|

시장보고서

상품코드

1716573

자동차 분야 AI 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)AI in Automotive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

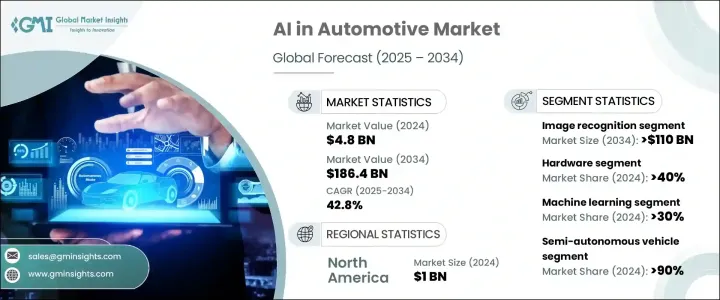

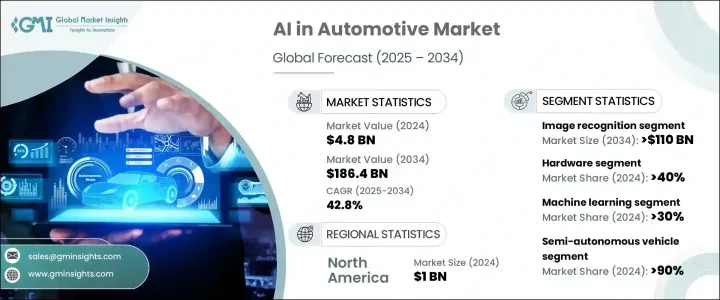

세계의 자동차 분야 AI 시장은 2024년에 48억 달러로 평가되었고, 2025년부터 2034년에 걸쳐 42.8%의 CAGR로 성장할 것으로 예측되고 있습니다.

이러한 급격한 성장은 AI 기술이 모빌리티의 미래를 계속 재정의함에 따라 지능형 자동차 솔루션에 대한 수요가 증가하고 있음을 반영합니다. 차량에 AI가 통합되면서 자동차 운행 방식이 변화하고 있으며, 탑승자의 안전과 운전 경험 모두 향상되고 있습니다. 선도적인 자동차 제조업체와 기술 기업들은 특히 자율 주행 차량과 차세대 첨단 운전자 지원 시스템(ADAS)을 위한 AI 기반 시스템에 막대한 투자를 하고 있습니다.

차량 인텔리전스, 상황 인식, 실시간 의사 결정을 향상시키는 AI의 역할은 자동차 산업을 더욱 안전하고, 더욱 연결되고, 더욱 자율적인 미래로 이끌고 있습니다. 교통 관리 및 충돌 방지부터 예측 유지보수 및 개인화된 차량 내 경험에 이르기까지, AI는 최신 차량 아키텍처의 핵심 요소로 자리 잡고 있습니다. 또한 자동차 제조업체들은 예측 내비게이션, 음성 인식, 행동 분석 기능을 제공하여 운전자와 탑승자의 편의성을 향상시키는 데 AI를 활용하고 있습니다. 보다 안전하고 스마트한 모빌리티 솔루션에 대한 소비자 수요가 증가함에 따라 AI는 자동차 업계에서 필수 불가결한 요소가 될 것이며, 향후 10년간 시장 성장을 더욱 가속화할 것입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 48억 달러 |

| 예측 금액 | 1,864억 달러 |

| CAGR | 42.8% |

AI 도입의 급증은 주로 ADAS 및 자율 주행 솔루션과 같은 기술 구현의 증가에 의해 주도되고 있습니다. AI는 첨단 센서, 고해상도 카메라, 레이더, LiDAR 시스템과의 원활한 통합을 통해 차량 안전과 전반적인 주행 경험을 크게 향상시킵니다. 차선 유지 보조, 어댑티브 크루즈 컨트롤, 자동 긴급 제동, 보행자 감지 등의 기능은 차량이 주변 환경을 분석하고 즉각적인 주행 결정을 내릴 수 있도록 하는 AI 알고리즘을 기반으로 하여 사고를 줄이고 도로 안전을 개선합니다.

이 시장은 주로 데이터 마이닝 및 이미지 인식과 같은 프로세스를 기반으로 세분화되며, 이미지 인식이 시장을 지배하고 있습니다. 이 부문은 자율 주행 차량과 ADAS 기능을 구현하는 데 중요한 역할을 함으로써 2034년까지 1,100억 달러 이상의 매출을 창출할 것으로 예상됩니다. 이미지 인식 기술을 통해 AI 시스템은 실시간 환경 데이터를 처리하고 해석하여 보행자, 교통 표지판, 차량, 차선 표시를 정확하게 식별할 수 있습니다. 동적인 도로 상황을 인식하고 이해하는 능력은 이미지 인식을 자율 주행 개발의 초석으로 만듭니다.

컴포넌트의 관점에서 자동차 시장의 AI는 하드웨어, 소프트웨어, 서비스로 나뉘며, 2024년에는 하드웨어가 40%의 상당한 점유율을 차지할 것으로 예상됩니다. 자동차 제조업체들은 AI 기반 차량의 연산 수요를 지원하기 위해 첨단 하드웨어에 막대한 투자를 하고 있습니다. 실시간 처리를 위한 방대한 데이터 스트림을 처리하고 자율 주행, 이미지 감지, 센서 융합, 딥러닝 기반 분석과 같은 원활한 AI 기능을 구현하려면 AI 칩, GPU, 센서, LiDAR 시스템과 같은 특수 부품이 필수적입니다.

