|

시장보고서

상품코드

1699360

헬스케어 데이터 수익화 솔루션 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Healthcare Data Monetization Solutions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

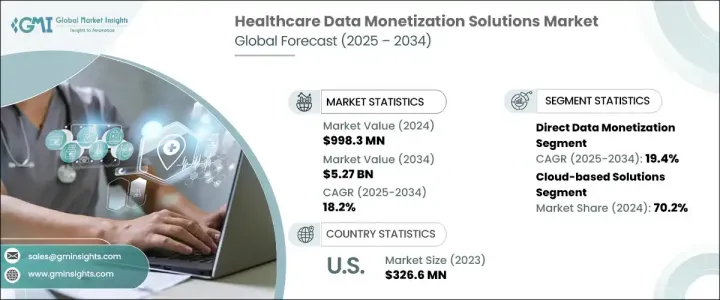

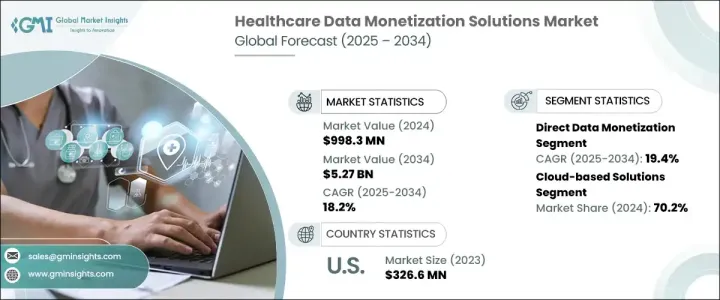

세계의 헬스케어 데이터 수익화 솔루션 시장은 2024년에는 9억 9,830만 달러를 기록했고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 18.2%를 나타낼 것으로 예측됩니다.

헬스케어 업계는 디지털 혁명의 한가운데에 있으며, 데이터 수익화가 중요한 촉진요인으로 부상하고 있습니다. 기업은 이 데이터의 가치를 인식해, 새로운 수익원의 개발, 환자 케어의 최적화, 업무 효율의 향상에 활용하고 있습니다.

헬스케어 데이터 수익화 솔루션에 대한 수요는 디지털 플랫폼의 진보, 클라우드 기반 서비스의 보급, 기술 공급업체와 의료기관의 전략적 제휴에 의해 높아지고 있습니다. 이러한 인사이트를 통해 제약회사, 보험회사, 의료 제공자는 데이터 주도의 의사결정을 실시해 업무를 합리화하고 환자의 결과를 개선할 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 9억 9,830만 달러 |

| 예측 금액 | 52억 7,000만 달러 |

| CAGR | 18.2% |

직접 데이터 수익화 분야는 대폭적인 성장이 예상되며 예측 기간 중 CAGR은 19.4%를 나타낼 것으로 예측됩니다. 판매, 분석 서비스 제공, 연구 목적 데이터세트의 라이선스 제공을 통해 수익을 올릴 수 있습니다. 한편, 간접 데이터 수익화는 여전히 중요한 전략이며, 기업은 데이터 인사이트를 활용하여 마케팅 활동을 강화하고 고객 참여를 촉진하고 비즈니스 의사 결정 프로세스를 개선합니다.

헬스케어 데이터 수익화 시장에서는 클라우드 기반 솔루션이 계속 우위를 차지하고 있으며, 2024년 시장 점유율은 70%에 달했습니다. 클라우드 기반 플랫폼은 의료 서비스 제공자가 원격으로 데이터를 관리하고 분석할 수 있도록 지원하므로 값비싼 온프레미스 인프라가 필요하지 않습니다.

2022년 미국의 헬스케어 데이터 수익화 솔루션 시장 규모는 2억 8,020만 달러로, 북미를 선도했습니다. 미국 전역의 의료 기관은 AI 기반 분석, 예측 모델링, 블록체인 기술을 활용하여 환자 데이터를 안전하고 규정을 준수하면서 수익화하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전자 차트(EHR)의 채용 확대

- 디지털 헬스 솔루션의 보급

- 데이터 분석의 기술적 진보

- 디지털 헬스 수익화 프로젝트를 합리화하는 AI 주도형 솔루션의 역동적인 채용

- 업계의 잠재적 위험 및 과제

- 규제상의 제약

- 데이터 프라이버시와 보안에 대한 우려

- 성장 촉진요인

- 성장 가능성 분석

- 기술적 전망

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 직접 데이터 수익화

- 간접 데이터 수익화

제6장 시장 추계·예측 : 전개 유형별(2021-2034년)

- 주요 동향

- 온프레미스

- 클라우드

제7장 시장 추계·예측 : 용도별(2021-2032년)

- 주요 동향

- 예측 분석 및 질병 관리

- 인구 건강 관리

- 수익 주기 관리

- 정밀의학

- 기타 용도

제8장 시장 추계·예측 : 데이터 유형별(2021-2034년)

