|

시장보고서

상품코드

1708203

바이오마커 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Biomarkers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

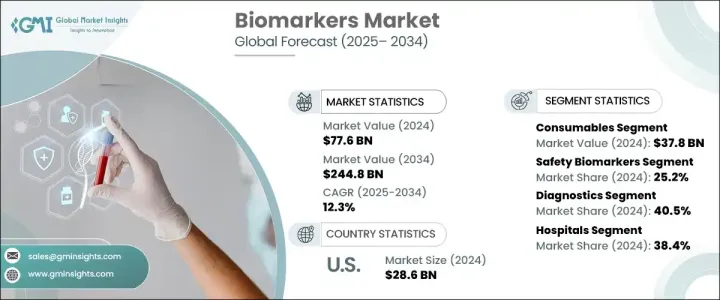

세계 바이오마커 시장은 2024년 776억 달러로 평가되었고, 2025년 859억 달러에서 2034년 2,448억 달러에 이르며 연평균 12.3% 성장할 것으로 예측됩니다.

혈액, 조직, 체액에 포함된 단백질, 유전자, 기타 분자를 포함한 바이오마커는 생물학적 과정과 병태생리를 파악하는 데 중요한 역할을 합니다. 질병의 조기 발견, 치료 반응 모니터링, 맞춤 치료 개발 등에 활용되어 시장 개척의 원동력이 되고 있습니다. 비침습적 식별과 치료 반응의 실시간 모니터링을 가능하게 하는 액체 생검과 같은 기술 혁신을 통해 개인 맞춤형 의료의 발전은 바이오마커 검출과 치료 접근법을 변화시키고 있습니다. 이러한 발전으로 바이오마커의 임상 적용이 확대되고 있으며, 환자 예후를 개선하고 신약 개발을 가속화하는 데 필수적인 도구가 되고 있습니다.

시약, 분석 키트, 마이크로플레이트 등 소모품 부문은 2024년 378억 달러 규모에 달했으며, 예측 기간 동안 12.1%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 엄격한 품질 관리 기준에 따라 제조된 소모품은 특히 임상 진단 및 신약 개발의 바이오마커 연구에서 일관되고 재현성 있는 결과를 보장합니다. 질량 분석, 차세대 염기서열 분석(NGS), 액체 크로마토그래피와 같은 첨단 플랫폼과의 호환성은 바이오마커 탐색 및 분석의 정확성과 효율성을 향상시켜 이 분야 수요를 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 776억 달러 |

| 예상 금액 | 2,448억 달러 |

| CAGR | 12.3% |

안전성 바이오마커 분야는 2024년 25.2% 시장 점유율을 차지했고, 2034년에는 632억 달러에 달할 것으로 예측됩니다. 안전성 바이오마커는 의약품 및 치료제의 잠재적 부작용을 조기에 발견하고, 심각한 합병증을 예방하며, 후기 임상시험 실패에 따른 비용을 최소화하는 데 중요한 역할을 합니다. 이러한 바이오마커는 여러 장기 시스템에 걸친 독성 식별을 용이하게 하고, 장기 기능의 지속적인 모니터링을 가능하게 하며, 의약품 개발의 전반적인 안전성을 향상시킬 수 있습니다.

진단 부문의 2024년 시장 점유율은 40.5%였습니다. 이는 바이오마커가 질병을 조기에 발견하고 적시에 개입하여 예후를 개선할 수 있는 능력에 기인합니다. 혈액검사, 소변검사, 타액검사 등 비침습적, 저침습적 바이오마커 검출 방법은 기존 진단방법의 불편함을 줄이고 환자의 순응도를 향상시키며, NGS, 질량분석 등 진단기술의 혁신은 바이오마커 검출의 민감도와 정확도를 더욱 향상시켜 임상적 유용성을 임상적 유용성을 확대하며 시장 성장을 견인하고 있습니다.

