|

시장보고서

상품코드

1698280

인크레틴계 의약품 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Incretin-based Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

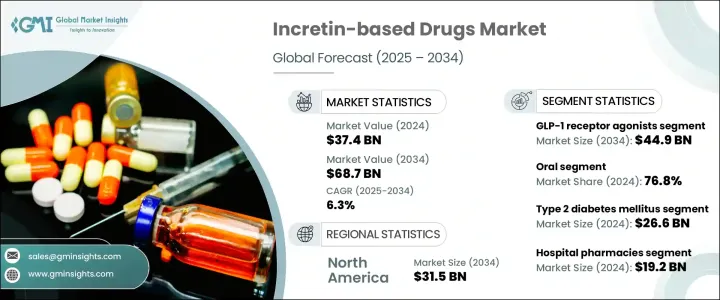

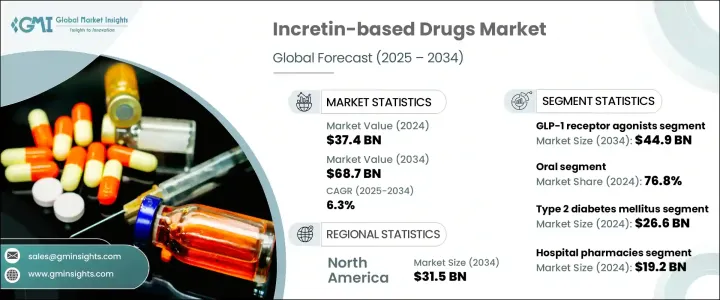

세계의 인크레틴계 의약품 시장은 2024년 374억 달러로 평가되었으며, 2025-2034년 연평균 복합 성장률(CAGR) 6.3%로 성장할 것으로 예상됩니다.

인크레틴계 의약품은 식후 혈당를 조절하는 장내 호르몬에 의해 인슐린 분비를 자극함으로써 2형 당뇨병의 관리에 도움이 됩니다. 주로 비만, 고령화, 앉아 있는 라이프 스타일에 의한 당뇨병 유병률의 증가는 시장 확대를 촉진하는 중요한 요인입니다. 환자 의식의 고조, 약제 제제의 진보, 당뇨병 치료에 대한 액세스 향상이, 이 성장을 한층 더 뒷받침하고 있습니다.

시장은 약제 유형별로 GLP-1 수용체 작용제와 DPP-4 억제제로 분류되며, 2023년 시장 규모는 355억 달러였습니다. GLP-1 수용체 작용제에 대한 수요가 높아지는 것은 인슐린 분비를 촉진하고 글루카곤 농도를 억제해 혈당을 효과적으로 관리하는 그 능력에 따른 것입니다. 이러한 약제는 또한 식욕을 조절하고 소화를 지연시킴으로써 체중 감소를 촉진하기 때문에 당뇨병 환자에게 있어서 바람직한 선택지가 되고 있습니다. 주 1회 주사 등의 서방성 제제는 환자의 복약 애드히어런스를 향상시켜 시장 규모를 확대하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 374억 달러 |

| 예측 금액 | 687억 달러 |

| CAGR | 6.3% |

시장은 또한 투여경로에 따라 경구약과 주사약으로 구분됩니다. 경구약 부문은 2024년에 287억 달러를 차지했으며, 시장 점유율은 76.8%였습니다. 경구약은 주사제를 대체할 수 있는 편리성을 제공하고 환자의 컴플라이언스 향상으로 이어집니다. 지속적인 연구 노력에 의해 유효성과 안전성 프로파일이 개선되어 경구약을 점점 선호하게 되고 있습니다. 이러한 제제는 배포, 보관, 투여가 용이하기 때문에 헬스케어 제공자의 부담이 경감되고 다양한 의료 현장에서의 이용 편의성이 향상되었습니다.

적응증별로는 2형 당뇨병, 비만증 및 체중관리, 기타 대사장애증이 포함됩니다. 제2형 당뇨병 부문이 가장 큰 점유율을 차지했으며, 2024년 매출액은 266억 달러였습니다. 제2형 당뇨병의 세계 이환율 상승은 식생활 불규칙 및 생활 습관의 악화에 기인하고 있으며, 인크레틴계 의약품의 수요를 촉진하고 있습니다. 이 치료제들은 저혈당 위험을 줄이면서 효과적으로 혈당을 낮추기 때문에 고령화된 사람들이나 혈당 변동이 심한 사람들에게 안전한 치료 선택지를 제공합니다.

유통 채널은 병원 약국, 소매 약국, 전자상거래로 구성됩니다. 병원 약국은 2024년 매출액이 192억 달러로 시장을 선도했습니다. 이러한 환경에서는, 특히 새롭게 진단된 환자 및 전문적인 치료를 필요로 하는 환자에게 있어서, 약에 대한 확실한 액세스가 보증됩니다. 약사는 용량, 부작용, 제제의 차이에 관한 지도를 실시해 치료의 애드히어런스를 높입니다. 투약 관리 프로그램 및 치료 반응의 면밀한 모니터링 등 포괄적인 지원 서비스가 더욱 시장 성장에 기여하고 있습니다.

