|

시장보고서

상품코드

1698232

종이컵 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Paper Cups Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

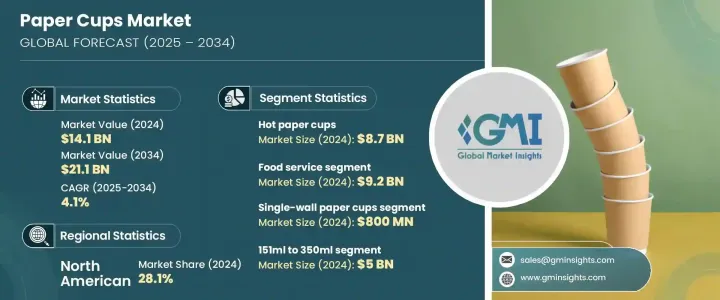

세계의 종이컵 시장은 2024년에 141억 달러로 평가되었으며, 2025-2034년 연평균 복합 성장률(CAGR) 4.1%로 성장할 것으로 예측됩니다.

이 확대에는 편리하고 휴대 가능한 음료 옵션에 대한 소비자 수요 증가 및 세계의 스페셜티 커피숍과 독립 카페의 인기 고조가 박차를 가하고 있습니다. 도시 소비자의 라이프 스타일 기호 진화 및 지속 가능성에 대한 세계의 뒷받침이, 혁신적이고 환경 친화적인 종이컵 솔루션에 대한 요구를 뒷받침하고 있습니다. 보다 많은 소비자가 장인적이고 프리미엄한 커피 체험을 요구하는 가운데, 카페나 퀵 서비스 레스토랑은 고품질의 지속 가능한 종이컵을 채용하는 것으로 대응하고 있습니다. 이러한 동향은, 환경을 배려한 패키징에 대한 업계 전체의 시프트를 반영하고 있어, 소비자의 기대와 규제 요건 양쪽 모두를 충족시키는 것을 목표로 하는 종이컵 제조업체에 유리한 기회를 낳고 있습니다.

지속가능성을 중시하게 됨으로써 기존의 플라스틱 코팅 종이컵을 대체하는 생분해성이나 퇴비화 가능한 종이컵에 대한 투자가 증가하고 있습니다. 일회용 플라스틱에 대한 정부의 규제가 강화되는 가운데, 제조업체는 환경에 대한 영향을 억제하면서 뛰어난 단열성을 제공하는 바이오 베이스나 폴리 젖산(PLA) 소재의 코팅을 한 종이컵을 적극적으로 개발하고 있습니다. 게다가 소비자의 건강 의식 고조로 화학물질을 포함하지 않고 재활용 가능한 종이컵을 선호하게 되어 다양한 최종 용도 분야에서의 수요가 더욱 높아지고 있습니다. 또한 기업들은 브랜딩과 커스터마이징의 중요성을 인식하고 있으며, 고객 인게이지먼트 및 마케팅 활동을 강화하는 인쇄된 명품 종이컵의 수요 급증으로 이어지고 있습니다. 이러한 요인들이 종합적으로 세계 종이컵 시장의 강력한 성장 궤도에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 141억 달러 |

| 예측 금액 | 211억 달러 |

| CAGR | 4.1% |

종이컵 시장은 뜨거운 종이컵과 차가운 종이컵의 두 가지 주요 범주로 나뉩니다. 2024년에는 뜨거운 종이컵 분야가 87억 달러의 매출액을 차지했으며, 커피와 홍차 등 나들이 장소에서의 뜨거운 음료 수요 급증이 그 원동력이 되고 있습니다. 도시화 및 페이스가 빠른 라이프 스타일이, 특히 퀵 서비스 레스토랑 및 카페에서의 뜨거운 음료 소비의 증가에 크게 기여하고 있습니다. 이 부문에 있어서 지속 가능한 솔루션의 필요성으로부터, 제조업체는 종래의 폴리에틸렌(PE) 코팅으로부터 환경 친화적인 대체품으로 이행해, 단열성과 지속 가능성의 양쪽 모두를 높이고 있습니다. 소비자 기호가 계속 진화하는 가운데, 보온성 향상이나 쏟아지기 어려운 뚜껑 등, 컵의 디자인에 있어서 혁신이 지지를 모아, 시장의 성장을 한층 더 강하게 하고 있습니다.

