|

시장보고서

상품코드

1699427

부동산용 디젤 발전기 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Diesel Powered Real Estate Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

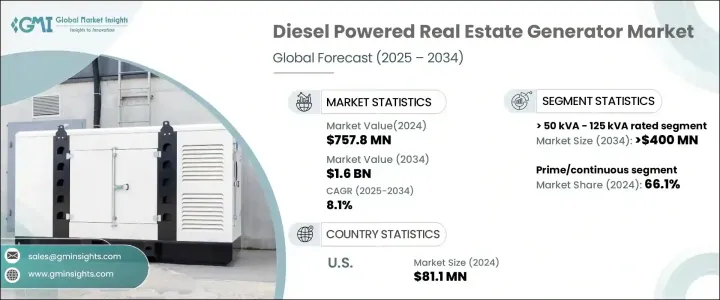

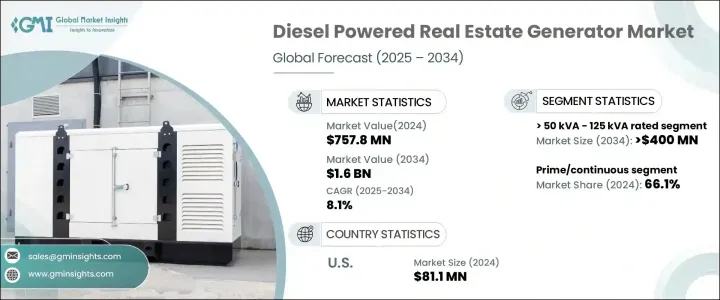

부동산용 디젤 발전기 세계 시장은 2024년에 7억 5,780만 달러에 달했으며, 2025-2034년 8.1%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다.

세계적으로 도시화가 가속화되고 안정적이고 신뢰할 수 있는 전력 솔루션에 대한 수요가 증가함에 따라 시장은 큰 모멘텀을 보이고 있습니다. 특히 신흥 경제 국가들의 급속한 인프라 개발로 인해 백업 전원 및 지속적인 전원 공급에 대한 필요성이 증가하고 있습니다. 주거 및 상업용 부동산 프로젝트가 확대됨에 따라 개발업체들은 중단 없는 전력 공급을 보장하기 위해 효율적이고 비용 효율적인 디젤 발전기에 투자하고 있습니다. 이상기후로 인한 정전 빈도 증가, 노후화된 전력망, 에너지 소비 증가는 시장 확대를 더욱 촉진할 것입니다.

기술 발전은 시장 성장을 가속하는 데 중요한 역할을 계속하고 있습니다. 자동 부하 관리 시스템, 전자식 연료 분사, 터보 과급기와 같은 기술 혁신은 연비를 개선하고 배기가스 배출을 감소시키고 있습니다. 탄소 발자국을 최소화하려는 규제 압력은 제조업체들이 더 깨끗하고 조용하며 에너지 효율적인 디젤 발전기를 개발하도록 유도하고 있습니다. 정부 및 민간 이해관계자들은 전력망 고장에 따른 리스크를 줄이고 부동산 부문 전반의 비즈니스 연속성을 보장하기 위해 백업 전원 솔루션에 많은 투자를 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 5,780만 달러 |

| 예상 금액 | 16억 달러 |

| CAGR | 8.1% |

50kVA 미만의 디젤 발전기 시장 규모는 2024년 1억 2,000만 달러에 달할 것으로 예상됩니다. 이러한 소형 발전기에 대한 수요 증가는 정전이 발생하기 쉬운 지역이나 신뢰할 수 있는 전력망 인프라가 없는 지역에서 안정적인 전력을 공급할 수 있는 능력에 기인합니다. 연료 효율과 소음 감소의 발전으로 인해 이 발전기는 안정적인 에너지 솔루션을 원하는 주택 소유자 및 기업에게 선호되는 선택이 되고 있습니다. 컴팩트하고 고성능인 이 발전기는 임시 또는 보조 전력이 필수적인 도시 및 반도시 지역 개발에서 인기를 끌고 있습니다.

시장은 대기 발전과 원동기/연속 발전의 두 가지 주요 응용 분야로 나뉘며, 2024년에는 원동기/연속 발전이 전체 시장 점유율의 66.1%를 차지할 것으로 예상되며, 이는 운전 효율 향상과 연료 절약 능력 강화가 그 원동력이 될 것입니다. 첨단 분사 기술과 지능형 전력 관리 시스템을 특징으로 하는 차세대 디젤 엔진에 대한 공공 및 민간 투자가 채택률을 높이고 있습니다. 산업계와 부동산 개발업체들이 지속 가능하고 강력한 에너지 솔루션을 우선시하는 가운데, 기술적으로 우수한 디젤 발전기에 대한 수요는 계속 증가하고 있습니다.