2024년 시장 점유율 38.5%를 차지한 암 분야는 여전히 바이오마커의 주요 용도입니다. 바이오마커는 다양한 암을 조기에 발견하고, 치료 성공 가능성을 높이고, 양성과 악성을 구분할 수 있습니다. 또한, 치료 후 감시를 통해 암의 재발 가능성을 파악하여 적시에 개입할 수 있도록 하여 환자의 예후를 개선하는 데 기여합니다.

2024년 시장 점유율 38.4%를 차지한 병원은 대량의 만성질환 환자를 관리하고 고급 진단을 위한 숙련된 인력을 제공할 수 있다는 점에서 바이오마커 시장을 주도하고 있습니다. 액체생검, 동반진단 등 비침습적 바이오마커 검사에 대한 수요가 증가하면서 바이오마커 시장에서 병원의 역할이 더욱 강화되고 있습니다.

북미는 2024년 314억 달러, 2034년에는 975억 달러에 달할 것으로 예상되며, 미국은 2024년 286억 달러로 이 지역을 지배했습니다. 심혈관질환, 신경질환, 암과 같은 만성질환의 유병률 증가가 미국 시장 성장의 원동력이 되고 있습니다. 이러한 질병의 부담이 증가함에 따라 제약회사, 병원 및 연구기관은 첨단 진단 솔루션과 혁신적인 치료법 개발에 투자하고 있으며, 이는 바이오마커 시장의 지속적인 성장을 보장하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- 규제 상황

- 기술적 전망

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업 - 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산 및 예측 : 제품 및 서비스별, 2021년-2034년

- 주요 동향

- 소모품

- 소프트웨어

- 서비스

제6장 시장 추산 및 예측 : 바이오마커 유형별, 2021년-2034년

- 주요 동향

- 안전성 바이오마커

- 유효성 바이오마커

- 예측 바이오마커

- 대체 바이오마커

- 약역학적 바이오마커

- 예후 예측 바이오마커

- 밸리데이션 바이오마커

제7장 시장 추산 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 진단

- Drug Discovery & Development

- 맞춤형 의료

- 질병 리스크 평가

- 기타 용도

제8장 시장 추산 및 예측 : 질환 유형별, 2021년-2034년

- 주요 동향

- 암

- 심혈관 질환

- 신경 질환

- 면역 질환

- 기타 질환 유형

제9장 시장 추산 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원

- 진단 실험실

- 학술기관 및 연구기관

- 기타 최종 사용

제10장 시장 추산 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 개요

- Abbott Laboratories

- Agilent Technologies

- Bio-Rad Laboratories

- Becton, Dickinson and Company

- Eurofins Scientific

- Epigenomics

- F. Hoffmann-La Roche

- GE Healthcare

- Illumina

- Johnson &Johnson

- Merck KGaA

- PerkinElmer

- QIAGEN

- Siemens Healthineers

- Thermo Fisher Scientific

The Global Biomarkers Market was valued at USD 77.6 billion in 2024 and is projected to grow from USD 85.9 billion in 2025 to USD 244.8 billion by 2034 at a CAGR of 12.3%. Biomarkers, which include proteins, genes, and other molecules found in blood, tissues, and body fluids, play a crucial role in identifying biological processes and disease conditions. Their use in early disease detection, monitoring treatment response, and developing personalized therapies continues to drive market growth. Advances in personalized medicine are transforming biomarker detection and treatment approaches, with innovations such as liquid biopsies enabling non-invasive identification and real-time monitoring of treatment responses. These advancements have expanded the clinical applications of biomarkers, making them indispensable tools in improving patient outcomes and accelerating drug discovery.