시장은 또한 최종 용도에 따라 분류되며 외식, 시설 및 가정의 각 부문을 포함합니다. 외식산업 부문은 퀵서비스 레스토랑의 급속한 확대, 택배 및 포장 서비스 급증, 일회용이면서도 지속 가능한 음료 포장을 선호하는 소비자 습관의 진화 등에 힘입어 2024년 평가액이 92억 달러로 시장을 선도했습니다. 게다가 플라스틱 폐기물 처리에 관한 규제 압력의 고조가, 생분해성과 퇴비화 가능한 종이컵의 채용을 가속시키고 있어, 시장의 수요를 한층 더 끌어올리고 있습니다.

북미의 종이컵 시장은 2024년에 28.1%의 점유율을 차지했는데, 이는 지속가능한 포장재료에 대한 소비자 취향 증가 및 외출처에서의 음료시장의 확대에 의한 것입니다. 일회용 플라스틱의 금지 등, 플라스틱 폐기물의 삭감을 목적으로 한 정부의 대처가, 이 지역 전체에서 환경 친화적인 종이컵의 채용을 큰폭으로 뒷받침하고 있습니다. 기업은 이러한 지속 가능성의 동향에 점점 보조를 맞추게 되고 있어 시장의 향후 성장 전망을 강화하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 편의점 및 이동중 음료에 대한 수요 증가

- 지속 가능하고 환경 친화적인 포장

- 종이컵 코팅 기술의 진보

- 스페셜티 커피숍 및 독립계 카페의 성장

- 커스터마이즈 및 브랜딩 기회

- 업계의 잠재적 위험 및 과제

- 원재료 가격 변동

- 공급망의 혼란

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 뜨거운 종이컵

- 차가운 종이컵

제6장 시장 추계 및 예측 : 월 유형별(2021-2034년)

- 주요 동향

- 싱글 월 종이컵

- 더블 월 종이컵

- 트리플 월 종이컵

제7장 시장 추계 및 예측 : 용량별(2021-2034년)

- 주요 동향

- 150ml까지

- 151-350ml

- 351-500ml

- 500ml 이상

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 푸드서비스

- 퀵 서비스 레스토랑(QSR)

- 카페 및 커피숍

- 기타

- 아이스크림 팔러, FSR

- 시설

- 가정

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Bender

- Converpack

- Dart Container

- Detmold

- Dispo

- Genpak

- Georgia-Pacific

- Golden Paper Cups

- Graphic Packaging

- Grupo Phoenix

- Huhtamaki

- Ishwara

- Nippon Paper

- Printed Cup Company

- Seda

- Stanpac

- Stora Enso

- Tekni-Plex

- Westrock

The Global Paper Cups Market was valued at USD 14.1 billion in 2024 and is projected to grow at a CAGR of 4.1% from 2025 to 2034. This expansion is fueled by increasing consumer demand for convenient, portable beverage options and the rising popularity of specialty coffee shops and independent cafes worldwide. The evolving lifestyle preferences of urban consumers, coupled with the global push toward sustainability, are driving the need for innovative and eco-friendly paper cup solutions. As more consumers seek out artisanal and premium coffee experiences, cafes and quick-service restaurants are responding by adopting high-quality, sustainable paper cups. These trends reflect a broader industry shift toward environmentally responsible packaging, creating lucrative opportunities for paper cup manufacturers aiming to meet both consumer expectations and regulatory requirements.