미국의 부동산용 디젤 발전기 시장은 2024년 8,110만 달러로 평가되었습니다. 이상기후로 인한 전력 장애 증가, 노후화된 전력망, 전력 수요의 급증으로 인해 신뢰할 수 있는 백업 전원 솔루션에 대한 필요성이 증가하고 있습니다. 부동산 개발자, 상업시설 소유주, 인프라 계획자들은 중단 없는 운영을 유지하고 정전에 따른 위험을 줄이기 위해 디젤 발전기에 주목하고 있습니다. 미국 시장은 발전기의 효율성 향상, 배출량 감소, 독립형 전원 솔루션 확대에 대한 투자로 에너지 공급업체들이 집중하고 있는 시장입니다. 전력 신뢰성에 대한 우려가 커지면서 부동산 분야에서 디젤 발전기의 역할이 그 어느 때보다 중요해지고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 전략적 전망

- 혁신과 지속가능성 전망

제5장 시장 규모와 예측 : 정격 출력별

- 주요 동향

- 50kVA 이하

- 50kVA-125kVA

- 125kVA-200kVA

- 200kVA-350kVA

- 350kVA-500kVA

- 500kVA 이상

제6장 시장 규모와 예측 : 용도별

- 주요 동향

- Standby

- Prime/continuous

제7장 시장 규모와 예측 : 지역별

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 러시아

- 영국

- 독일

- 프랑스

- 스페인

- 오스트리아

- 이탈리아

- 아시아태평양

- 중국

- 호주

- 인도

- 일본

- 한국

- 인도네시아

- 말레이시아

- 태국

- 베트남

- 필리핀

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 튀르키예

- 이란

- 오만

- 아프리카

- 이집트

- 나이지리아

- 알제리

- 남아프리카공화국

- 앙골라

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 칠레

제8장 기업 개요

- Aggreko

- Atlas Copco

- Caterpillar

- Cooper

- Cummins

- DEUTZ Power Center

- Generac Power Systems

- Greaves Cotton

- HIMOINSA

- J C Bamford Excavators

- Kirloskar

- Mahindra Powerol

- Rehlko

- Rolls-Royce

- YANMAR HOLDINGS

The Global Diesel Powered Real Estate Generator Market reached USD 757.8 million in 2024 and is projected to grow at a CAGR of 8.1% between 2025 and 2034. The market is witnessing significant momentum as urbanization accelerates worldwide, increasing the demand for reliable and stable power solutions. Rapid infrastructure development, especially in emerging economies, is amplifying the need for backup and continuous power sources. With real estate projects expanding in both residential and commercial sectors, developers are investing in efficient and cost-effective diesel generators to ensure uninterrupted power supply. The increasing frequency of power outages due to extreme weather conditions, aging grid networks, and growing energy consumption further fuels market expansion.

Technological advancements continue to play a critical role in driving market growth. Innovations such as automatic load management systems, electronic fuel injection, and turbocharging mechanisms are improving fuel efficiency and reducing emissions. Regulatory pressures aimed at minimizing carbon footprints have pushed manufacturers to develop cleaner, quieter, and more energy-efficient diesel generators. Governments and private stakeholders are heavily investing in backup power solutions to mitigate risks associated with grid failures, ensuring business continuity across real estate sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $757.8 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 8.1% |

Diesel-powered real estate generators with a rating of <= 50 kVA were valued at USD 120 million in 2024. The rising demand for these smaller generators stems from their ability to deliver consistent power in regions prone to outages or lacking reliable grid infrastructure. Advancements in fuel efficiency and noise reduction have made these generators a preferred choice for homeowners and businesses seeking stable energy solutions. Compact and high-performing, these units are gaining traction in urban and semi-urban developments where temporary or supplemental power is essential.

The market is divided into two primary application segments: standby and prime/continuous power generation. In 2024, prime/continuous generators accounted for 66.1% of the total market share, driven by improvements in operational efficiency and enhanced fuel-saving capabilities. Public and private investments in next-generation diesel engines featuring advanced injection technologies and intelligent power management systems are bolstering adoption rates. As industries and real estate developers prioritize sustainable yet powerful energy solutions, the demand for technologically superior diesel generators continues to rise.

The U.S. diesel-powered real estate generator market was valued at USD 81.1 million in 2024. Increasing power disruptions caused by extreme weather conditions, an aging power grid, and surging electricity demand have intensified the need for reliable backup power solutions. Real estate developers, commercial property owners, and infrastructure planners are turning to diesel generators to maintain uninterrupted operations and mitigate risks associated with power failures. The U.S. market remains a focal point for energy providers, with investments directed toward upgrading generator efficiency, lowering emissions, and expanding grid-independent power solutions. As electricity reliability concerns grow, the role of diesel-powered generators in real estate applications is becoming more critical than ever.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 350 kVA

- 5.6 > 350 kVA - 500 kVA

- 5.7 > 500 kVA

Chapter 6 Market Size and Forecast, By Application (USD Million & Units)

- 6.1 Key trends

- 6.2 Standby

- 6.3 Prime/continuous

Chapter 7 Market Size and Forecast, By Region (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 Aggreko

- 8.2 Atlas Copco

- 8.3 Caterpillar

- 8.4 Cooper

- 8.5 Cummins

- 8.6 DEUTZ Power Center

- 8.7 Generac Power Systems

- 8.8 Greaves Cotton

- 8.9 HIMOINSA

- 8.10 J C Bamford Excavators

- 8.11 Kirloskar

- 8.12 Mahindra Powerol

- 8.13 Rehlko

- 8.14 Rolls-Royce

- 8.15 YANMAR HOLDINGS