|

시장보고서

상품코드

1716449

반려동물용 의약품 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Companion Animal Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

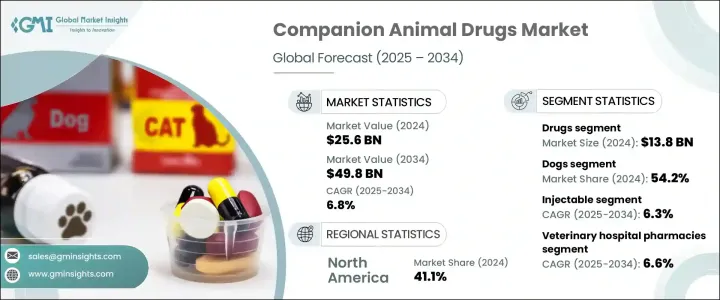

반려동물용 의약품 세계 시장은 2024년에 256억 달러로 평가되었으며, 2025년부터 2034년에 걸쳐 CAGR은 6.8%를 보일 것으로 예측됩니다.

반려동물의 입양이 증가하고 있는 것, 반려동물의 만성 질환의 유병률이 상승하고 있는 것, 고도의 치료나 수의학적 케어에 투자하는 반려동물 소유자의 의욕 증가가 이 성장을 뒷받침하고 있습니다. 반려동물 주인들은 점점 더 반려동물의 건강을 위해 예방의료, 예방접종, 투약에 지출하게 되었습니다. 이러한 의식의 변화가 시장의 확대에 크게 기여하고 있습니다.

2024년에 138억 달러로 가장 높은 시장 점유율을 차지한 의약품 분야는 반려동물의 만성질환과 감염증의 이환율의 상승으로 계속 시장을 독점하고 있습니다. 제약 회사는 연구개발에 적극적으로 투자하고, 씹을 수 있는 정제나 맛을 낸 약 등, 새로운 제제를 도입하는 것으로, 투여를 용이하게 해, 컴플라이언스를 향상시키고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 256억 달러 |

| 예측 금액 | 498억 달러 |

| CAGR | 6.8% |

동물 유형별로는 개 부문이 2024년에 54.2%의 최대 수익 점유율을 유지하여 높은 양자율과 개 케어에 대한 지출 증가가 견인하고 있습니다. 상승은 효과적인 치료법의 필요성을 돋보이게 하고, 제약회사가 개의 건강을 타겟으로 한 특수한 의약품을 개발하도록 촉구하고 있습니다. 종합적인 헬스케어 옵션이 이용 가능하고, 주인의 지출이 증가하고 있는 것이, 이 부문의 성장을 더욱 뒷받침하고 있습니다.

2024년 최대 시장 점유율을 차지한 주사제 투여 경로는 예측 기간 동안 CAGR 6.3% 로 큰 성장을 이룰 것으로 예측되고 있습니다. 배리 기술의 진보와 바늘이 없는 주사기의 도입으로 반려동물과 주인 모두에게 편의성이 향상되어 스트레스가 경감된 것이 이 루트에의 기호성의 향상에 기여하고 있습니다.

동물병원 약국은 2024년에 유통 채널의 대부분을 차지하고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR)은 6.6%를 보일 것으로 예측됩니다. 이 약국은 처방약, 백신 및 보충제를 포함한 광범위한 동물 건강 제품을 제공하며 반려동물 주인에게 신뢰할 수있는 출처가 되었습니다.

북미는 2024년에 41.1%의 최대 시장 점유율을 차지했으며, 미국은 91억 달러의 수익을 올렸습니다. 이 지역은 잘 발달된 수의학적 의료 시스템, 높은 반려동물 소유율, 반려동물 건강 관리에 대한 지출 증가의 혜택을 받아 반려동물 의약품 시장의 지속적인 성장을 지원하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 반려동물 보험 수요 급증

- 반려동물의 비만률 상승

- 세계 반려동물 관리에 대한 정부 지원 증가

- 온라인 동물 약국 수요 증가

- 업계의 잠재적 위험 및 과제

- 반려동물용 의약품과 관련된 높은 비용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- GAP 분석

- 소비자 행동 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- 의약품

- 항기생충약

- 항염증제

- 항감염증약

- 부신피질 스테로이드

- 정신안정제

- 심장혈관약

- 위장약

- 백신

- 개량형 생백신(MLV)

- 킬드 불활화 백신

- 재조합 백신

- 약용 사료 첨가물

- 항생제

- 비타민

- 아미노산

- 효소

- 산화 방지제

- 프리바이오틱스와 프로바이오틱스

- 미네랄

- 탄수화물

- 프로판디올

제6장 시장 추정 및 예측 : 동물 유형별, 2021년-2034년

- 주요 동향

- 개

- 고양이

- 말

- 기타 동물 유형

제7장 시장 추정 및 예측 : 투여 경로별, 2021-2034년

- 주요 동향

- 경구제

- 주사제

- 국소

- 기타 투여 경로

제8장 시장 추정 및 예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 동물병원 약국

- 전자상거래

- 소매 약국

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 폴란드

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 대만

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- GCC 국가

- 이스라엘

제10장 기업 프로파일

- Agrolabo

- Boehringer Ingelheim International

- Ceva Sante Animale

- Chanelle Pharma

- Dechra Pharmaceuticals

- Elanco Animal Health Incorporated

- Endovac Animal Health

- HIPRA

- Indian Immunologicals

- Merck.

