|

시장보고서

상품코드

1699277

프로그래머블 로직 컨트롤러(PLC) 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Programmable Logic Controller (PLC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

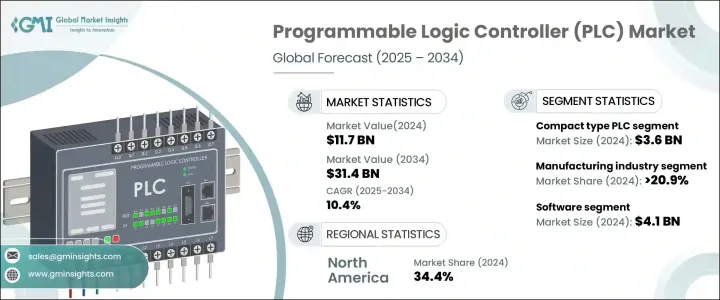

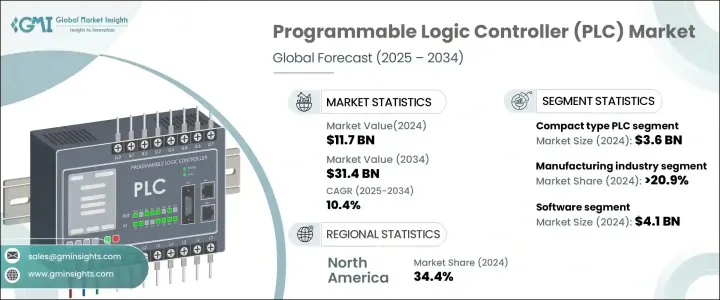

세계의 프로그래머블 로직 컨트롤러 시장은 2024년에 117억 달러로 평가되었으며, 2025-2034년 연평균 복합 성장률(CAGR) 10.4%를 나타낼 것으로 예측됩니다.

인더스트리 4.0, 디지털 트윈 기술, 자동화 주도형 솔루션의 채용이 증가하고 있는 것이 시장 확대에 박차를 가하고 있습니다. 전기차(EV) 수요 증가는 PLC 기반 시스템이 생산라인 자동화 및 제조 효율 최적화에 중요한 역할을 하기 때문에 성장을 더욱 가속화하고 있습니다. 자동차 회사들은 EV 생산을 합리화하고 확장성을 높이며 다운타임을 줄이기 위해 PLC 구동 솔루션에 의존하고 있습니다. 또한 이러한 시스템은 배터리 제조 및 복잡한 조립 공정에 필수적이며 최대 생산성을 확보합니다.

AI 주도의 애널리틱스, 머신 커뮤니케이션, 클라우드 컴퓨팅을 통합하는 인더스트리 4.0 구상은 고급 PLC에 대한 큰 수요를 촉진하고 있습니다. 이러한 시스템은 실시간 데이터 처리 및 매끄러운 연결성을 촉진해, 스마트 제조에 불가결한 것이 되고 있습니다. 디지털 트윈 테크놀로지 및 PLC 기반 시스템을 통합함으로써 제조사는 물리적 운영을 중단하지 않고 성능을 테스트하고 최적화하기 위한 가상 모델을 만들 수 있습니다. 예지 보전과 효율 개선을 위해 디지털 트윈을 채택하는 기업이 늘고 있기 때문에 PLC 제조사들은 이러한 진보에 대응하는 솔루션 개발에 주력하고 있습니다. 다양한 산업에서 지능형 자동화에 대한 요구가 증가하고 있기 때문에 PLC의 수요가 지속되어 현대 산업 생태계에 필수적인 구성 요소로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 117억 달러 |

| 예측 금액 | 314억 달러 |

| CAGR | 10.4% |

시장은 유형별로 모듈형 PLC, 콤팩트 PLC, 랙 마운트형 PLC로 구분됩니다. 그 중에서도 모듈형 PLC는 예측 기간 동안 CAGR 11.1%를 기록할 것으로 예측되며, 가장 높은 성장이 전망됩니다. 이러한 PLC는 뛰어난 확장성과 유연성을 갖추고 있어 제조, 에너지, 수처리, 식품가공 등의 업계에서 선호되고 있습니다. 시스템 전체를 중단시키지 않고 고장난 모듈을 교체할 수 있어 다운타임을 최소화할 수 있어 보급의 원동력이 되고 있습니다.

