|

시장보고서

상품코드

1699400

디지털 헬스 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Digital Health Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

세계 디지털 헬스 시장은 2024년 3,129억 달러로 2025년부터 2034년까지 연평균 21.2%의 성장률을 보일 것으로 예상됩니다.

이러한 놀라운 성장은 헬스케어 분야에서 최첨단 디지털 기술이 통합되고 있기 때문입니다. 인공지능(AI), 빅데이터 분석, 클라우드 컴퓨팅, 사물인터넷(IoT)은 산업을 변화시키고, 효율성을 높이고, 환자 치료를 향상시키고 있습니다. 접근성 향상, 비용 효율적인 치료, 실시간 환자 모니터링의 필요성에 힘입어 디지털 헬스 솔루션에 대한 수요는 지속적으로 증가하고 있습니다. 디지털 헬스케어 솔루션의 급속한 발전은 업무 효율성을 개선할 뿐만 아니라 환자 참여를 재정의하고 보다 개인화된 데이터 기반 의료 접근 방식을 위한 길을 열어주고 있습니다.

전 세계 정부와 민간 투자자들이 디지털 헬스 이니셔티브에 막대한 자금을 지원하면서 시장 확대가 더욱 가속화되고 있습니다. 원격의료, AI 기반 진단, 디지털 치료법을 지원하는 강력한 정책적 프레임워크는 의료 서비스 제공의 재편에 있어 매우 중요한 역할을 하고 있습니다. 커넥티드 디바이스와 모바일 헬스(mHealth) 애플리케이션의 등장은 환자 행동에 큰 영향을 미치고 있으며, 예방 의료 및 원격의료 모델로 전환을 촉진하고 있습니다. 또한, 만성질환의 증가와 고령화로 인해 디지털 헬스 플랫폼에 대한 수요가 증가하고 있으며, 이는 현대의 헬스케어 생태계에 필수적인 요소로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 3,129억 달러 |

| 예상 금액 | 2조 1,900억 달러 |

| CAGR | 21.2% |

디지털 헬스 시장은 하드웨어, 소프트웨어, 서비스의 세 가지 핵심 요소로 분류됩니다. 서비스 부문은 2024년 1,228억 달러로 평가되며, 2034년까지 연평균 21.3%로 성장할 것으로 예상됩니다. 이러한 성장은 원격 환자 모니터링, 원격의료, 헬스케어 분석에 대한 수요가 급증하고 있으며, AI 및 IoT와 같은 첨단 기술의 통합을 통해 디지털 의료 서비스는 업무를 간소화하고, 의료 서비스를 강화하며, 환자와 의료진의 원활한 상호 작용을 촉진하고 있습니다. 의료 기관이 워크플로우를 최적화하고 환자 결과를 개선하기 위해 노력하는 가운데, 디지털 서비스는 효율적이고 능동적인 의료 개입을 가능하게 하는 중요한 역할을 하고 있습니다.

원격의료, 모바일 헬스(모바일 헬스), 건강 분석, 디지털 헬스 시스템은 여전히 업계 발전의 최전선에 있습니다. 원격의료 분야는 2024년 시장 점유율의 43.1%를 차지했으며, 이는 가상 진료, 원격 진단, 원격의료 플랫폼에 대한 의존도가 높아짐에 따른 것입니다. COVID-19 사태는 이러한 기술의 채택을 가속화하고, 접근 가능하고 확장 가능한 헬스케어 솔루션의 필요성을 강조했습니다. 그 결과, 의료 서비스 제공자들은 전 세계적으로 원격의료 서비스를 통합하고, 도달 범위를 확장하고, 환자가 적시에 비용 효율적인 의료 서비스를 받을 수 있도록 의료 접근성을 높이고 있습니다.

미국의 디지털 헬스케어 시장은 2024년 1,236억 달러 규모에 달했으며, 2025-2034년 연평균 20.7%의 성장률을 기록할 것으로 전망됩니다. 미국은 강력한 규제 프레임워크, 높은 투자 수준, 첨단 디지털 인프라를 바탕으로 디지털 헬스케어 도입의 세계 리더로 자리매김하고 있으며, AI 기반 진단 도구, 원격 환자 모니터링 솔루션, 데이터 기반 헬스케어 모델을 광범위하게 도입하여 미국 시장에서의 우위를 공고히 하고 있습니다. 미국 시장에서의 우위를 확고히 하고 있습니다. 차세대 기술의 통합이 진행되고 가치 기반 의료가 강력하게 추진되는 가운데, 미국의 디지털 의료 분야는 지속적인 성장을 이루며 세계 시장의 선두주자로서의 입지를 강화할 것으로 보입니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 원격 환자 모니터링 서비스에 대한 수요 증가

