|

시장보고서

상품코드

1708167

데이터센터 화재 감지 및 진압 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Data Center Fire Detection and Suppression Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

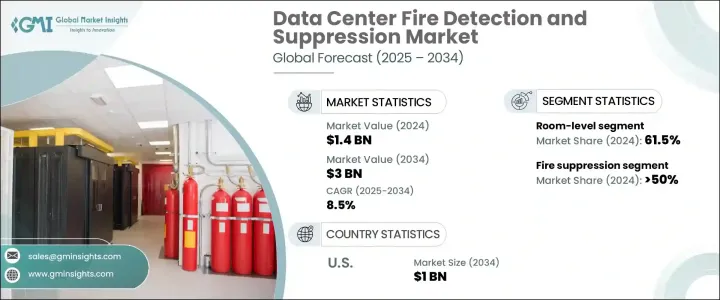

세계 데이터센터 화재 감지 및 진압 시장은 2024년 14억 달러 규모에 달했으며, 2025년부터 2034년까지 8.5%의 견고한 CAGR을 기록할 것으로 예측됩니다. 고급 화재 안전 솔루션에 대한 수요 증가는 클라우드 컴퓨팅, 엣지 컴퓨팅, AI 기반 기술, 고성능 컴퓨팅(HPC)의 채택 증가로 인한 세계 데이터센터의 급격한 성장에 힘입은 바 큽니다. 기업들은 방대한 데이터 흐름과 저지연 서비스를 지원하기 위해 데이터 인프라를 지속적으로 확장하고 있으며, 종합적인 화재 안전 확보가 최우선 과제로 떠오르고 있습니다.

최신 데이터센터, 특히 하이퍼스케일 및 코로케이션 시설은 수백만 달러 상당의 미션 크리티컬한 IT 자산을 보유하고 있기 때문에 전기적 장애, 과열, 장비 고장으로 인한 화재의 위험에 노출되기 쉽습니다. 다운타임의 비용은 분당 수십만 달러에 달하기 때문에 신뢰할 수 있고 지능적인 화재 감지 및 소화 시스템의 필요성이 그 어느 때보다 높아졌습니다. 또한, 엄격한 화재 안전 규정과 기밀 데이터 및 장비 보호에 대한 인식이 높아짐에 따라 사업자들은 실시간 모니터링과 빠른 응답 시간을 제공하는 AI 기반 및 IoT 지원 화재 방지 솔루션의 통합을 추진하고 있습니다. 비즈니스 연속성, 운영 탄력성, 증가하는 사이버 물리적 위험으로부터의 보호에 대한 중요성이 강조되면서 시장은 더욱 발전하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 14억 달러 |

| 예상 금액 | 30억 달러 |

| CAGR | 8.5% |

시장은 화재 감지 시스템과 진압 시스템으로 분류되며, 2024년에는 소화 시스템이 50%의 시장 점유율을 차지하여 화재로 인한 피해로부터 고가의 자산을 보호하는 데 중요한 역할을 한 것으로 나타났습니다. 화재 감지 시스템은 화재 위험을 조기에 식별하고 효율적인 사고 대응에 필수적입니다. 이러한 시스템은 AI 기반 연기 감지기, 다중 센서 감지 장치, 흡입식 연기 감지(ASD) 시스템 등으로 구성되어 있으며, ASD+와 같은 최첨단 기술은 이중 파장 신호 처리를 활용하여 연기와 먼지를 구분하는 능력을 강화하여 오경보를 방지하고, 화재 위험을 조기에 식별하여 효율적인 사고 대응을 가능하게 합니다. 오경보를 줄이고 실제 위협에 대해 적시에 경보를 발령할 수 있습니다.