- 주요 동향

- 임상 데이터

- 청구 데이터

- EHR 데이터

- 게놈 데이터

- 기타 데이터 유형

제9장 시장 추계·예측 : 최종 용도별(2021-2032년)

- 제약 및 생명공학 기업

- 헬스케어 지불자

- 헬스케어 제공자

- 의료기술기업

- 기타 최종 용도

제10장 시장 추계·예측 : 지역별(2021-2032년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Accenture

- H1

- IBM

- Infor

- Innovaccer

- LexisNexis Risk Solutions

- Microsoft

- Oracle

- Salesforce

- SAS Institute

- Siemens Healthineers

- Snowflake

- Thoughtspot

- Verato

The Global Healthcare Data Monetization Solutions Market was valued at USD 998.3 million in 2024 and is projected to grow at a CAGR of 18.2% between 2025 and 2034. The healthcare industry is undergoing a digital revolution, and data monetization is emerging as a crucial growth driver. With the increasing adoption of electronic health records (EHRs), AI-powered diagnostics, and connected medical devices, healthcare institutions are generating vast amounts of data. Companies are recognizing the value of this data, using it to develop new revenue streams, optimize patient care, and enhance operational efficiency.

The demand for healthcare data monetization solutions is being fueled by advancements in digital platforms, the proliferation of cloud-based services, and strategic collaborations between technology providers and healthcare organizations. As healthcare systems generate and store an unprecedented amount of patient data, businesses are leveraging analytics, AI, and machine learning to extract actionable insights. These insights are enabling pharmaceutical companies, insurers, and healthcare providers to make data-driven decisions, streamline operations, and improve patient outcomes. With regulatory bodies enforcing stringent compliance measures, organizations are investing in secure, scalable, and compliant data monetization solutions to remain competitive in the evolving market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $998.3 Million |

| Forecast Value | $5.27 Billion |

| CAGR | 18.2% |

The direct data monetization segment is expected to witness substantial growth, with a projected CAGR of 19.4% during the forecast period. Businesses are increasingly capitalizing on their proprietary data by developing new services, optimizing product offerings, and improving operational efficiencies. Direct monetization allows healthcare organizations to generate revenue by selling de-identified patient data, offering analytics-as-a-service, and licensing datasets for research purposes. Meanwhile, indirect data monetization remains a critical strategy, as companies utilize data insights to enhance marketing efforts, drive customer engagement, and improve business decision-making processes.

Cloud-based solutions continue to dominate the healthcare data monetization market, holding a 70% market share in 2024. The growing reliance on cloud technology stems from its ability to offer cost-effective, scalable, and easily accessible solutions. Cloud-based platforms empower healthcare providers to manage and analyze data remotely, eliminating the need for expensive on-premises infrastructure. With automatic updates, enhanced security features, and seamless integration with AI-driven analytics tools, cloud-based data monetization solutions are revolutionizing how the healthcare sector manages and leverages data assets.

The U.S. Healthcare Data Monetization Solutions Market was valued at USD 280.2 million in 2022 and continues to lead North America. The country's well-established healthcare infrastructure, coupled with its early adoption of digital transformation initiatives, has accelerated the demand for data-driven solutions. Healthcare institutions across the U.S. are leveraging AI-powered analytics, predictive modeling, and blockchain technology to monetize patient data securely and compliantly. As the healthcare sector evolves, data monetization is becoming an integral component of revenue generation strategies, positioning the U.S. as a frontrunner in this rapidly expanding market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of electronic health records (EHRs)

- 3.2.1.2 Growing adoptability of digital health solutions

- 3.2.1.3 Technological advancement in data analysis

- 3.2.1.4 Dynamic adoption of AI-driven solutions streamlining digital health monetization projects

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory constraints

- 3.2.2.2 Data privacy and security concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technological landscape

- 3.5 Regulatory landscape

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Direct data monetization

- 5.3 Indirect data monetization

Chapter 6 Market Estimates and Forecast, By Deployment Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Predictive analytics and disease management

- 7.3 Population health management

- 7.4 Revenue cycle management

- 7.5 Precision medicine

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By Data Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Clinical data

- 8.3 Claims data

- 8.4 EHR data

- 8.5 Genomic data

- 8.6 Other data types

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2032 ($ Mn)

- 9.1 Pharmaceutical and biotechnology companies

- 9.2 Healthcare payers

- 9.3 Healthcare providers

- 9.4 Medical technology companies

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2032 ($ Mn

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Accenture

- 11.2 Google

- 11.3 H1

- 11.4 IBM

- 11.5 Infor

- 11.6 Innovaccer

- 11.7 LexisNexis Risk Solutions

- 11.8 Microsoft

- 11.9 Oracle

- 11.10 Salesforce

- 11.11 SAS Institute

- 11.12 Siemens Healthineers

- 11.13 Snowflake

- 11.14 Thoughtspot

- 11.15 Verato