동차, 건축 및 위생 분야에서 고성능 접착제 수요 증가에 따라 첨단 태키파이어 솔루션의 요구가 높아지고 있습니다. 이 시장에서는 특히 부직포 위생 용품과 연포장에 있어서 핫멜트 접착제(HMA) 수요가 급증하고 있어 업계의 확대를 더욱 뒷받침하고 있습니다.

시장 성장의 주요 촉진요인은 접착 기술의 지속적인 발전과 환경 친화적인 솔루션으로의 변화 증가를 포함합니다. 산업계가 점점 지속가능성을 우선시함에 따라 바이오의 태키파이어로의 전환이 가속화되고 있습니다. 재생가능한 자원으로부터 유래된 이러한 대안은 휘발성 유기화합물(VOC)의 배출량이 적고 엄격한 환경규제 준수를 목표로 하는 기업들에게 선호되는 옵션이 되었습니다. 게다가 전자상거래의 급속한 확대 및 효율적인 포장용 접착제에 대한 요구가 증가함에 따라 세계적으로 수요가 증가하고 있습니다. 자동차 조립 및 의료용 등 접착제의 성능이 중요한 산업에서는 태키파이어가 우수한 접착 능력을 발휘하여 현대 제조업에 필수적인 역할을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 42억 달러 |

| 예측 금액 | 59억 달러 |

| CAGR | 3.6% |

2024년에 31억 달러로 평가된 합성 태키파이어 분야가 시장을 독점하였고, 예측 기간의 CAGR은 3.5%로 예측됩니다. 지방족 탄화수소, C9 방향족, 합성 폴리테르펜과 같은 석유 기반 원료로부터 얻은 합성 태키파이어는 우수한 열 안정성, 강력한 접착 특성, 다양한 태키파이어와의 상용성으로 널리 지지됩니다. 포장, 건축, 자동차 등의 업계에서는 가혹한 조건 하에서의 내구성과 효율성으로 인해 이러한 태키파이어에 큰 신뢰를 갖고 있습니다. 고온 및 다양한 환경 조건 하에서도 점착력을 유지할 수 있기 때문에 오래 지속되는 점착 솔루션을 요구하는 제조업체에게 최선의 선택이 되고 있습니다.

견고한 태키파이어 부문은 2024년에 23억 달러를 창출하였고, 2034년까지 연평균 복합 성장률(CAGR) 3.4%로 성장할 것으로 예상됩니다. 고형 태키파이어는 비용 효율적이고 취급이 용이하며, 감압 접착제 및 핫멜트 접착제의 용도로 뛰어난 성능을 발휘하기 때문에 높은 인기가 있습니다. 강력한 폴리머 적합성과 열 안정성은 내구성과 유연한 접착 솔루션이 필요한 산업에 이상적입니다. 산업 포장 및 건축에서 위생 용품 및 자동차 용도에 이르기까지 고형 태키파이어는 진화하는 태키파이어 업계에서 기본적인 요소입니다.

중국의 태키파이어 시장은 2024년 16억 달러로 평가되었으며 2034년까지 연평균 복합 성장률(CAGR) 3.4%로 확대될 것으로 예상됩니다. 세계의 제조 강국인 중국은 강력한 산업 기반과 다양한 용도 분야에서 접착제 수요가 증가함에 따라 시장을 독점하고 있습니다. 포장, 건설, 자동차 산업의 급성장으로 인해 태키파이어의 요구가 크게 증가하고 있습니다. 게다가 중국의 전자상거래 부문의 활황이 고품질 포장용 접착제 수요를 견인해 세계 시장에서 중국의 리더십을 더욱 견고하게 하고 있습니다. 지속적인 산업화 및 인프라 개발로 중국은 태키파이어 산업의 미래를 형성하는 중요한 기업으로 남아 있습니다.

