|

시장보고서

상품코드

1699289

눈 외상용 디바이스 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Ocular Trauma Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

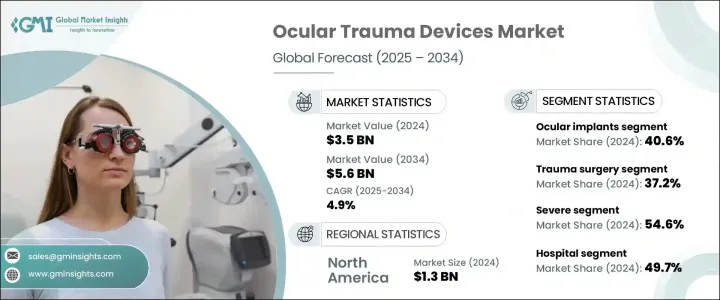

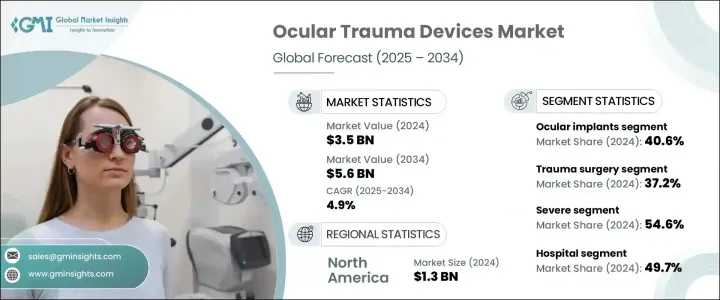

세계의 눈 외상용 디바이스 시장은 2024년에 35억 달러에 이르렀으며, 눈 외상 유병률 증가와 전문 치료 솔루션에 대한 요구 증가를 배경으로 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.9%를 나타낼 것으로 예측됩니다.

눈 외상은 여전히 공중 보건상의 심각한 관심사이며, 경미한 찰과상에서 심각한 관통 외상까지 다양한 사고가 발생하고 있으며, 급한 의료 개입이 필요합니다. 조기 진단의 진보, 이용 가능한 치료 옵션의 인지도 향상 최첨단 수술 기술의 채용이 시장 확대에 박차를 가하고 있습니다.

저침습 수술과 기술적으로 고도의 장치는 환자의 결과를 개선하고 회복 시간을 단축하며 전체적인 수술 효율을 높이는 데 중요한 역할을 하고 있습니다. 또한 정부의 이니셔티브와 세계 건강 관리 투자 증가는 안과 연구 개발 노력을 강화하고 보다 효과적인 외상 관리 솔루션의 도입으로 이어졌습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 35억 달러 |

| 예측 금액 | 56억 달러 |

| CAGR | 4.9% |

병원, 전문 클리닉, 외래수술센터(ASC)에서 눈 외상용 디바이스의 도입이 증가하고 있는 것이, 이 상승 경향을 촉진하는데 있어 매우 중요한 역할을 하고 있습니다.

제품 유형별로 볼 때, 눈 외상용 디바이스 시장은 수술 기구, 안구 내 렌즈(IOL), 눈 임플란트, 눈 점탄성 장치(OVD) 및 기타 관련 장비로 구분됩니다. 임플란트는 사고, 둔한 외상, 관통 외상으로 인한 구조적 손상 후 시력 회복과 안구의 무결성 유지에 중요한 역할을 하고 있습니다.

시장은 또한 용도별로 외상 수술, 망막 박리, 백내장 수술, 녹내장 관리, 기타 처치로 분류됩니다. 심각한 외상 관리에는 출혈 통제, 구조 수리 및 시력 회복이 포함되어 있기 때문에 정밀 수술 기구를 사용해야 합니다.

미국은 눈 외상용 디바이스 업계에서 여전히 압도적인 힘을 자랑하고 있으며, 2024년 시장 규모는 12억 3,000만 달러였고, 2032년에는 18억 달러에 이를 것으로 예상되고 있습니다. 이와 같은 안과 기술 혁신의 최전선에 있습니다. 관민 양 부문으로부터의 투자가 획기적인 연구를 뒷받침해, 제조업체가 외상성 눈 손상 치료를 위한 차세대 솔루션을 개발하는 것을 가능하게 하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 눈 외상 증가

- 기술의 진보

- 의식의 고조와 조기 진단

- 유리한 정부의 대처와 보험 적용

- 업계의 잠재적 위험 및 과제

- 고액의 치료비

- 숙련된 의료 전문가의 부족

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 상환 시나리오

- 향후 시장 동향

- 갭 분석

- 기술 전망

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 벤더 매트릭스 분석

- 전략 대시보드

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 수술 기구

- 인공수정체(IOLs)

- 안구 임플란트

- 안과용 점탄성 디바이스(OVDs)

- 기타 제품

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 외상 수술

- 망막 박리

- 백내장 수술

- 녹내장 관리

- 기타 용도

제7장 시장 추계·예측 : 외상 중증도별(2021-2034년)

