|

시장보고서

상품코드

1698271

상피종 치료 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Epithelioma Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 상피종 치료 시장은 2024년 약 52억 달러로 평가되었으며, 2025-2034년 연평균 복합 성장률(CAGR) 9.4%로 성장할 것으로 예측됩니다.

이 시장은 기저세포암 및 편평상피암 등 양성 또는 악성 상피조직종양의 증례 증가로 확대되고 있습니다. 치료는 종양 제거, 재발 예방, 유해 작용 경감에 중점을 두고 있습니다. 인지도 향상, 조기 발견, 정부의 대처가 시장 성장을 촉진하는 주요 요인입니다. 피부암 환자의 증가가 혁신적인 치료법에 대한 수요를 부추겨 치료법의 대폭적인 진보로 이어지고 있습니다. 지속적인 연구개발 노력 및 신약 승인이 시장 확대를 더욱 뒷받침하고 있습니다. 규제 기관은 선진적인 치료 솔루션의 도입을 지원하고 있으며, 효과적인 치료 옵션에 대한 환자의 액세스를 개선하고 있습니다. 의료 기술의 향상도, 보다 뛰어난 질병 관리를 가능하게 함으로써 시장의 성장을 강화하고 있습니다.

시장은 유형별, 약제 클래스별, 유통채널별로 구분됩니다. 유형별로는 기저세포암이 가장 큰 점유율을 차지했으며, 2024년에는 35억 달러의 매출을 올렸습니다. 비흑색종 피부암의 가장 일반적인 형태로서 그 이환율의 증가는 효과적인 치료에 대한 수요를 높이고 있습니다. 장시간의 자외선 노출 및 라이프 스타일의 변화와 같은 요인이 이환률의 급증에 기여하고 있습니다. 조기 발견에 대한 의식의 고조가 선진적인 치료법의 필요성을 더욱 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 52억 달러 |

| 예측 금액 | 115억 달러 |

| CAGR | 9.4% |

약제 등급별로는 헤지호그 경로 억제제가 압도적인 점유율을 차지했으며, 2024년 시장 총수익의 42.4%를 차지했습니다. 이 분야 성장의 원동력이 되고 있는 것은, 특히 일조 시간이 길고 고령화가 진행되는 지역에서의 기저 세포암 유병률의 증가입니다. 이러한 억제제는 진행 및 전이증례에 대한 유효성이 입증되었으며, 기존의 화학요법 및 방사선요법보다 높은 채택률로 이어지고 있습니다. 현재 진행 중인 조사 및 임상시험을 통해 헤지호그 경로 억제제가 더 도입될 가능성이 높아 환자 치료 선택지가 확대됩니다.

유통 채널의 경우 병원 약국이 주요 부문으로 부상했으며, 2024년에는 27억 달러를 창출했습니다. 이 약국들은 상피종 치료를 받고 있는 입원 환자들에게 의약품에 대한 즉각적인 접근을 제공하는 데 중요한 역할을 하고 있습니다. 기저세포암이나 편평상피암의 입원환자수 증가가 이 부문의 확대에 기여하고 있습니다. 병원 약국은 또한 포괄적인 치료를 보장하고 환자의 전귀를 개선하는 지지 요법 서비스를 촉진합니다.

지역별로는 북미가 상피종 치료 시장의 주요 기업입니다. 특히 미국은 대폭적인 성장이 예상되고 있으며, 시장 수익은 2023년 20억 달러에서 2034년에는 47억 달러로 증가할 것으로 예측됩니다. 이 국가는 선진 치료의 채택을 촉진하는 유리한 규제 상황의 혜택을 받고 있습니다. 신규 치료에 대한 규제 당국의 승인이 시장 성장을 촉진하고, 향후 몇 년간 이 지역의 우위성이 강해질 것으로 예상됩니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 피부암 유병률의 상승

- 표적요법 및 면역요법의 진보

- 헬스케어 인프라 및 계발 캠페인의 지원

- 업계의 잠재적 위험 및 과제

- 고액의 치료비

- 진행기에 있어서 한정적인 유효성 및 부작용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 갭 분석

- 특허 분석

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 기저세포암

- 편평상피암

- 기타 유형

제6장 시장 추계 및 예측 : 약제 클래스별(2021-2034년)

- 주요 동향

- 헤지호그 경로 억제제

- 면역관문 억제제

- 화학요법제

- 기타 약제 클래스별

제7장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 병원 약국

- 소매 약국

- 전자상거래

- 기타 유통 채널

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Amgen

- AstraZeneca

- BeiGene

- Bristol-Myers Squibb

- F. Hoffmann-La Roche

- Johnson &Johnson

- Merck and Co.