목차

제1장 조사 방법 및 조사 범위

- 시장 범위 및 정의

- 기본 추정 및 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 자료

- 유료 정보원

- 공적 정보원

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴

- 장래 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스 및 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 각 업계의 접착제 수요 증가

- 친환경 태키파이어 수요 증가

- 아시아태평양의 산업 성장

- 업계의 잠재적 위험 및 과제

- 합성 태키파이어를 제한하는 환경 규제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 합성 태키파이어

- 천연 태키파이어

제6장 시장 추계 및 예측 : 형태별(2021-2034년)

- 주요 동향

- 고체

- 액체

- 수지 분산체

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 포장

- 건축

- 부직포

- 제본

- 자동차

- 기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Arkema

- BASF SE

- Eastman Chemical

- Exxon Mobil

- HB Fuller

- Henkel AG &Co. KGaA

- Kolon Industries

- KRATON

- SI Group

- ZEON

The Global Tackifier Market reached USD 4.2 billion in 2024 and is poised for steady growth, projected to expand at a CAGR of 3.6% between 2025 and 2034. Tackifiers play a crucial role in adhesive formulations by enhancing their stickiness and improving adhesion across various industries. With the growing demand for high-performance adhesives, particularly in the packaging, automotive, construction, and hygiene sectors, the need for advanced tackifier solutions is on the rise. The market is witnessing a surge in demand for hot-melt adhesives (HMAs), particularly in nonwoven hygiene products and flexible packaging, further propelling industry expansion.

Key drivers of market growth include continuous advancements in adhesive technologies and a rising shift toward environmentally friendly solutions. As industries increasingly prioritize sustainability, the transition to bio-based tackifiers is accelerating. These alternatives, derived from renewable sources, offer lower volatile organic compound (VOC) emissions, making them a preferred choice for companies aiming to comply with stringent environmental regulations. Additionally, the rapid expansion of e-commerce and the growing need for efficient packaging adhesives are fueling demand across the globe. In industries where adhesive performance is critical, such as automotive assembly and medical applications, tackifiers provide superior bonding capabilities, reinforcing their indispensable role in modern manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 3.6% |

The synthetic tackifiers segment, valued at USD 3.1 billion in 2024, dominates the market and is projected to grow at a CAGR of 3.5% over the forecast period. Derived from petroleum-based sources such as aliphatic hydrocarbons, C9 aromatics, and synthetic polyterpenes, synthetic tackifiers are widely favored for their outstanding thermal stability, strong adhesion properties, and compatibility with various adhesives. Industries such as packaging, construction, and automotive heavily rely on these tackifiers for their durability and efficiency in extreme conditions. Their ability to maintain adhesion under high temperatures and diverse environmental conditions makes them a top choice for manufacturers seeking long-lasting adhesive solutions.

The solid tackifier segment generated USD 2.3 billion in 2024 and is expected to grow at a 3.4% CAGR through 2034. Solid tackifiers are highly sought after due to their cost-effectiveness, ease of handling, and exceptional performance in pressure-sensitive and hot-melt adhesive applications. Their strong polymer compatibility and thermal stability make them ideal for industries that require durable and flexible bonding solutions. From industrial packaging and construction to hygiene products and automotive applications, solid tackifiers continue to be a fundamental component in the evolving adhesive landscape.

China tackifier market was valued at USD 1.6 billion in 2024 and is anticipated to expand at a CAGR of 3.4% through 2034. As a global manufacturing powerhouse, China dominates the market due to its strong industrial base and rising demand for adhesives across various applications. The rapid growth of the packaging, construction, and automotive industries has significantly increased the need for tackifiers. Additionally, China's booming e-commerce sector is driving demand for high-quality packaging adhesives, further solidifying the country's leadership in the global market. With continued industrialization and infrastructure development, China remains a key player in shaping the future of the tackifier industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increased adhesive demand across industries

- 3.6.1.2 Rise in eco-friendly tackifier demand

- 3.6.1.3 Growth in Asia-Pacific’s industries

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Environmental regulations limiting synthetic tackifiers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Synthetic tackifiers

- 5.3 Natural tackifiers

Chapter 6 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid

- 6.3 Liquid

- 6.4 Resin dispersions

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Packaging

- 7.3 Construction

- 7.4 Non-woven

- 7.5 Bookbinding

- 7.6 Automotive

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Arkema

- 9.2 BASF SE

- 9.3 Eastman Chemical

- 9.4 Exxon Mobil

- 9.5 H.B. Fuller

- 9.6 Henkel AG & Co. KGaA

- 9.7 Kolon Industries

- 9.8 KRATON

- 9.9 SI Group

- 9.10 ZEON