시장은 최종 용도별로 항공우주 및 방위, 자동차, 화학, 에너지 및 유틸리티, 식품 및 음료, 헬스케어, 제조, 광업 및 금속, 석유 및 가스, 운수로 나눌 수 있습니다. 스마트 공장 및 자동화 생산라인에 PLC 도입이 증가하면서 2024년 시장 점유율은 제조업이 전체의 20.9% 이상을 차지했습니다. 최신 PLC 시스템은 실시간 데이터 처리, 예지 보전, 적응형 자동화를 통해 효율을 높이고 산업의 진보에 필수적인 요소가 되고 있습니다.

시장은 또한 컴포넌트별로 소프트웨어, 하드웨어, 서비스로 분류됩니다. 소프트웨어 부문은 급속한 인더스트리 4.0 채택 및 IoT 통합으로 2024년 41억 달러를 차지했습니다. 소프트웨어 기반 PLC는 실시간 모니터링, 예측 분석, 프로세스 최적화를 지원해 산업계 효율 향상과 조작 실수 최소화를 지원합니다. 시스템의 다운타임을 줄이고 생산 프로세스를 합리화하는 PLC의 역할은 스마트 제조가 기세를 올리면서 계속 확대되고 있습니다.

지역별로는 북미가 2024년 세계 PLC 시장에서 34.4%의 점유율을 차지했으며, 스마트 인프라 및 자동화 기술에 대한 투자 증가가 그 요인이 되고 있습니다. 미국은 이 지역 시장을 선도해 2024년에는 31억 달러를 창출했으며, CAGR 10.8%로 성장할 것으로 예측되고 있습니다. 인더스트리 4.0 이니셔티브의 확대 및 EV 생산에 대한 관심의 고조가 이 지역에서의 PLC 채용을 촉진하는 주요 요인입니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 인더스트리 4.0 및 디지털 트윈 구상의 채용

- 업계 전체의 자동화 수요 증가

- 산업용 로봇에 대한 수요 증가

- 노후화된 인프라의 업그레이드

- 전기자동차(EV) 산업의 상승

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 높은 투자 비용

- 사이버 보안 공격의 위협

- 규제 상황

- 기술 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 모듈러

- 컴팩트

- 랙 마운트

제6장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 하드웨어

- 중앙처리장치(CPU)

- 메모리 모듈

- 입력 모듈

- 출력 모듈

- 통신 모듈

- 전원 유닛

- 휴먼 머신 인터페이스(HMI)

- 기타

- 소프트웨어

- 서비스

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 항공우주 및 방위

- 자동차

- 화학

- 에너지 및 유틸리티

- 음식

- 헬스케어

- 제조업

- 광업 및 금속

- 석유 및 가스

- 운수

- 기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- ABB

- Bosch Rexroth

- Delta Electronics

- Eaton

- General Electric

- Honeywell International

- Keyence

- Mitsubishi Electric

- Omron

- Panasonic

- Phoenix Contact

- Rockwell Automation

- Schneider Electric

- Siemens

- Yokogawa Electric

The Global Programmable Logic Controller Market was valued at USD 11.7 billion in 2024 and is projected to grow at a CAGR of 10.4% from 2025 to 2034. The increasing adoption of Industry 4.0, digital twin technology, and automation-driven solutions is fueling market expansion. The rising demand for electric vehicles (EVs) is further accelerating growth, as PLC-based systems play a critical role in automating production lines and optimizing manufacturing efficiency. Automakers rely on PLC-driven solutions to streamline EV production, enhance scalability, and reduce downtime. Additionally, these systems are essential for battery manufacturing and complex assembly processes, ensuring maximum productivity.