- 스마트폰 보급과 인터넷 접속 증가

- 디지털 헬스의 정부 적극적인 대처와 자금 제공

- 벤처 캐피털에서 투자 증가

- 업계의 잠재적 리스크·과제

- 데이터 프라이버시와 보안에 관한 우려

- 높은 도입 비용

- 성장 촉진요인

- 성장 가능성 분석

- 시장 진입 상황

- 규제 상황

- 미국

- 유럽

- 투자 분석 : 지역별

- 미국

- 유럽

- 아시아태평양

- 인수합병 상황

- 상환 시나리오

- 디지털 헬스 프로젝트/이니셔티브

- 기술 상황

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 시장 매트릭스 분석

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정과 예측 : 구성요소별, 2021-2034년

- 주요 동향

- 하드웨어

- 소프트웨어

- 클라우드 기반

- 온프레미스

- 서비스

제6장 시장 추정과 예측 : 기술별, 2021-2034년

- 주요 동향

- 텔레헬스 케어

- 텔레케어

- 활동 모니터링

- 원격 복약 관리

- 원격의료

- LTC 모니터링

- 비디오 상담

- 텔레케어

- 모바일 헬스(mHealth)

- 웨어러블과 접속된 의료기기

- 혈압 모니터

- 심박수 모니터

- 혈당치 모니터

- 산소포화도측정기

- 수면 트래커

- 신경 모니터

- 기타 웨어러블과 접속된 의료기기

- 모바일 헬스(mHealth) 앱

- 의료 앱

- 여성 건강 앱

- 만성질환 관리 앱

- 개인 건강 기록 앱

- 투약 관리 앱

- 원격 모니터링 앱

- 기타 의료 앱

- 피트니스 앱

- 의료 앱

- 웨어러블과 접속된 의료기기

- 건강 분석

- 예측 분석

- 처방적 분석

- 기술적 분석

- 디지털 헬스 시스템

- 전자건강기록(EHR)

- 전자 처방 시스템

제7장 시장 추정과 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 의료 제공자

- 환자

- 지불자

- 기타 최종 용도

제8장 시장 추정과 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제9장 기업 개요

- Accenture

- AMD Global Telemedicine

- American Well(Amwell)

- Athenahealth

- Capsa Healthcare

- Eagle Telemedicine

- Firstbeat Technologies

- GE Healthcare

- Health Catalyst

- Honeywell International

- IBM

- iHealth Lab

- Koninklijke Philips N.V.

- McKesson Corporation

- Oracle(Cerner Corporation)

- Qualcomm Technologies

- Teladoc Health

- Veradigm LLC(Allscripts Healthcare Solutions)

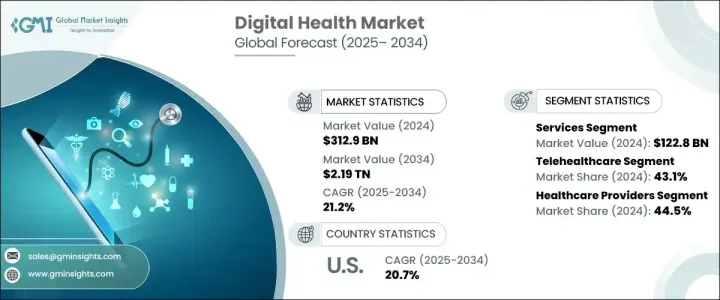

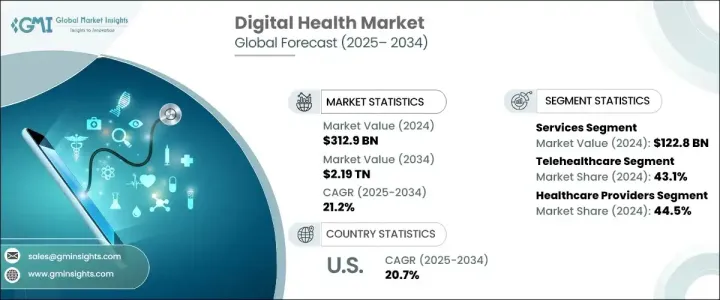

The Global Digital Health Market was valued at USD 312.9 billion in 2024 and is poised to expand at a CAGR of 21.2% between 2025 and 2034. This remarkable growth stems from the increasing integration of cutting-edge digital technologies in healthcare. Artificial intelligence (AI), big data analytics, cloud computing, and the Internet of Things (IoT) are transforming the industry, driving efficiency, and enhancing patient care. The demand for digital health solutions continues to surge, fueled by the need for improved accessibility, cost-effective treatments, and real-time patient monitoring. The rapid evolution of digital healthcare solutions is not just improving operational efficiency but also redefining patient engagement, paving the way for more personalized and data-driven medical approaches.

