|

시장보고서

상품코드

1698285

펩티드 항생제 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Peptide Antibiotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

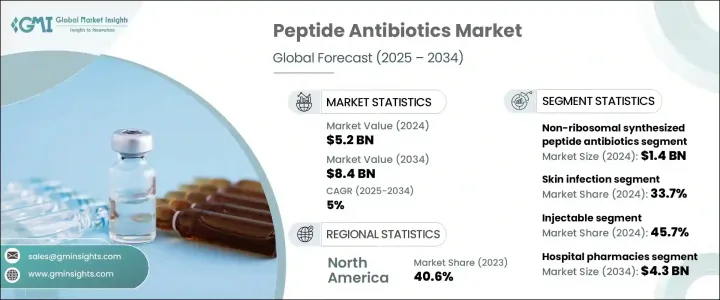

세계의 펩티드 항생제 시장은 2024년에 52억 달러로 평가되었으며, 2025-2034년 CAGR 5%로 성장할 것으로 예측됩니다.

항균제 내성(AMR)의 위협이 높아지고 고급 항생제 솔루션에 대한 수요가 급증함에 따라 시장이 크게 확대되고 있습니다. 세균감염병이 기존 치료에 내성을 갖게 됨에 따라 펩티드 항생제가 중요한 대체품으로 떠오르고 있습니다. 폴리믹신이나 그라미시딘을 포함한 이들 특수 항생제는 다제내성(MDR) 미생물에 대해 강력한 활성을 나타내 내성 감염증 대책에 필수적인 것이 되고 있습니다.

세계의 헬스케어 시스템이 항생제 내성의 증례 증가에 임하고 있는 가운데 제약회사는 혁신적인 펩티드 항생제를 시장에 투입하기 위해 연구개발에 주력하고 있습니다. 병원 내 감염(HAI) 및 혈류 감염증의 유행은 효과적인 치료 옵션의 필요성을 더욱 높이고 있으며, 이 분야에 대한 투자를 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 52억 달러 |

| 예측 금액 | 84억 달러 |

| CAGR | 5% |

제약업계의 주요 기업이 효능을 높이고 내성 리스크를 최소화하는 신규 제제의 공동개발에 임하고 있기 때문에 펩티드 기반의 신규 치료제의 파이프라인은 확대되고 있습니다. 또한 AMR에 대처하기 위한 정부의 이니셔티브 증가 및 항생제 연구에 대한 자금 지원이 시장의 성장 궤도를 형성하는 데 중요한 역할을 하고 있습니다. 최소한의 부작용으로 표적을 좁힌 작용을 발휘하는 차세대 항생제가 중시되고 있는 것이 펩티드 기반 솔루션 개발에 박차를 가하고 있어 기존 치료법으로는 듣지 않게 된 중증 세균감염병 치료에 특히 유용합니다.

시장은 주로 리보솜과 비리보솜 합성 펩티드 항생제로 분류됩니다. 2024년에는 비리보솜 합성 펩타이드 항생제 분야가 시장을 독점하며 14억 달러의 평가액을 보유했습니다. 이 항생제들은 비리보솜 펩티드 합성효소(NRPS)를 통해 생산되며, 구조의 다양성과 효소 분해에 대한 내성을 강화합니다. 비단백성 아미노산을 흡수하는 그 능력은 뛰어난 항균 특성을 가져와 고도의 내성을 가진 병원체에 보다 효과적으로 작용합니다. 그 결과, 비리보솜 합성 펩티드 항생제는 보다 내구성이 있고 폭넓은 항균제를 찾는 헬스케어 공급자와 조사 연구자들 사이에서 계속해서 선호되고 있습니다.

펩티드 항생제 시장은 피부 감염, 원내 세균성 폐렴, 혈류 감염, 기타 세균성 질환 등 주요 관심 분야를 포함한 용도별로 구분되어 있습니다. 피부 감염증은 2024년에 시장의 33.7%를 차지하는 주요 세그먼트로 부상했습니다. 봉와직염, 농가진, 당뇨병성 족궤양 등 질환 유병률 증가, 만성 창상 및 수술 후 감염병 급증이 이들 표적 항생제 수요를 촉진하고 있습니다. 펩티드 항생제는 전신 독성을 경감한 보다 정확한 치료 접근법을 제공하기 때문에 장기 항균 요법을 필요로 하는 기저 질환을 가진 환자에게 매우 효과적입니다.

북미는 펩티드 항생제의 지역별 시장에서 지배적인 지위를 유지하고 있으며, 2023년에는 40.6%의 점유율을 차지했습니다. 특히 미국은, 강력한 제약 연구 에코 시스템, 확립된 규제 틀, 고액의 헬스케어 지출에 힘입어, 이 분야의 성장을 계속 견인하고 있습니다. 미국에는 대형 바이오 테크놀로지 기업 및 제약 기업이 존재해, 항생 물질 개발에 있어서 계속적인 기술 혁신을 촉진하고 있습니다. AMR 환자가 증가함에 따라, 이 나라에서는 새로운 펩티드 항생제에 대한 수요가 증가하고, 항생제 내성의 위험을 저감하는 보다 초점을 맞춘 효율적인 치료 옵션이 제공되게 됩니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 다제 내성(MDR)균 증가

