|

시장보고서

상품코드

1699343

로봇 소프트웨어 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Robotic Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

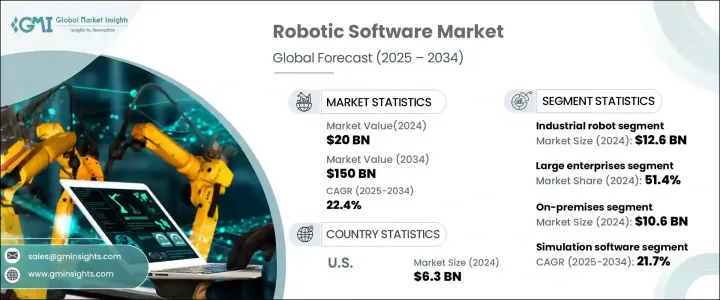

세계의 로봇 소프트웨어 시장은 2024년 200억 달러로 평가되었으며 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 22.4%를 나타낼 것으로 예상됩니다.

이 성장의 원동력이 되는 것은 로봇 소프트웨어에 대한 인공지능과 머신러닝의 통합이 진행되고 있는 것과 협동 로봇 수요가 각 업계에서 높아지고 있는 것입니다. 진정한 자동화 솔루션에 많은 투자를 하고 있습니다. AI와 ML은 데이터 중심의 의사 결정, 역동적인 환경에 적응, 복잡한 작업의 고정밀 실행을 가능하게 함으로써 로봇 시스템에 변화를 가져오고 있습니다.

이러한 진보는 제조, 건강 관리, 물류, 농업 등의 분야에서 특히 두드러지며, 자동화에 의해 효율이 최적화되어 전반적인 생산고가 향상되고 있습니다. 정부와 기업이 스마트 로봇에 대한 투자를 강화하고 있으며, 시장 확대를 더욱 가속화하고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 200억 달러 |

| 예측 금액 | 1,500억 달러 |

| CAGR | 22.4% |

시장은 로봇 유형에 따라 구분되며, 산업용 로봇과 서비스 로봇이 2대 카테고리입니다. 또한 성능을 최적화하고 다운타임을 최소화하고 제품 품질을 향상시킬 수 있습니다. 경계에 원활한 통합을 실현할 수 있습니다. 산업계에서는 증가하는 수요에 대응해 경쟁력을 유지하기 위해 자동화를 우선하는 경향이 강해지고 있어 산업용 로봇 소프트웨어의 채용은 대폭 증가할 전망입니다.

기업 규모는 로봇 소프트웨어 시장을 형성하는 또 다른 중요한 부문이며 대기업과 중소기업(SME)을 모두 포함합니다. 2024년 시장 점유율은 대기업이 51.4%를 차지했으며, 로봇 솔루션 채용에 있어 대기업이 지배적인 역할을 담당하고 있음을 부각하고 있습니다. 이러한 조직은 여러 생산 라인, 창고 및 물류 센터를 운영하며, 원활한 조정, 작업 관리 및 프로세스 최적화를 위한 고급 소프트웨어가 필요합니다. 로봇 소프트웨어는 대기업이 성능을 모니터링하고, 반복 작업을 자동화하고, 확장성을 강화할 수 있게 하고, 궁극적으로 효율성을 높이고 비용을 절감할 수 있습니다. 한편, 중소기업은 운영 민첩성을 향상시키고 인건비를 최소화하고 진화하는 비즈니스 환경에서 보다 효과적으로 경쟁하기 위해 로봇의 자동화에 대한 투자를 늘리고 있습니다.

2024년 미국의 로봇 소프트웨어 시장 규모는 63억 달러로, 자동화와 고급 로봇 공학의 도입에 있어 이 나라의 리더십이 반영되었습니다. 제조, 헬스케어, 물류 등 업계가 지능형 오토메이션을 채용하는 가운데 로봇 소프트웨어 솔루션 수요는 계속 급증하고 있습니다. 비용 효율적이고 효율적이고 정확한 제조 공정를 요구하는 움직임은 AI를 탑재한 로봇 공학을 도입하여 생산 품질을 향상시키고 인적 개입을 줄이기 위해 기업을 추진하고 있습니다. 미국 기업이 지능형 자동화를 통한 운영 최적화를 모색하는 동안 미국은 세계 로봇 소프트웨어의 전망을 형성하는 중요한 기업로 남아 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴적 혁신

- 향후 전망

- 제조업체

- 유통업체

- 공급업체의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 로봇 소프트웨어에 AI와 ML의 통합 확대

- 협동 로봇 수요 증가

- 각 업계에서 자동화의 진전

- 다양한 분야에 로봇 도입 증가

- 업계의 잠재적 위험 및 과제

- 고액의 초기 투자 비용

- 복잡한 기존 시스템과의 통합

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계·예측 : 소프트웨어 유형별(2021-2034년)

- 주요 동향

- 시뮬레이션 소프트웨어

- 네비게이션 및 매핑 소프트웨어

- 데이터 분석 및 관리 소프트웨어

- 비전 소프트웨어

- 예측적 유지보수 소프트웨어

- 기타

제6장 시장 추계·예측 : 로봇 유형별(2021-2034년)

- 주요 동향

- 산업용 로봇

- 서비스 로봇

제7장 시장 추계·예측 : 배포 모드별(2021-2034년)

- 주요 동향

- 온프레미스

- 클라우드

제8장 시장 추계·예측 : 기업 규모별(2021-2034년)

- 주요 동향

- 대기업

- 중소기업(SME)

제9장 시장 추계·예측 : 최종 사용자 산업별(2021-2034년)

- 주요 동향

- 제조

- 자동차

- 헬스케어

- 운송 및 물류

- BFSI

- 소매 및 E-Commerce

- 기타

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- ABB Ltd

- Amazon Robotics(Amazon.com, Inc.)