도입 현황에 따라 시장은 룸 레벨 솔루션과 빌딩 레벨 솔루션으로 나뉘며, 2024년에는 룸 레벨 시스템이 61.5%의 점유율을 차지했습니다. 데이터센터 사업자들은 전체 시설을 위험에 빠뜨리지 않고 개별 데이터 홀, 서버실, 고밀도 랙 공간을 보호하기 위해 국소적이고 표적화된 억제력을 제공하기 때문에 룸 레벨의 화재 예방 조치를 선호하고 있습니다. 이 접근 방식은 사전 조치 스프링클러, 고급 가스 기반 소화 시스템, 제한된 구역 내에서 신속하게 반응하도록 설계된 AI 통합 감지 장치 등을 사용합니다. 하이퍼스케일, 코로케이션, 엔터프라이즈 데이터센터의 급속한 증가를 고려할 때, 화재 발생 시 광범위한 정전 및 장비 손실을 방지하기 위해 룸 레벨의 화재 예방 조치가 필수적이라고 여겨집니다.

북미 데이터센터 화재 감지 및 소화 시장은 2034년까지 10억 달러 규모의 시장을 형성하며 전 세계적으로 지배적인 위치를 차지할 것으로 예측됩니다. 이 지역의 시장 강세는 복잡한 데이터센터 인프라의 설치 면적이 확대되고 있으며, 첨단 화재 안전 기술 도입에 대한 중요성이 높아지고 있기 때문입니다. 미국에서는 클라우드 서비스, AI 워크로드, 데이터 트래픽의 지속적인 증가로 인해, 탁월한 신뢰성과 엄격한 안전 표준을 준수하는 차세대 화재 감지 및 소화 시스템에 대한 수요가 증가하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 산업 생태계 분석

- 원재료 공급업체

- 제조업체

- 시스템 통합사업자

- 설치·보수 프로바이더

- 최종 용도

- 공급업체 상황

- 이익률 분석

- 기술 혁신 상황

- 특허 분석

- 주요 뉴스와 대처

- 사례 연구

- 규제 상황

- 영향요인

- 성장 촉진요인

- 데이터센터 확장 증가

- 화재 안전 규제 엄격화

- AI와 스마트 감지 채용 확대

- 지속가능한 화재 억제로의 이동 증가

- 업계의 잠재적 리스크·과제

- 높은 도입 비용

- 기존 인프라와의 통합

- 성장 촉진요인

- 성장 가능성 분석

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정과 예측 : 시스템별, 2021-2034년

- 주요 동향

- 화재 감지

- 연기

- 열

- 불꽃

- 가스

- 화재 진압

- 클린제

- 수성

- 가스 기반

- 폼 기반

제6장 시장 추정과 예측 : 전개별, 2021-2034년

- 주요 동향

- 방 레벨

- 건물 레벨

제7장 시장 추정과 예측 : 데이터센터별, 2021-2034년

- 주요 동향

- 하이퍼스케일

- 코로케이션

- 기업

- 엣지

- 정부·군수

제8장 시장 추정과 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카공화국

- 사우디아라비아

제9장 기업 개요

- 3S

- Ambetronics Engineers

- Cannon Fire Protection

- Chemours

- Control Fire Systems

- Eaton

- Fike

- FireFlex Systems

- Hiller Companies

- Honeywell

- Impact Fire Services

- Johnson Controls

- Minimax

- ORR Protection

- Robert Bosch

- SEM-SAFE

- SEVO Systems

- Siemens

- Victaulic

- WAGNER Group

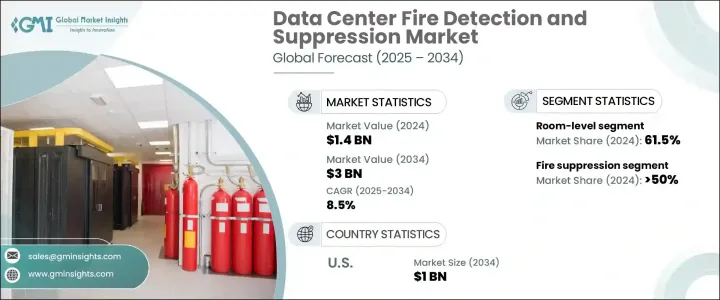

The Global Data Center Fire Detection and Suppression Market reached USD 1.4 billion in 2024 and is expected to witness a robust CAGR of 8.5% from 2025 to 2034. The rising demand for advanced fire safety solutions is largely fueled by the exponential growth of data centers worldwide, driven by the increasing adoption of cloud computing, edge computing, AI-powered technologies, and high-performance computing (HPC). As companies continue to scale up their data infrastructure to support massive data flows and low-latency services, ensuring comprehensive fire safety has become a top priority.

