|

시장보고서

상품코드

1699281

관절내 보충 요법 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Viscosupplementation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

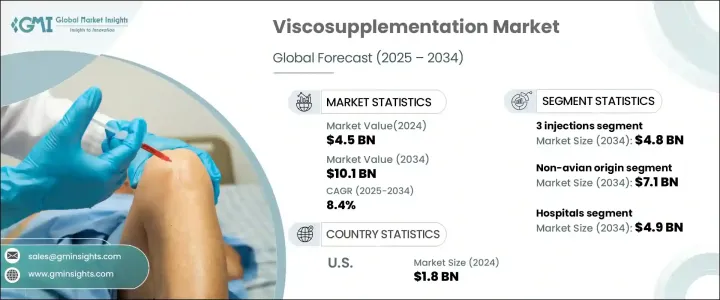

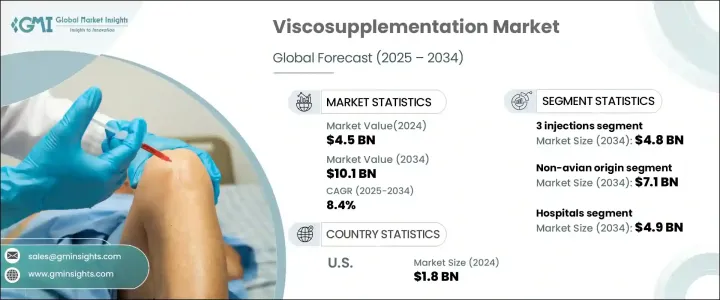

세계의 관절내 보충 요법 시장은 2024년에 45억 달러에 이르렀으며, 2025-2034년 연평균 복합 성장률(CAGR) 8.4%로 성장할 것으로 예측됩니다.

골관절염, 특히 무릎 골관절염의 유병률 증가는 첨단 치료 솔루션에 대한 수요를 계속 추진하고 있습니다. 비외과적 개입으로서 관절내 보충 요법은 관절의 가동성을 개선하고 통증을 완화하며 침습적 처치의 필요성을 지연시키는 능력이 있다고 널리 인지되고 있습니다. 고령자는 관절 퇴행 및 변형성 골관절염 관련 합병증에 걸리기 쉽기 때문에 고령화로 인해 시장은 급속히 확대되고 있습니다.

퇴행성 관절염 사례가 세계적으로 급증하는 가운데, 헬스케어 제공자도 환자도 마찬가지로 장기적인 증상 관리를 위해 관절내 보충 요법을 이용하게 되어 왔습니다. 이 치료법에서는 환부 관절에 히알루론산을 주입해 윤활성을 회복시키고 뻣뻣함을 줄여 가동성을 높입니다. 이 치료법은 회복에 소요되는 시간이 짧고 진통제에 대한 의존도가 낮기 때문에 환자들에게 선호되고 있습니다. 한편, 제제 기술이나 제품 순도의 진보가 계속 되고 있어 다양한 환자 그룹에서의 채용이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 45억 달러 |

| 예측 금액 | 101억 달러 |

| CAGR | 8.4% |

효능이 확대되어 생체 적합성이 향상된 차세대 비스코 보충제의 도입이 시장의 성장을 더욱 뒷받침하고 있습니다. 제조사들은 제품의 성능을 높이기 위해 지속적으로 기술 혁신을 하고 있으며, 관절내 보충 요법이 퇴행성 관절염 관리에 바람직한 선택지임을 확실히 하고 있습니다. 게다가 정부의 지원책, 헬스케어 지출 증가, 비외과적 치료 선택지에 대한 의식의 고조가, 시장의 궤도를 가속시키고 있습니다.

관절내 보충 요법 시장은 제품 유형별로 단회 주사, 3회 주사, 5회 주사로 구분됩니다. 이 중 3회 주사 부문은 2024년 매출액이 21억 달러로 시장을 독점하였고, 2034년에는 CAGR 8.5%를 기록해 48억 달러에 이를 것으로 예측되고 있습니다. 골관절염의 증상 관리 및 관절 기능의 회복에 효과적이기 때문에 표준적인 치료법이 되고 있습니다. 이 치료법은 구조화된 투여 스케줄로 인해 잦은 진료의 필요성을 최소화하면서 지속적인 증상 완화를 가져오기 때문에 의사들로부터 지지를 받고 있습니다. 투여의 간편함, 균형 잡힌 치료 기간, 일관된 임상 성적으로 인해 이 분야의 인기는 계속 높아지고 있습니다.

공급원별로 시장은 조류 유래와 비조류 유래의 점액 보충제로 분류되며, 비조류 유래 제품이 2024년 시장 점유율의 71.6%를 차지했습니다. 이 분야는 알레르기 반응에 대한 우려의 고조, 윤리적 배려, 제품의 일관성 향상 등을 배경으로 2034년에는 71억 달러에 이를 것으로 예측되고 있습니다. 비조류 유래 비스코 보충제는 순도가 높고 면역반응 위험이 낮기 때문에 환자에게도 헬스케어 공급자에게도 점점 선호되고 있습니다. 제조사가 알레르겐 프리 고순도 제제 개발에 주력하고 있기 때문에 합성 및 생물공학적인 대체품으로의 이행이 시장을 더욱 형성하고 있습니다.