- Norbrook

- Symrise

- Vetoquinol

- Virbac

- Zoetis

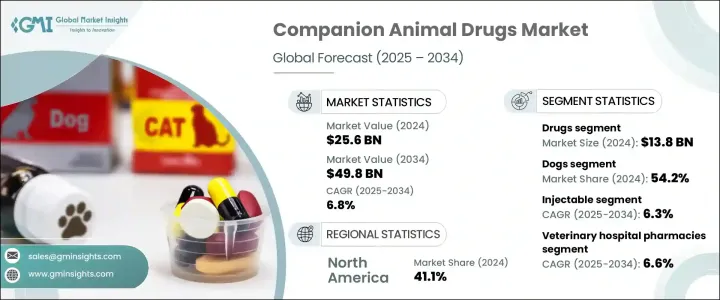

The Global Companion Animal Drugs Market was valued at USD 25.6 billion in 2024 and is expected to grow at a CAGR of 6.8% from 2025 to 2034. The increasing adoption of companion animals, the rising prevalence of chronic diseases in pets, and the growing willingness of pet owners to invest in advanced treatments and veterinary care are fueling this growth. Pet owners increasingly perceive their animals as family members, prompting them to spend on preventive care, vaccinations, and medications to ensure their well-being. This shift in attitude has contributed significantly to the expansion of the market. As veterinary science continues to advance, innovative formulations, targeted therapies, and improved drug delivery methods are enhancing treatment efficacy and compliance among pet owners, thereby accelerating market growth.

The drugs segment, which accounted for the highest market share of USD 13.8 billion in 2024, continues to dominate the market due to the rising incidence of chronic diseases and infections in pets. Increased pet ownership and the growing trend of pet humanization have boosted the demand for antibiotics, anti-inflammatory drugs, and parasiticides. Pharmaceutical companies are actively investing in research and development to introduce novel formulations such as chewable tablets and flavored medications, making administration easier and improving compliance. Regulatory approvals and innovations in veterinary medicine have also played a pivotal role in driving the sustained growth of this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.6 Billion |

| Forecast Value | $49.8 Billion |

| CAGR | 6.8% |

By animal type, the dogs segment maintained the largest revenue share of 54.2% in 2024, driven by high adoption rates and increased spending on dog care. Growing awareness of chronic diseases among dogs, such as cancer and diabetes, has led to a higher demand for advanced treatments and medications. The rising prevalence of these conditions highlights the need for effective therapies, encouraging pharmaceutical companies to develop specialized drugs targeting canine health. The availability of comprehensive healthcare options and increased expenditure by pet owners further bolster segment growth.

The injectable route of administration, which held the largest market share in 2024, is anticipated to witness significant growth at a CAGR of 6.3% during the forecast period. Injectable drugs, including vaccines, antibiotics, and analgesics, offer rapid onset of action and precise dosing, making them ideal for emergency treatments. Advancements in injectable drug delivery technologies and the introduction of needle-free injectors have enhanced convenience and reduced stress for both pets and their owners, contributing to the growing preference for this route.

Veterinary hospital pharmacies dominated the distribution channel in 2024 and are projected to grow at a CAGR of 6.6% from 2025 to 2034. These pharmacies offer a wide range of animal healthcare products, including prescription drugs, vaccines, and supplements, making them a reliable source for pet owners. Their established reputation, quality assurance, and expertise in dispensing medications drive their continued dominance in the market.

North America accounted for the largest market share of 41.1% in 2024, with the U.S. generating USD 9.1 billion in revenue. The region benefits from a well-developed veterinary healthcare system, high pet ownership rates, and increased spending on pet healthcare, supporting the continuous growth of the companion animal drugs market. The presence of leading pharmaceutical companies further ensures a steady supply of innovative and effective drugs, driving the expansion of the market in this region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging demand for pet insurance policies worldwide

- 3.2.1.2 Rising rate of obesity in companion animals

- 3.2.1.3 Increasing government support for pet care across the globe

- 3.2.1.4 Growing demand for online veterinary pharmacies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with companion animal drugs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 GAP analysis

- 3.6 Consumer behaviour trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Drugs

- 5.2.1 Antiparasitic

- 5.2.2 Anti-inflammatory

- 5.2.3 Anti-infectives

- 5.2.4 Corticosteroids

- 5.2.5 Tranquilizers

- 5.2.6 Cardiovascular drugs

- 5.2.7 Gastrointestinal drugs

- 5.3 Vaccines

- 5.3.1 Modified live vaccines (MLV)

- 5.3.2 Killed inactivated vaccines

- 5.3.3 Recombinant vaccines

- 5.4 Medicated feed additives

- 5.4.1 Antibiotics

- 5.4.2 Vitamins

- 5.4.3 Amino acids

- 5.4.4 Enzymes

- 5.4.5 Antioxidants

- 5.4.6 Prebiotics and probiotics

- 5.4.7 Minerals

- 5.4.8 Carbohydrates

- 5.4.9 Propandiol

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Horses

- 6.5 Other animal types

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

- 7.4 Topical

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospital pharmacies

- 8.3 E-commerce

- 8.4 Retail pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Taiwan

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 GCC Countries

- 9.6.3 Israel

Chapter 10 Company Profiles

- 10.1 Agrolabo

- 10.2 Boehringer Ingelheim International

- 10.3 Ceva Sante Animale

- 10.4 Chanelle Pharma

- 10.5 Dechra Pharmaceuticals

- 10.6 Elanco Animal Health Incorporated

- 10.7 Endovac Animal Health

- 10.8 HIPRA

- 10.9 Indian Immunologicals

- 10.10 Merck.

- 10.11 Norbrook

- 10.12 Symrise

- 10.13 Vetoquinol

- 10.14 Virbac

- 10.15 Zoetis