Industry 4.0 initiatives, which integrate AI-driven analytics, machine communication, and cloud computing, are driving significant demand for advanced PLCs. These systems facilitate real-time data processing and seamless connectivity, making them indispensable for smart manufacturing. The integration of digital twin technology with PLC-based systems enables manufacturers to create virtual models for testing and optimizing performance without disrupting physical operations. As companies increasingly adopt digital twins for predictive maintenance and efficiency improvements, PLC manufacturers are focusing on developing solutions that align with these advancements. The growing need for intelligent automation across various industries ensures sustained demand for PLCs, positioning them as essential components of modern industrial ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.7 Billion |

| Forecast Value | $31.4 Billion |

| CAGR | 10.4% |

The market is segmented based on type into modular, compact, and rack-mounted PLCs. Among these, modular PLCs are expected to witness the highest growth, registering a CAGR of 11.1% during the forecast period. These PLCs offer superior scalability and flexibility, making them a preferred choice across industries, including manufacturing, energy, water treatment, and food processing. Their ability to minimize downtime by enabling faulty module replacements without disrupting entire systems drives their widespread adoption.

By end-use, the market is divided into aerospace and defense, automotive, chemicals, energy and utilities, food and beverages, healthcare, manufacturing, mining and metals, oil and gas, and transportation. The manufacturing sector accounted for over 20.9% of the total market share in 2024, driven by the increasing deployment of PLCs in smart factories and automated production lines. Modern PLC systems enhance efficiency through real-time data processing, predictive maintenance, and adaptive automation, making them integral to industrial advancements.

The market is also categorized by component into software, hardware, and services. The software segment accounted for USD 4.1 billion in 2024, driven by rapid Industry 4.0 adoption and IoT integration. Software-based PLCs support real-time monitoring, predictive analytics, and process optimization, helping industries improve efficiency and minimize operational errors. Their role in reducing system downtime and streamlining production processes continues to expand as smart manufacturing gains momentum.

Geographically, North America held a 34.4% share of the global PLC market in 2024, fueled by increased investments in smart infrastructure and automation technologies. The U.S. led the regional market, generating USD 3.1 billion in 2024, and is projected to grow at a CAGR of 10.8%. The expansion of Industry 4.0 initiatives and the rising focus on EV production are key factors driving PLC adoption in the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Adoption of industry 4.0 and digital twin initiatives

- 3.2.1.2 Growing demand for automation across industries

- 3.2.1.3 Rising demand for Industrial robotics

- 3.2.1.4 Upgradation of aging infrastructure

- 3.2.1.5 The rise of electric vehicles (EV) industry

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1.1 High investment costs

- 3.3.1.2 Threats of cybersecurity attacks

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Bn & Units)

- 5.1 Key trends

- 5.2 Modular

- 5.3 Compact

- 5.4 Rack mounted

Chapter 6 Market Estimates and Forecast, By Component, 2021 – 2034 (USD Bn & Units)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Central Processing Unit (CPU)

- 6.2.2 Memory modules

- 6.2.3 Input modules

- 6.2.4 Output modules

- 6.2.5 Communication modules

- 6.2.6 Power supply unit

- 6.2.7 Human Machine Interface (HMI)

- 6.2.8 Others

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Bn & Units)

- 7.1 Key trends

- 7.2 Aerospace & defence

- 7.3 Automotive

- 7.4 Chemical

- 7.5 Energy & utilities

- 7.6 Food & beverages

- 7.7 Healthcare

- 7.8 Manufacturing

- 7.9 Mining & metal

- 7.10 Oil & gas

- 7.11 Transportation

- 7.12 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Bosch Rexroth

- 9.3 Delta Electronics

- 9.4 Eaton

- 9.5 General Electric

- 9.6 Honeywell International

- 9.7 Keyence

- 9.8 Mitsubishi Electric

- 9.9 Omron

- 9.10 Panasonic

- 9.11 Phoenix Contact

- 9.12 Rockwell Automation

- 9.13 Schneider Electric

- 9.14 Siemens

- 9.15 Yokogawa Electric