북미의 관절내 보충 치료 시장은 2024년에 18억 달러에 이르렀습니다. 연구에 따르면 관절염은 여전히 가장 흔한 관절 장애이며 수백만 명이 이환하고 있습니다. 조사에 따르면 65세 이상의 43%가 골관절염에 이환되어 있으며, 그 주요 원인은 연골의 변성, 관절의 열화, 회복력 저하입니다. 효과적이고 저침습적인 해결책에 대한 수요가 증가하는 가운데 관절 내 보충요법은 골관절염 치료에 있어 중요한 치료 선택지로서의 입지를 계속 굳히고 있습니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 골관절염에 걸리기 쉬운 노인 인구 증가

- 저침습 치료에 대한 수요 증가

- 기술의 진보

- 스포츠 관련 상해 증가

- 업계의 잠재적 위험 및 과제

- 높은 치료비

- 대체 치료의 가용성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 단회 주사

- 3회 주사

- 5회 주사

제6장 시장 추계 및 예측 : 유래별(2021-2034년)

- 주요 동향

- 조류 유래

- 비조류 유래

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 정형외과 클리닉

- 외래수술센터(ASC)(ASCs)

- 기타 최종 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Anika Therapeutics

- APTISSEN

- Avanos

- Biotech Healthcare

- Bioventus

- Ferring Pharmaceuticals

- Fidia Pharma

- Premier Surgical

- Sanofi

- Seikagaku Corporation

- Stellar Pharmaceuticals

- TRB Pharma

- Zimmer Biomet

The Global Viscosupplementation Market reached USD 4.5 billion in 2024 and is projected to grow at a CAGR of 8.4% from 2025 to 2034. The rising prevalence of osteoarthritis, particularly knee osteoarthritis, continues to drive the demand for advanced treatment solutions. As a non-surgical intervention, viscosupplementation is gaining widespread recognition for its ability to improve joint mobility, alleviate pain, and delay the need for invasive procedures. The market is witnessing rapid expansion due to the aging population, as older individuals are more susceptible to joint degeneration and osteoarthritis-related complications.

With osteoarthritis cases surging globally, healthcare providers and patients alike are increasingly turning to viscosupplementation for long-term symptom management. The procedure involves injecting hyaluronic acid into the affected joints to restore lubrication, reduce stiffness, and enhance mobility. Patients prefer this treatment for its minimal recovery time and reduced dependence on pain medication. Meanwhile, ongoing advancements in formulation technologies and product purity are expanding adoption across diverse patient groups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.5 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 8.4% |

The introduction of next-generation viscosupplements with extended efficacy and improved biocompatibility is further fueling market growth. Manufacturers are continuously innovating to enhance product performance, ensuring that viscosupplementation remains a preferred choice for osteoarthritis management. Additionally, supportive government initiatives, rising healthcare expenditure, and increasing awareness about non-surgical treatment alternatives are accelerating the market's trajectory.

The viscosupplementation market is segmented by product type into single injection, three injections, and five injections. Among these, the three-injection segment dominated the market with USD 2.1 billion in revenue in 2024 and is expected to reach USD 4.8 billion by 2034, registering a CAGR of 8.5%. Its effectiveness in managing osteoarthritis symptoms and restoring joint function has made it the standard treatment approach. Physicians favor this regimen due to its structured dosing schedule, which provides sustained symptom relief while minimizing the need for frequent medical visits. The segment's popularity continues to rise due to its ease of administration, balanced treatment duration, and consistent clinical outcomes.

By source, the market is categorized into avian-origin and non-avian-origin viscosupplements, with non-avian-origin products accounting for 71.6% of the market share in 2024. This segment is projected to reach USD 7.1 billion by 2034, driven by growing concerns over allergic reactions, ethical considerations, and improved product consistency. Non-avian-origin viscosupplements offer enhanced purity and a lower risk of immune response, making them increasingly preferred by both patients and healthcare providers. The transition toward synthetic and bioengineered alternatives is further shaping the market as manufacturers focus on developing allergen-free, high-purity formulations.

North America viscosupplementation market reached USD 1.8 billion in 2024, as osteoarthritis cases continue to rise across the region. Studies indicate that arthritis remains the most common joint disorder, affecting millions of individuals, with osteoarthritis being the leading cause of disability among aging populations. Research shows that 43% of individuals aged 65 and above suffer from osteoarthritis, primarily due to cartilage degeneration, joint deterioration, and reduced resilience. As demand for effective, minimally invasive solutions grows, viscosupplementation continues to cement its position as a key treatment option in osteoarthritis care.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population prone to osteoarthritis

- 3.2.1.2 Rising demand for minimally invasive treatments

- 3.2.1.3 Technological advancements

- 3.2.1.4 Increasing sport-related injuries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Availability of alternative treatments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Single injection

- 5.3 3 injections

- 5.4 5 injections

Chapter 6 Market Estimates and Forecast, By Source of Origin, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Avian origin

- 6.3 Non-avian origin

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Orthopedic clinics

- 7.4 Ambulatory surgical centers (ASCs)

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anika Therapeutics

- 9.2 APTISSEN

- 9.3 Avanos

- 9.4 Biotech Healthcare

- 9.5 Bioventus

- 9.6 Ferring Pharmaceuticals

- 9.7 Fidia Pharma

- 9.8 Premier Surgical

- 9.9 Sanofi

- 9.10 Seikagaku Corporation

- 9.11 Stellar Pharmaceuticals

- 9.12 TRB Pharma

- 9.13 Zimmer Biomet