- 급성 및 만성 감염의 발생률 증가

- 펩티드 합성 기술의 진보

- 업계의 잠재적 위험 및 과제

- 높은 제조 비용

- 경구 생체이용률의 한계

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 파이프라인 분석

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 리보솜 합성 펩티드 항생제

- 비리보솜 합성 펩티드 항생제

제6장 시장 추계 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 피부 감염증

- 원내 세균성 폐렴 및 인공호흡기 관련 세균성 폐렴(HABP/VABP)

- 혈류 감염증

- 기타 적응증

제7장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 주사

- 경구

- 국소

- 기타 투여 경로

제8장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 병원 약국

- 소매 약국

- 온라인 약국

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AbbVie

- ANI Pharmaceuticals

- Cumberland Pharmaceuticals

- Eli Lilly and Company

- GSK plc

- JHP Pharmaceuticals

- Merck

- Monarch Pharmachem

- Melinta Therapeutics

- NPS Pharmaceuticals

- Pfizer

- Sanofi

- Sandoz

- Teva Pharmaceuticals

- The Menarini Group

- Xellia Pharmaceuticals

The Global Peptide Antibiotics Market was valued at USD 5.2 billion in 2024 and is projected to grow at a CAGR of 5% from 2025 to 2034. The market is experiencing significant expansion due to the escalating threat of antimicrobial resistance (AMR), which has led to an urgent demand for advanced antibiotic solutions. With bacterial infections becoming increasingly resistant to conventional treatments, peptide antibiotics are emerging as a crucial alternative. These specialized antibiotics, including polymyxins and gramicidin, exhibit potent activity against multidrug-resistant (MDR) microbes, making them indispensable in combating resistant infections.

As healthcare systems worldwide grapple with rising cases of antibiotic resistance, pharmaceutical companies are focusing on research and development efforts to bring innovative peptide antibiotics to the market. The growing prevalence of hospital-acquired infections (HAIs) and bloodstream infections has further intensified the need for effective treatment options, driving investments in this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $8.4 Billion |

| CAGR | 5% |

The pipeline for new peptide-based treatments is expanding as major players in the pharmaceutical industry collaborate on novel drug formulations that enhance efficacy and minimize resistance risks. Additionally, increasing government initiatives to tackle AMR and funding for antibiotic research are playing a crucial role in shaping the growth trajectory of the market. The emphasis on next-generation antibiotics that provide targeted action with minimal side effects is fueling the development of peptide-based solutions, which are particularly useful in treating severe bacterial infections that no longer respond to traditional therapies.

The market is primarily categorized into ribosomal and non-ribosomal synthesized peptide antibiotics. In 2024, the non-ribosomal synthesized peptide antibiotics segment dominated the market, holding a valuation of USD 1.4 billion. These antibiotics, produced through non-ribosomal peptide synthetases (NRPSs), offer structural diversity and enhanced resistance to enzymatic degradation. Their ability to incorporate non-proteinogenic amino acids gives them superior antimicrobial properties, making them more effective in tackling highly resistant pathogens. As a result, non-ribosomal synthesized peptide antibiotics continue to be the preferred choice among healthcare providers and researchers striving for more durable and broad-spectrum antibacterial agents.

The peptide antibiotics market is segmented by application, with key focus areas including skin infections, hospital-acquired bacterial pneumonia, bloodstream infections, and other bacterial conditions. Skin infections emerged as the leading segment in 2024, accounting for a 33.7% share of the market. The increasing prevalence of conditions such as cellulitis, impetigo, and diabetic foot ulcers, along with a surge in chronic wounds and post-surgical infections, is fueling demand for these targeted antibiotics. Peptide antibiotics offer a more precise treatment approach with reduced systemic toxicity, making them highly effective for patients with underlying health conditions requiring prolonged antibacterial therapy.

North America remained the dominant regional market for peptide antibiotics, accounting for a 40.6% share in 2023. The United States, in particular, continues to drive growth in this sector, supported by a strong pharmaceutical research ecosystem, a well-established regulatory framework, and substantial healthcare spending. The presence of leading biotechnology and pharmaceutical firms in the U.S. fosters continuous innovation in antibiotic development. With the rise of AMR cases, the demand for new peptide antibiotics in the country is set to increase, providing more targeted and efficient treatment options that reduce the risk of antibiotic resistance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of multi-drug resistant (MDR) bacteria

- 3.2.1.2 Increasing incidence of acute and chronic infectious diseases

- 3.2.1.3 Technological advancements in peptide synthesis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Limited oral bioavailability

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Ribosomal synthesized peptide antibiotics

- 5.3 Non-ribosomal synthesized peptide antibiotics

Chapter 6 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Skin infection

- 6.3 Hospital-acquired bacterial pneumonia and ventilator-associated bacterial pneumonia (HABP/VABP)

- 6.4 Blood stream infections

- 6.5 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Injectable

- 7.3 Oral

- 7.4 Topical

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 ANI Pharmaceuticals

- 10.3 Cumberland Pharmaceuticals

- 10.4 Eli Lilly and Company

- 10.5 GSK plc

- 10.6 JHP Pharmaceuticals

- 10.7 Merck

- 10.8 Monarch Pharmachem

- 10.9 Melinta Therapeutics

- 10.10 NPS Pharmaceuticals

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sandoz

- 10.14 Teva Pharmaceuticals

- 10.15 The Menarini Group

- 10.16 Xellia Pharmaceuticals