북미는 시장을 독점하며, 2024년에는 171억 달러를 차지하였고, 미국은 155억 달러로 최고를 차지했습니다. 당뇨병, 심혈관 질환, 비만의 유병률 증가가 인크레틴계 의약품에 대한 수요를 계속 견인하고 있습니다. 이 지역 시장 확대에는 지원 규제 프레임워크 및 의약품 개발의 급속한 발전이 기여하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 2형 당뇨병 유병률 상승

- 비 인슐린 요법으로의 이동

- 약물 전달 기술의 진보

- 심혈관 및 체중 관리의 장점

- 업계의 잠재적 위험 및 과제

- 높은 치료비

- 부작용 및 금기

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 갭 분석

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 약제 유형별(2021-2034년)

- 주요 동향

- GLP-1 수용체 작용제

- DPP-4 억제제

제6장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 경구제

- 주사제

제7장 시장 추계 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 2형 당뇨병

- 비만증 및 체중 관리

- 기타 대사성 질환

제8장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 병원 약국

- 소매 약국

- 전자상거래

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AstraZeneca

- Boehringer Ingelheim

- Eli Lilly and Company

- GlaxoSmithKline

- Lupin Limited

- Merck

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceutical Company

- Viatris

The Global Incretin-Based Drugs Market was valued at USD 37.4 billion in 2024 and is predicted to grow at a CAGR of 6.3% from 2025 to 2034. Incretin-based drugs help manage type 2 diabetes by stimulating insulin secretion through gut hormones, which regulate blood sugar levels after meals. The growing prevalence of diabetes, primarily due to obesity, aging populations, and sedentary lifestyles, is a key factor driving market expansion. Increasing patient awareness, advancements in drug formulations, and improved accessibility to diabetes treatments further support this growth.

The market is categorized by drug type into GLP-1 receptor agonists and DPP-4 inhibitors, with a market size of USD 35.5 billion in 2023. The rising demand for GLP-1 receptor agonists is driven by their ability to enhance insulin secretion and suppress glucagon levels, effectively managing blood sugar. These drugs also promote weight loss by controlling appetite and slowing digestion, making them a preferred option for diabetes patients. Extended-release formulations, such as once-weekly injections, improve patient adherence and expand market reach.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.4 Billion |

| Forecast Value | $68.7 Billion |

| CAGR | 6.3% |

The market is also segmented by the route of administration into oral and injectable drugs. The oral segment accounted for USD 28.7 billion in 2024, with a market share of 76.8%. Oral formulations offer a convenient alternative to injections, leading to higher patient compliance. Continuous research efforts have led to improved efficacy and safety profiles, making oral medications increasingly preferred. These formulations are easy to distribute, store, and administer, reducing the burden on healthcare providers and enhancing accessibility across various healthcare settings.

By indication, the market includes type 2 diabetes mellitus, obesity and weight management, and other metabolic disorders. The type 2 diabetes mellitus segment held the largest share, generating USD 26.6 billion in revenue in 2024. The rising global incidence of type 2 diabetes, attributed to poor dietary habits and lifestyle factors, fuels the demand for incretin-based drugs. These medications effectively lower blood sugar levels while reducing the risk of hypoglycemia, offering a safer treatment option for aging populations and those prone to severe blood sugar fluctuations.

The distribution channel segment comprises hospital pharmacies, retail pharmacies, and e-commerce. Hospital pharmacies led the market with USD 19.2 billion in revenue in 2024. These settings ensure secure access to medications, particularly for newly diagnosed patients or those requiring specialized care. Pharmacists provide guidance on dosage, side effects, and formulation differences, enhancing treatment adherence. Comprehensive support services, including medication management programs and close monitoring of treatment responses, further contribute to market growth.

North America dominated the market, accounting for USD 17.1 billion in 2024, with the U.S. leading at USD 15.5 billion. The rising prevalence of diabetes, cardiovascular diseases, and obesity continues to drive demand for incretin-based drugs. Supportive regulatory frameworks and rapid advancements in drug development contribute to the region's market expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of type 2 diabetes mellitus

- 3.2.1.2 Shift toward non-insulin therapies

- 3.2.1.3 Advancements in drug delivery technologies

- 3.2.1.4 Cardiovascular and weight management benefits

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Adverse effects and contraindications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Pipeline analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 GLP-1 receptor agonists

- 5.3 DPP-4 inhibitors

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Injectable

Chapter 7 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Type 2 diabetes mellitus

- 7.3 Obesity and weight management

- 7.4 Other metabolic disorders

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Boehringer Ingelheim

- 10.3 Eli Lilly and Company

- 10.4 GlaxoSmithKline

- 10.5 Lupin Limited

- 10.6 Merck

- 10.7 Novo Nordisk

- 10.8 Pfizer

- 10.9 Sanofi

- 10.10 Takeda Pharmaceutical Company

- 10.11 Viatris