The growing emphasis on sustainability has led to increased investment in biodegradable and compostable alternatives to traditional plastic-coated paper cups. With mounting government regulations on single-use plastics, manufacturers are actively developing paper cups with coatings made from bio-based and polylactic acid (PLA) materials, which offer superior insulation while reducing environmental impact. Additionally, rising health awareness among consumers has led to a preference for chemical-free, recyclable paper cups, further driving demand across various end-use sectors. Businesses are also recognizing the importance of branding and customization, leading to a surge in demand for printed and branded paper cups that enhance customer engagement and marketing efforts. These factors collectively contribute to the strong growth trajectory of the global paper cups market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.1 Billion |

| Forecast Value | $21.1 Billion |

| CAGR | 4.1% |

The paper cups market is segmented into two main categories: hot and cold paper cups. In 2024, the hot paper cups segment accounted for USD 8.7 billion in revenue, driven by the surging demand for on-the-go hot beverages such as coffee and tea. Urbanization and fast-paced lifestyles have significantly contributed to the increased consumption of hot beverages, particularly from quick-service restaurants and cafes. The need for sustainable solutions in this segment has led manufacturers to shift from conventional polyethylene (PE) coatings to eco-friendly alternatives, enhancing both insulation and sustainability. As consumer preferences continue to evolve, innovations in cup design, including improved heat retention and spill-resistant lids, are gaining traction, further strengthening market growth.

The market is also categorized based on end-use applications, including foodservice, institutional, and household segments. The foodservice segment led the market with a valuation of USD 9.2 billion in 2024, fueled by the rapid expansion of quick-service restaurants, the surge in food delivery and takeaway services, and evolving consumer habits favoring disposable yet sustainable beverage packaging. Additionally, increasing regulatory pressures on plastic waste disposal are accelerating the adoption of biodegradable and compostable paper cups, further bolstering market demand.

North America Paper Cups Market accounted for a 28.1% share in 2024, driven by the growing consumer preference for sustainable packaging materials and the expanding market for on-the-go beverages. Government initiatives aimed at reducing plastic waste, including bans on single-use plastics, have significantly boosted the adoption of eco-friendly paper cups across the region. Businesses are increasingly aligning with these sustainability trends, reinforcing the market's growth outlook in the years to come.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in demand for convenience & on-the-go beverages

- 3.2.1.2 Sustainable and eco-friendly packaging

- 3.2.1.3 Advancements in paper cup coating technologies

- 3.2.1.4 Growth of specialty coffee shops & independent cafes

- 3.2.1.5 Customization & branding opportunities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating raw material price

- 3.2.2.2 Supply chain disruption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Hot paper cups

- 5.3 Cold paper cups

Chapter 6 Market Estimates and Forecast, By Wall Type, 2021 – 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Single wall paper cups

- 6.3 Double wall paper cups

- 6.4 Triple wall paper cups

Chapter 7 Market Estimates and Forecast, By Capacity, 2021 – 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Up to 150 ml

- 7.3 151 to 350 ml

- 7.4 351 to 500 ml

- 7.5 Above 500 ml

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Foodservice

- 8.2.1 Quick service restaurants (QSRs)

- 8.2.2 Cafes and coffee shops

- 8.2.3 Others

- 8.2.3.1 Ice cream parlour, FSR

- 8.3 Institutional

- 8.4 Household

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bender

- 10.2 Converpack

- 10.3 Dart Container

- 10.4 Detmold

- 10.5 Dispo

- 10.6 Genpak

- 10.7 Georgia-Pacific

- 10.8 Golden Paper Cups

- 10.9 Graphic Packaging

- 10.10 Grupo Phoenix

- 10.11 Huhtamaki

- 10.12 Ishwara

- 10.13 Nippon Paper

- 10.14 Printed Cup Company

- 10.15 Seda

- 10.16 Stanpac

- 10.17 Stora Enso

- 10.18 Tekni-Plex

- 10.19 Westrock