The consumables segment, which includes reagents, assay kits, and microplates, generated USD 37.8 billion in 2024 and is projected to grow at a CAGR of 12.1% during the forecast period. Consumables manufactured under stringent quality control standards ensure consistent and reproducible results across biomarker studies, particularly in clinical diagnostics and drug discovery. Their compatibility with advanced platforms such as mass spectrometry, next-generation sequencing (NGS), and liquid chromatography enhances the accuracy and efficiency of biomarker discovery and analysis, driving demand in this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $77.6 Billion |

| Forecast Value | $244.8 Billion |

| CAGR | 12.3% |

The safety biomarkers segment captured a 25.2% market share in 2024 and is expected to reach USD 63.2 billion by 2034. Safety biomarkers play a critical role in detecting potential adverse effects of drugs or treatments at an early stage, preventing severe complications, and minimizing costs associated with late-stage clinical trial failures. These biomarkers facilitate the identification of toxicity across multiple organ systems, allowing continuous monitoring of organ function and improving overall safety in drug development.

The diagnostics segment held a 40.5% market share in 2024, driven by the ability of biomarkers to identify diseases at an early stage and improve prognosis through timely intervention. Non-invasive and minimally invasive biomarker detection methods, including blood, urine, and saliva tests, enhance patient compliance while reducing discomfort associated with traditional diagnostic methods. Innovations in diagnostic technologies, such as NGS and mass spectrometry, further improve the sensitivity and accuracy of biomarker detection, expanding their clinical utility and boosting market growth.

The cancer segment, with a 38.5% market share in 2024, remains a dominant application of biomarkers. Biomarkers enable the early detection of various cancers, improving the likelihood of successful treatment and distinguishing between benign and malignant tumors. They also facilitate post-treatment surveillance to identify potential cancer recurrence, ensuring timely intervention and contributing to better patient outcomes.

Hospitals, which accounted for a 38.4% market share in 2024, continue to lead the biomarkers market due to their ability to manage a large volume of chronic disease patients and provide highly skilled personnel for advanced diagnostic procedures. The growing demand for non-invasive biomarker tests, such as liquid biopsy and companion diagnostics, has further strengthened the role of hospitals in the biomarker landscape.

North America generated USD 31.4 billion in 2024 and is expected to reach USD 97.5 billion by 2034, with the U.S. dominating the region at USD 28.6 billion in 2024. The rising prevalence of chronic diseases, including cardiovascular diseases, neurological disorders, and cancer, drives market growth in the U.S. The increasing burden of these diseases has prompted pharmaceutical companies, hospitals, and research institutions to invest in the development of advanced diagnostic solutions and innovative therapies, ensuring the continued expansion of the biomarkers market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Advancements in genomic and proteomic technologies

- 3.2.1.3 Rising demand for personalized medicine

- 3.2.1.4 Increasing research and development activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of biomarker development and testing

- 3.2.2.2 Lack of standardization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product and Services, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Biomarker Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Safety biomarkers

- 6.3 Efficacy biomarkers

- 6.4 Predictive biomarkers

- 6.5 Surrogate biomarkers

- 6.6 Pharmacodynamic biomarkers

- 6.7 Prognostics biomarkers

- 6.8 Validation biomarkers

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Diagnostics

- 7.3 Drug discovery and development

- 7.4 Personalized medicine

- 7.5 Disease risk assessment

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Cancer

- 8.3 Cardiovascular diseases

- 8.4 Neurological diseases

- 8.5 Immunological diseases

- 8.6 Other diseases types

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic laboratories

- 9.4 Academic and research institutions

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Abbott Laboratories

- 11.2 Agilent Technologies

- 11.3 Bio-Rad Laboratories

- 11.4 Becton, Dickinson and Company

- 11.5 Eurofins Scientific

- 11.6 Epigenomics

- 11.7 F. Hoffmann-La Roche

- 11.8 GE Healthcare

- 11.9 Illumina

- 11.10 Johnson & Johnson

- 11.11 Merck KGaA

- 11.12 PerkinElmer

- 11.13 QIAGEN

- 11.14 Siemens Healthineers

- 11.15 Thermo Fisher Scientific