|

시장보고서

상품코드

1698321

이중보온관 시스템 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Pre-Insulated Pipe Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

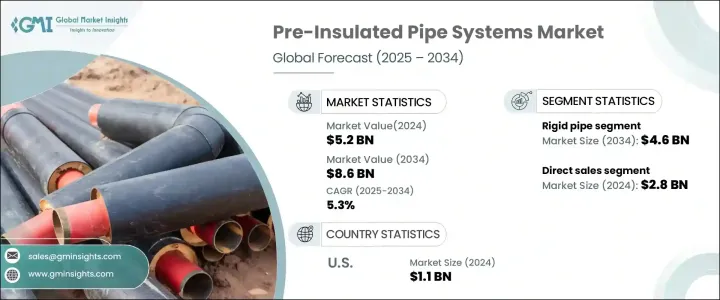

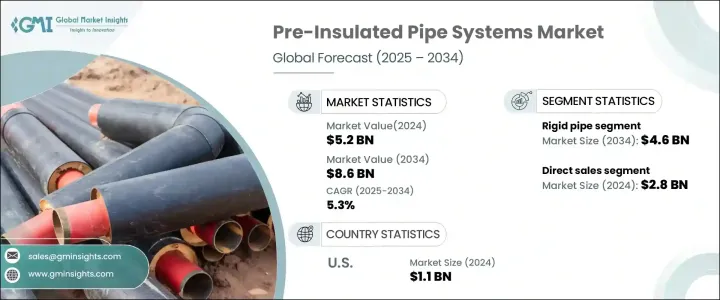

세계의 이중보온관 시스템 시장은 2024년 52억 달러로 평가되었으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.3%를 나타낼 것으로 예상됩니다.

지역 냉난방 시스템의 채용이 증가하고 있는 것이, 이 성장의 주된 요인입니다. 이러한 시스템에서는 복수의 건물에 집중형의 냉난방을 공급하기 위해서 고효율의 인프라가 필요하기 때문입니다. 효과적인 열관리 솔루션의 필요성이 높아지고 있습니다. 화학, 제약, 석유화학, 데이터센터 등의 산업 확대는 온수, 냉각수, 기름, 폐수의 운송에 이중보온관 시스템이 필수적이기 때문에 시장의 성장을 한층 더 가속시킵니다.

시장은 제품 유형별로 연질관와 경질관으로 구분됩니다. 외부 케이싱, 절연층, 중실의 내관을 특징으로 하는 경질 이중보온관은 지역 난방 시스템, 화학 처리, 석유 및 가스관 라인, 대규모 인프라 프로젝트에서 널리 사용되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 52억 달러 |

| 예측 금액 | 86억 달러 |

| CAGR | 5.3% |

유통 채널별로 볼 때 시장은 직접 판매와 간접 판매로 나뉩니다. 직접 판매 분야는 2024년 28억 달러로 평가되었고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.5%를 나타낼 것으로 예측됩니다. 직접 판매는 제조업체가 건설 회사, 산업 기업, 정부 기관 등 최종 사용자에게 제품을 공급하는 것입니다. 이 접근법은 장기적인 협력 관계를 키우고 맞춤형 솔루션을 보장합니다. 전력 및 에너지 부문을 포함한 대규모 인프라 프로젝트는 프로젝트 일정을 준수하는 데 직접 판매가 효율적이기 때문에 직접 조달에 크게 의존합니다. 제조업체는 고객과 직접적인 커뮤니케이션을 통해 맞춤형 제품을 제공하고 리드 타임을 단축할 수 있다는 장점이 있습니다.

미국의 이중보온관 시스템 시장은 2024년에 11억 달러로 평가되었으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.2%를 나타낼 것으로 예측됩니다. 북미 시장 확대는 급속한 도시화, 인프라 개척, 지역 냉난방 시스템의 채용 확대가 원동력이 되고 있습니다. 에너지 효율과 지속가능성에 대한 노력이 중시되고, 재생가능 에너지 프로젝트 증가도 함께 수요는 더욱 높아지고 있습니다. 상업 및 산업 분야에서 열효율을 높이기 위한 노력이 진행됨에 따라, 이중보온관 시스템은 에너지 사용 최적화 및 운영 비용 절감에 중요한 역할을 계속하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 파라미터

- 데이터 소스

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴적 혁신

- 향후 전망

- 제조업체

- 유통업체

- 소매업체

- 영향요인

- 성장 촉진요인

- 지역 냉난방 시스템 수요 급증

- 최종 이용 산업에서의 수요 증가

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용과 유지 보수 비용

- 안전에 대한 우려와 숙련 노동자의 부족

- 성장 촉진요인

- 기술 혁신의 상황

- 잠재성장력의 분석

- 규제 상황

- 가격 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계·예측 : 제품 유형별(2021-2032년)

- 연질관

- 경질관

제6장 시장 추계·예측 : 방화 유형별(2021-2032년)

- 주요 동향

- 난연성관

- 비난연성관

제7장 난연성관 시장 추계·예측 : 차원별(2021-2032년)

- 주요 동향

- 소구경관(최대 65mm)

- 연질관

- 경질관

- 중구경관(65-300mm)

- 연질관

- 경질관

- 대구경관(300mm 이상)

- 연질관

- 경질관

제8장 시장 추계·예측 : 설치별(2021-2032년)

- 주요 동향

- 지하

- 지상

제9장 시장 추계·예측 : 최종 용도별(2021-2032년)

- 주요 동향

- 주거용 건물

- 상업용 건물

- 산업용 건물

제10장 시장 추계·예측 : 유통 채널별(2021-2032년)