Governments and private investors worldwide are heavily funding digital health initiatives, further accelerating the market's expansion. Strong policy frameworks supporting telehealth adoption, AI-driven diagnostics, and digital therapeutics are playing a pivotal role in reshaping healthcare delivery. The rise of connected devices and mobile health (mHealth) applications has significantly influenced patient behaviors, prompting a shift toward preventive and remote care models. Additionally, the increasing prevalence of chronic diseases and aging populations has heightened the demand for digital health platforms, making them indispensable components of modern healthcare ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $312.9 Billion |

| Forecast Value | $2.19 trillion |

| CAGR | 21.2% |

The digital health market is categorized into three core components: hardware, software, and services. The services segment, valued at USD 122.8 billion in 2024, is expected to grow at a CAGR of 21.3% through 2034. This expansion is driven by the soaring demand for remote patient monitoring, telehealth, and healthcare analytics. With the integration of advanced technologies such as AI and IoT, digital health services are streamlining operations, enhancing care delivery, and fostering seamless patient-provider interactions. As healthcare organizations seek to optimize workflows and improve patient outcomes, digital services are becoming a critical enabler of efficient and proactive medical interventions.

Telehealthcare, mobile health (mHealth), health analytics, and digital health systems remain at the forefront of industry advancements. The telehealthcare segment accounted for 43.1% of the market share in 2024, propelled by the growing reliance on virtual consultations, remote diagnostics, and telemedicine platforms. The COVID-19 pandemic accelerated the adoption of these technologies, highlighting the necessity of accessible and scalable healthcare solutions. As a result, healthcare providers globally continue to integrate telehealth services to expand their reach and enhance care accessibility, ensuring patients receive timely and cost-effective medical attention.

The U.S. digital health market generated USD 123.6 billion in 2024, with a projected CAGR of 20.7% between 2025 and 2034. The country remains a global leader in digital healthcare adoption, backed by strong regulatory frameworks, high investment levels, and an advanced digital infrastructure. The widespread implementation of AI-powered diagnostic tools, remote patient monitoring solutions, and data-driven healthcare models has cemented the U.S. market's dominance. With the increasing integration of next-gen technologies and a robust push toward value-based care, the digital health sector in the U.S. is set to experience sustained growth, reinforcing its position as a driving force in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for remote patient monitoring services

- 3.2.1.2 Increasing smartphone penetration and internet connectivity

- 3.2.1.3 Favorable government initiatives and fundings in digital health

- 3.2.1.4 Growing venture capital investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security concerns

- 3.2.2.2 High implementation cost

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Market entry landscape

- 3.5 Regulatory landscape

- 3.5.1 U.S.

- 3.5.2 Europe

- 3.6 Investment analysis, by region

- 3.6.1 U.S.

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.7 Merger and acquisition landscape

- 3.8 Reimbursement scenario

- 3.9 Digital health project/initiatives

- 3.10 Technology landscape

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.3.1 Cloud-based

- 5.3.2 On-premises

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Telehealthcare

- 6.2.1 Telecare

- 6.2.1.1 Activity monitoring

- 6.2.1.2 Remote medication management

- 6.2.2 Telehealth

- 6.2.2.1 LTC monitoring

- 6.2.2.2 Video consultation

- 6.2.1 Telecare

- 6.3 mHealth

- 6.3.1 Wearables and connected medical devices

- 6.3.1.1 Blood pressure monitors

- 6.3.1.2 Heart rate monitors

- 6.3.1.3 Blood glucose monitor

- 6.3.1.4 Pulse oximeters

- 6.3.1.5 Sleep trackers

- 6.3.1.6 Neurological monitors

- 6.3.1.7 Other wearables and connected medical devices

- 6.3.2 mHealth apps

- 6.3.2.1 Medical apps

- 6.3.2.1.1 Womens health apps

- 6.3.2.1.2 Chronic disease management apps

- 6.3.2.1.3 Personal health record apps

- 6.3.2.1.4 Medication management apps

- 6.3.2.1.5 Remote monitoring apps

- 6.3.2.1.6 Other medical apps

- 6.3.2.2 Fitness apps

- 6.3.2.1 Medical apps

- 6.3.1 Wearables and connected medical devices

- 6.4 Health analytics

- 6.4.1 Predictive analytics

- 6.4.2 Prescriptive analytics

- 6.4.3 Descriptive analytics

- 6.5 Digital health systems

- 6.5.1 Electronic health records (EHRs)

- 6.5.2 e-prescribing systems

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Healthcare providers

- 7.3 Patients

- 7.4 Payers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accenture

- 9.2 AMD Global Telemedicine

- 9.3 American Well (Amwell)

- 9.4 Athenahealth

- 9.5 Capsa Healthcare

- 9.6 Eagle Telemedicine

- 9.7 Firstbeat Technologies

- 9.8 GE Healthcare

- 9.9 Health Catalyst

- 9.10 Honeywell International

- 9.11 IBM

- 9.12 iHealth Lab

- 9.13 Koninklijke Philips N.V.

- 9.14 McKesson Corporation

- 9.15 Oracle (Cerner Corporation)

- 9.16 Qualcomm Technologies

- 9.17 Teladoc Health

- 9.18 Veradigm LLC (Allscripts Healthcare Solutions)