- Autodesk, Inc.

- Blue Prism Group plc

- Boston Dynamics

- Clearpath Robotics

- Cognex Corporation

- Denso Corporation

- FANUC Corporation

- Hanson Robotics

- iRobot Corporation

- KUKA AG

- Mitsubishi Electric Corporation

- NVIDIA Corporation

- Omron Corporation

- Open Robotics(OSRF)

- Rockwell Automation, Inc.

- Siemens AG

- SoftBank Robotics

- Teradyne Inc.

- UiPath Inc.

- Universal Robots A/S

- Vecna Robotics

- Yaskawa Electric Corporation

The Global Robotic Software Market was valued at USD 20 billion in 2024 and is expected to expand at a CAGR of 22.4% from 2025 to 2034. This growth is being driven by the increasing integration of artificial intelligence and machine learning into robotic software, as well as the rising demand for collaborative robots across industries. Businesses are investing heavily in intelligent automation solutions to streamline operations, reduce costs, and enhance productivity. AI and ML are transforming robotic systems by enabling them to make data-driven decisions, adapt to dynamic environments, and perform complex tasks with greater precision.

These advancements are particularly evident in sectors such as manufacturing, healthcare, logistics, and agriculture, where automation is optimizing efficiency and improving overall output. The growing reliance on robotics for labor-intensive and repetitive processes is fueling the demand for advanced software solutions capable of managing, analyzing, and enhancing robot performance. Additionally, governments and enterprises worldwide are ramping up investments in smart robotics, further accelerating market expansion. The rise of cloud-based robotics, enhanced connectivity, and seamless software integration is making robotic applications more scalable and accessible, opening new opportunities for businesses of all sizes to leverage automation for competitive advantage.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20 Billion |

| Forecast Value | $150 Billion |

| CAGR | 22.4% |

The market is segmented based on the type of robot, with industrial robots and service robots being the two primary categories. In 2024, industrial robot software dominated the market, accounting for USD 12.6 billion. These systems are essential for automating manufacturing and assembly processes, reducing errors, and improving operational efficiency. Industrial robot software incorporates powerful data analytics tools that provide real-time insights into robotic operations, allowing businesses to optimize performance, minimize downtime, and enhance product quality. Additionally, features such as simulation and visualization tools enable users to anticipate and mitigate potential issues before deployment, ensuring seamless integration into production environments. As industries increasingly prioritize automation to meet growing demands and maintain a competitive edge, the adoption of industrial robot software is set to rise significantly.

Enterprise size is another crucial segment shaping the robotic software market, encompassing both large enterprises and small and medium-sized enterprises (SMEs). Large enterprises accounted for a 51.4% market share in 2024, highlighting their dominant role in adopting robotic solutions. These organizations operate multiple production lines, warehouses, and logistics centers, necessitating advanced software for seamless coordination, task management, and process optimization. Robotic software enables large companies to monitor performance, automate repetitive tasks, and enhance scalability, ultimately leading to higher efficiency and cost savings. Meanwhile, SMEs are also increasingly investing in robotic automation to improve operational agility, minimize labor costs, and compete more effectively in an evolving business landscape.

The U.S. robotic software market was valued at USD 6.3 billion in 2024, reflecting the country's leadership in automation and advanced robotics adoption. With industries such as manufacturing, healthcare, and logistics embracing intelligent automation, demand for robotic software solutions continues to surge. The push for cost-effective, efficient, and precise manufacturing processes is driving businesses to implement AI-powered robotics to enhance production quality and reduce human intervention. As American companies seek to optimize operations through intelligent automation, the U.S. remains a key player in shaping the global robotic software landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing integration of AI and ML into robotic software

- 3.6.1.2 Rising demand for collaborative robots

- 3.6.1.3 Increased automation across industries

- 3.6.1.4 Raising the adoption of robots across various sectors

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investments

- 3.6.2.2 Complexes in integration with existing systems

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Software Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Simulation software

- 5.3 Navigation and mapping software

- 5.4 Data analytics and management software

- 5.5 Vision software

- 5.6 Predictive maintenance software

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Robot Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Industrial robot

- 6.3 Service robot

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Large enterprise

- 8.3 Small and Medium Enterprises (SME)

Chapter 9 Market Estimates & Forecast, By End-use Industry, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Manufacturing

- 9.3 Automotive

- 9.4 Healthcare

- 9.5 Transportation and logistics

- 9.6 BFSI

- 9.7 Retail & e-commerce

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABB Ltd

- 11.2 Amazon Robotics (Amazon.com, Inc.)

- 11.3 Autodesk, Inc.

- 11.4 Blue Prism Group plc

- 11.5 Boston Dynamics

- 11.6 Clearpath Robotics

- 11.7 Cognex Corporation

- 11.8 Denso Corporation

- 11.9 FANUC Corporation

- 11.10 Hanson Robotics

- 11.11 iRobot Corporation

- 11.12 KUKA AG

- 11.13 Mitsubishi Electric Corporation

- 11.14 NVIDIA Corporation

- 11.15 Omron Corporation

- 11.16 Open Robotics (OSRF)

- 11.17 Rockwell Automation, Inc.

- 11.18 Siemens AG

- 11.19 SoftBank Robotics

- 11.20 Teradyne Inc.

- 11.21 UiPath Inc.

- 11.22 Universal Robots A/S

- 11.23 Vecna Robotics

- 11.24 Yaskawa Electric Corporation