- 주요 동향

- 직접 판매

- 간접 판매

제11장 시장 추계·예측 : 지역별(2021-2032년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 중동 및 아프리카

- 사우디아라비아

- UAE

- 남아프리카

- 세계 기타 지역

제12장 기업 프로파일

- Aquatherm

- Brugg Group

- CPV

- Ecoline

- Elips

- Georg Fischer

- Insul-Pipe Systems

- KE KELIT

- LOGSTOR

- Perma-Pipe International

- Polypipe Group

- REHAU

- Thermaflex International

- Vital Energi Utilities

- Watts Water Technologies

The Global Pre-Insulated Pipe Systems Market, valued at USD 5.2 billion in 2024, is expected to expand at a CAGR of 5.3% from 2025 to 2034. The rising adoption of district heating and cooling systems is a key driver of this growth, as these systems require highly efficient infrastructure to deliver centralized heating and cooling to multiple buildings. Pre-insulated pipes are designed to minimize heat loss during transmission, enhancing energy efficiency. As global temperatures rise, cooling demand is projected to increase, pushing the need for effective thermal management solutions. The expansion of industries such as chemical, pharmaceutical, petrochemical, and data centers further accelerates market growth, as pre-insulated pipe systems are essential for transporting hot water, cooling water, oil, and wastewater. The increasing focus on energy-efficient solutions in large-scale industrial applications is also a contributing factor.

The market is segmented by product type into flexible and rigid pipes. The rigid pipe segment, valued at USD 2.8 billion in 2024, is anticipated to reach USD 4.6 billion by 2034. This segment is expected to maintain its dominance due to its durability, resistance to extreme temperatures, and ability to withstand mechanical stress and corrosion. Rigid pre-insulated pipes featuring an outer casing, insulating layer, and solid inner pipe are widely used in district heating systems, chemical processing, oil and gas pipelines, and large-scale infrastructure projects. The growing demand for energy in developing regions is fueling their adoption in refineries, power plants, and industrial facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $8.6 Billion |

| CAGR | 5.3% |

By distribution channel, the market is divided into direct and indirect sales. The direct sales segment, valued at USD 2.8 billion in 2024, is projected to grow at a CAGR of 5.5% from 2025 to 2034. Direct sales involve manufacturers supplying products to end users such as construction firms, industrial businesses, and government agencies. This approach fosters long-term collaborations and ensures tailored solutions. Large-scale infrastructure projects, including those in the power and energy sectors, rely heavily on direct procurement due to the efficiency of direct sales in meeting project timelines. Manufacturers benefit from direct communication with customers, enabling them to provide customized products and reduce lead times.

The U.S. pre-insulated pipe systems market, valued at USD 1.1 billion in 2024, is forecasted to grow at a CAGR of 5.2% between 2025 and 2034. North America's market expansion is driven by rapid urbanization, infrastructure development, and increased adoption of district heating and cooling systems. The emphasis on energy efficiency and sustainability initiatives, coupled with the rise of renewable energy projects, is further boosting demand. With growing efforts to enhance thermal efficiency in commercial and industrial applications, pre-insulated pipe systems continue to play a crucial role in optimizing energy usage and reducing operational costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging demand for district heating and cooling system

- 3.2.1.2 Increase in demand from end-use industries

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial and maintenance cost

- 3.2.2.2 Safety concern and limited availability of skilled labor

- 3.2.1 Growth drivers

- 3.3 Technology & innovation landscape

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Pricing analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 – 2032, (USD Million) (Million Meters)

- 5.1 Flexible pipe

- 5.2 Rigid pipe

Chapter 6 Market Estimates & Forecast, By Fire Protection, 2021 – 2032, (USD Million) (Million Meters)

- 6.1 Key trends

- 6.2 Flame-Retardant pipes

- 6.3 Non-Flame-Retardant pipes

Chapter 7 Market Estimates & Forecast, By Dimensions, 2021 – 2032, (USD Million) (Million Meters)

- 7.1 Key trends

- 7.2 Small diameter pipes(Up to 65 mm)

- 7.2.1 Flexible pipe

- 7.2.2 Rigid pipe

- 7.3 Medium diameter pipes(65 to 300 mm)

- 7.3.1 Flexible pipe

- 7.3.2 Rigid pipe

- 7.4 Large diameter pipes(Above 300 mm)

- 7.4.1 Flexible pipe

- 7.4.2 Rigid pipe

Chapter 8 Market Estimates & Forecast, By Installation, 2021 – 2032, (USD Million) (Million Meters)

- 8.1 Key trends

- 8.2 Below ground

- 8.3 Above ground

Chapter 9 Market Estimates & Forecast, By End Use, 2021 – 2032, (USD Million) (Million Meters)

- 9.1 Key trends

- 9.2 Residential buildings

- 9.3 Commercial buildings

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 – 2032, (USD Million) (Million Meters)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 – 2032, (USD Million) (Million Meters)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 MEA

- 11.4.1 Saudi Arabia

- 11.4.2 UAE

- 11.4.3 South Africa

- 11.5 Rest of World

Chapter 12 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 12.1 Aquatherm

- 12.2 Brugg Group

- 12.3 CPV

- 12.4 Ecoline

- 12.5 Elips

- 12.6 Georg Fischer

- 12.7 Insul-Pipe Systems

- 12.8 KE KELIT

- 12.9 LOGSTOR

- 12.10 Perma-Pipe International

- 12.11 Polypipe Group

- 12.12 REHAU

- 12.13 Thermaflex International

- 12.14 Vital Energi Utilities

- 12.15 Watts Water Technologies