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Sun Pharmaceutical Industries

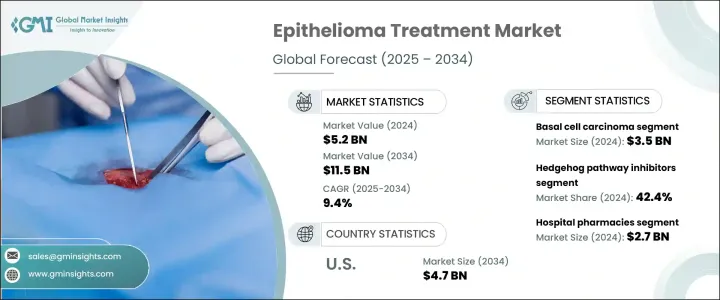

The Global Epithelioma Treatment Market was valued at approximately USD 5.2 billion in 2024 and is projected to grow at a 9.4% CAGR from 2025 to 2034. The market is expanding due to rising cases of epithelial tissue tumors, which may be benign or malignant, such as basal cell carcinoma and squamous cell carcinoma. Treatment focuses on removing tumors, preventing recurrence, and mitigating harmful effects. Increasing awareness, early detection, and government initiatives are key factors driving market growth. The growing number of skin cancer cases has fueled demand for innovative therapies, leading to significant advancements in treatment methods. Continuous R&D efforts and new drug approvals are further propelling market expansion. Regulatory bodies are supporting the introduction of advanced therapeutic solutions, improving patient access to effective treatment options. Medical technology improvements have also strengthened market growth by enabling better disease management.

The market is segmented by type, drug class, and distribution channel. Based on type, basal cell carcinoma accounted for the largest share, generating USD 3.5 billion in revenue in 2024. As the most prevalent form of non-melanoma skin cancer, its rising incidence has increased the demand for effective treatments. Factors such as prolonged UV exposure and shifting lifestyle patterns have contributed to the surge in cases. Greater awareness of early detection has further boosted the need for advanced therapies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 9.4% |

By drug class, hedgehog pathway inhibitors held the dominant share, contributing 42.4% of total market revenue in 2024. The segment growth is driven by the increasing prevalence of basal cell carcinoma, especially in regions with high sunlight exposure and aging populations. These inhibitors have demonstrated efficacy in treating advanced and metastatic cases, leading to their higher adoption over traditional chemotherapy and radiation therapies. Ongoing research and clinical trials are likely to introduce additional hedgehog pathway inhibitors, expanding treatment options for patients.

Regarding distribution channels, hospital pharmacies emerged as the leading segment, generating USD 2.7 billion in 2024. These pharmacies play a crucial role in providing immediate access to medications for inpatients undergoing treatment for epithelioma. The rising number of hospital admissions for basal cell carcinoma and squamous cell carcinoma has contributed to segment expansion. Hospital pharmacies also facilitate supportive care services, ensuring comprehensive treatment and improving patient outcomes.

Regionally, North America is a key player in the epithelioma treatment market. The United States, in particular, is projected to witness substantial growth, with market revenue increasing from USD 2 billion in 2023 to USD 4.7 billion by 2034. The country benefits from a favorable regulatory landscape that promotes the adoption of advanced therapies. Regulatory approvals for novel treatments are expected to drive market progression, strengthening the region's dominance in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of skin cancer

- 3.2.1.2 Advancements in targeted therapies and immunotherapies

- 3.2.1.3 Supportive healthcare infrastructure and awareness campaigns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Limited efficacy and adverse effects in advanced stages of the disease

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Pipeline analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Basal cell carcinoma

- 5.3 Squamous cell carcinoma

- 5.4 Other types

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hedgehog pathway inhibitors

- 6.3 Immune checkpoint inhibitors

- 6.4 Chemotherapeutic agents

- 6.5 Other drug classes

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 E-commerce

- 7.5 Other distribution channels

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amgen

- 9.2 AstraZeneca

- 9.3 BeiGene

- 9.4 Bristol-Myers Squibb

- 9.5 F. Hoffmann-La Roche

- 9.6 Johnson & Johnson

- 9.7 Merck and Co.

- 9.8 Novartis

- 9.9 Pfizer

- 9.10 Regeneron Pharmaceuticals

- 9.11 Sanofi

- 9.12 Sun Pharmaceutical Industries