- 주요 동향

- 경증

- 보통

- 중증

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 안과 클리닉

- 외래수술센터(ASC)

- 기타 최종 사용

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 아시아태평양

- 일본

- 중국

- 인도

- 한국

- 호주

- 라틴아메리카

- 브라질

- 아르헨티나

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Alcon

- Bausch Lomb

- Carl Zeiss Meditec

- CooperVision

- Essilor Instruments

- Haag-Streit Group

- Innovative Optics

- IRIDEX Corporation

- Johnson &Johnson Vision

- Leica Microsystems

- Optos

- Sonomed Escalon

- Topcon Corporation

The Global Ocular Trauma Devices Market reached USD 3.5 billion in 2024 and is projected to expand at a CAGR of 4.9% from 2025 to 2034, driven by the rising prevalence of eye injuries and the growing need for specialized treatment solutions. Ocular trauma remains a significant public health concern, with incidents ranging from minor abrasions to severe penetrating injuries that require immediate medical intervention. Advancements in early diagnosis, increased awareness of available treatment options, and the adoption of cutting-edge surgical techniques are fueling market expansion. As healthcare providers prioritize rapid and effective intervention for eye trauma cases, the demand for high-precision trauma devices continues to climb.

Minimally invasive procedures and technologically advanced devices are playing a crucial role in improving patient outcomes, reducing recovery time, and enhancing overall surgical efficiency. Innovations such as bioengineered ocular implants, robotic-assisted eye surgeries, and ophthalmic viscoelastic devices (OVDs) are gaining traction, further contributing to the market's positive trajectory. Moreover, government initiatives and increased healthcare investments worldwide are strengthening ophthalmic research and development efforts, leading to the introduction of more effective trauma management solutions. The integration of artificial intelligence in diagnostic tools and surgical systems is further streamlining treatment protocols, offering enhanced precision and efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 4.9% |

The increasing adoption of ocular trauma devices across hospitals, specialty clinics, and ambulatory surgical centers is playing a pivotal role in driving this upward trend. With a growing number of trauma-related surgeries performed globally, healthcare facilities are actively upgrading their ophthalmic equipment, leading to higher adoption of innovative solutions.

By product type, the ocular trauma devices market is segmented into surgical instruments, intraocular lenses (IOLs), ocular implants, ophthalmic viscoelastic devices (OVDs), and other related devices. Ocular implants captured a 40.6% market share in 2024, propelled by the rising number of severe trauma cases necessitating secondary solutions such as artificial lenses and retinal prostheses. These implants play a vital role in restoring vision and maintaining ocular integrity following structural damage caused by accidents, blunt force injuries, or penetrating trauma. The increasing prevalence of complex ocular injuries is fueling demand for specialized implants designed to address severe cases effectively.

The market is also categorized by application into trauma surgery, retinal detachment, cataract surgery, glaucoma management, and other procedures. Trauma surgery accounted for a 37.2% market share in 2024, driven by the rising incidence of blunt force trauma, penetrating wounds, and chemical burns requiring advanced surgical interventions. Managing severe ocular trauma involves hemorrhage control, structural repairs, and visual function restoration, necessitating the use of high-precision surgical tools. The growing demand for sophisticated trauma management solutions is reinforcing the market's expansion.

The United States remains a dominant force in the ocular trauma devices industry, with the market valued at USD 1.23 billion in 2024 and expected to generate USD 1.8 billion by 2032. As a global leader in medical technology, the country is at the forefront of ophthalmic innovations, including robotic eye surgeries, bioengineered implants, and minimally invasive surgical tools. Investments from both private and public sectors are fueling groundbreaking research, enabling manufacturers to develop next-generation solutions for treating traumatic eye injuries. With continuous advancements in ocular trauma care, the market is set to witness sustained growth in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of ocular trauma

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing awareness and early diagnosis

- 3.2.1.4 Favorable government initiatives and insurance coverage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Technology landscape

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Vendor matrix analysis

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical instruments

- 5.3 Intraocular lenses (IOLs)

- 5.4 Ocular implants

- 5.5 Ophthalmic viscoelastic devices (OVDs)

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Trauma surgery

- 6.3 Retinal detachment

- 6.4 Cataract surgery

- 6.5 Glaucoma management

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Trauma Severity, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Mild

- 7.3 Moderate

- 7.4 Severe

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ophthalmic clinics

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alcon

- 10.2 Bausch + Lomb

- 10.3 Carl Zeiss Meditec

- 10.4 CooperVision

- 10.5 Essilor Instruments

- 10.6 Haag-Streit Group

- 10.7 Innovative Optics

- 10.8 IRIDEX Corporation

- 10.9 Johnson & Johnson Vision

- 10.10 Leica Microsystems

- 10.11 Optos

- 10.12 Sonomed Escalon

- 10.13 Topcon Corporation