Modern data centers, especially hyperscale and colocation facilities, house mission-critical IT assets worth millions of dollars, making them vulnerable to fire hazards caused by electrical faults, overheating, or equipment failures. With downtime costs running into hundreds of thousands of dollars per minute, the need for reliable and intelligent fire detection and suppression systems has never been greater. Additionally, stringent fire safety regulations and rising awareness about safeguarding sensitive data and equipment are pushing operators to integrate AI-based and IoT-enabled fire protection solutions, which offer real-time monitoring and faster response times. Increasing emphasis on business continuity, operational resilience, and protection against growing cyber-physical risks is further propelling the market forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $3 Billion |

| CAGR | 8.5% |

The market is categorized into fire detection and fire suppression systems, where in 2024, the fire suppression segment captured a 50% market share, highlighting its critical role in safeguarding high-value assets from fire-related damages. Fire detection systems are indispensable for early-stage fire risk identification and efficient incident response. These systems comprise AI-powered smoke detectors, multi-sensor detection units, and aspirating smoke detection (ASD) systems, all designed to offer faster and more accurate detection capabilities. Cutting-edge technologies like ASD+ leverage dual-wavelength signal processing, enhancing their ability to differentiate between smoke and dust, thereby reducing false alarms and ensuring timely alerts for genuine threats.

Based on deployment, the market is split between room-level and building-level solutions, with room-level systems commanding a 61.5% share in 2024. Data center operators increasingly prefer room-level fire protection because it provides localized and targeted suppression, protecting individual data halls, server rooms, and high-density rack spaces without compromising entire facilities. This approach involves the use of pre-action sprinklers, advanced gas-based suppression systems, and AI-integrated detection devices designed to respond swiftly within confined zones. Given the rapid rise of hyperscale, colocation, and enterprise data centers, room-level fire protection is seen as essential to prevent widespread outages and equipment loss in the event of a fire.

North America Data Center Fire Detection and Suppression Market is projected to generate USD 1 billion by 2034, retaining its dominant position globally. The region's market strength stems from the expanding footprint of complex data center infrastructure and a growing emphasis on implementing state-of-the-art fire safety technologies. In the U.S., continuous growth in cloud services, AI workloads, and data traffic is escalating the demand for next-gen fire detection and suppression systems that offer unmatched reliability and compliance with stringent safety standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 System integrators

- 3.1.4 Installation and maintenance providers

- 3.1.5 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Case studies

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising data center expansion

- 3.9.1.2 Increasing stringency of fire safety regulations

- 3.9.1.3 Growing adoption of AI & smart detection

- 3.9.1.4 Increasing shift to sustainable fire suppression

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High implementation cost

- 3.9.2.2 Integration with existing infrastructure

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By System, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Fire detection

- 5.2.1 Smoke

- 5.2.2 Heat

- 5.2.3 Flame

- 5.2.4 Gas

- 5.3 Fire suppression

- 5.3.1 Clean agent

- 5.3.2 Water-based

- 5.3.3 Gas- based

- 5.3.4 Foam- based

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Room level

- 6.3 Building level

Chapter 7 Market Estimates & Forecast, By Data Center, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Hyperscale

- 7.3 Colocation

- 7.4 Enterprise

- 7.5 Edge

- 7.6 Government & military

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 3S

- 9.2 Ambetronics Engineers

- 9.3 Cannon Fire Protection

- 9.4 Chemours

- 9.5 Control Fire Systems

- 9.6 Eaton

- 9.7 Fike

- 9.8 FireFlex Systems

- 9.9 Hiller Companies

- 9.10 Honeywell

- 9.11 Impact Fire Services

- 9.12 Johnson Controls

- 9.13 Minimax

- 9.14 ORR Protection

- 9.15 Robert Bosch

- 9.16 SEM-SAFE

- 9.17 SEVO Systems

- 9.18 Siemens

- 9.19 Victaulic

- 9.20 WAGNER Group