미국 자동차 분야 AI 시장은 이 나라의 견고한 기술 인프라와 급속한 AI 도입으로 주목할만한 33%의 점유율을 차지했으며, 2024년에는 10억 달러를 창출했습니다. 주요 자동차 제조업체와 거대 기술 기업들이 AI 기반 자율주행 기술과 첨단 안전 시스템 개발을 주도하면서 미국은 글로벌 AI 기반 자동차 환경을 형성하는 핵심 업체로 확고히 자리매김하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 기술 공급자

- OEM 제조업체

- 유통업체

- 최종 용도

- 이익률 분석

- 공급자의 상황

- 기술과 혁신의 전망

- 특허 분석

- 규제 상황

- 영향요인

- 성장 촉진요인

- 첨단 운전자 지원 시스템(ADAS) 및 자율 주행 차량

- 차량 안전 및 충돌 방지 강화

- 예측 유지보수 및 차량 관리

- AI 기반 차량 내 인포테인먼트 및 음성 비서

- 업계의 잠재적 위험 및 과제

- 높은 구현 비용 및 통합 복잡성

- 데이터 프라이버시 및 사이버 보안 문제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 하드웨어

- 소프트웨어

- 서비스

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 컴퓨터 비전

- 상황 인식

- 딥러닝

- 머신러닝

- 자연어처리(NLP)

제7장 시장 추계 및 예측 : 프로세스별(2021-2034년)

- 주요 동향

- 데이터 마이닝

- 이미지 인식

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 반자율주행차

- 완전 자율 주행차

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- Alphabet

- Audi

- Bayerische Motoren Werke(BMW)

- Daimler

- Didi Chuxing

- 포드모터

- General Motors

- Harman International Industries

- Honda Motor

- Intel

- International Business Machines(IBM)

- Microsoft

- NVIDIA

- Qualcomm

- Tesla

- Toyota Motor

- Uber Technologies

- Volvo Car

- Waymo

- Xilinx

The Global AI In Automotive Market was valued at USD 4.8 billion in 2024 and is projected to witness a staggering CAGR of 42.8% between 2025 and 2034. This exponential growth reflects the rising demand for intelligent automotive solutions as AI technologies continue to redefine the future of mobility. The integration of AI into vehicles is transforming the way cars operate, elevating both the safety and driving experience of passengers. Leading automakers and technology companies are heavily investing in AI-driven systems, particularly for autonomous vehicles and next-generation Advanced Driver Assistance Systems (ADAS).

AI's role in enhancing vehicle intelligence, situational awareness, and real-time decision-making is pushing the automotive sector toward a future where cars are safer, more connected, and increasingly autonomous. From traffic management and collision avoidance to predictive maintenance and personalized in-car experiences, AI is becoming a central component of modern vehicle architecture. Automakers are also capitalizing on AI to offer predictive navigation, voice recognition, and behavior analysis features, enhancing both driver and passenger convenience. With growing consumer demand for safer and smarter mobility solutions, AI is set to become indispensable in the automotive world, further accelerating market growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $186.4 Billion |

| CAGR | 42.8% |

The surge in AI adoption is largely driven by the increasing implementation of technologies such as ADAS and autonomous driving solutions. AI significantly enhances vehicle safety and overall driving experience through seamless integration with advanced sensors, high-resolution cameras, radar, and LiDAR systems. Features like lane-keeping assistance, adaptive cruise control, automatic emergency braking, and pedestrian detection are powered by AI algorithms that enable vehicles to analyze their surroundings and make instant driving decisions, reducing accidents and improving road safety.

The market is primarily segmented based on processes like data mining and image recognition, with image recognition dominating the landscape. This segment is expected to generate over USD 110 billion by 2034, driven by its critical role in enabling autonomous vehicles and ADAS functionalities. Image recognition technology allows AI systems to process and interpret real-time environmental data, identifying pedestrians, traffic signs, vehicles, and lane markings with precision. The ability to perceive and understand dynamic road conditions makes image recognition a cornerstone of autonomous driving development.

In terms of components, the AI in automotive market is divided into hardware, software, and services, with hardware accounting for a significant 40% share in 2024. Automotive manufacturers are heavily investing in advanced hardware to support the computational demands of AI-powered vehicles. Specialized components such as AI chips, GPUs, sensors, and LiDAR systems are essential to handle vast streams of data for real-time processing, enabling seamless AI functionalities like automated driving, image detection, sensor fusion, and deep learning-based analytics.

The U.S. AI in automotive market commanded a notable 33% share and generated USD 1 billion in 2024, thanks to the country's robust technological infrastructure and rapid AI adoption. Major automakers and tech giants are leading the charge in developing AI-based autonomous driving technologies and advanced safety systems, firmly positioning the U.S. as a key player in shaping the global AI-driven automotive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Technology providers

- 3.1.1.2 OEM Manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Advanced Driver Assistance Systems (ADAS) and Autonomous Vehicles

- 3.5.1.2 Enhanced Vehicle Safety and Collision Avoidance

- 3.5.1.3 Predictive Maintenance and Fleet Management

- 3.5.1.4 AI-powered In-Vehicle Infotainment and Voice Assistants

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High Implementation Costs and Integration Complexity

- 3.5.2.2 Data Privacy and Cybersecurity Concerns

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Service

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Computer vision

- 6.3 Context awareness

- 6.4 Deep learning

- 6.5 Machine learning

- 6.6 Natural Language Processing (NLP)

Chapter 7 Market Estimates & Forecast, By Process, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Data mining

- 7.3 Image recognition

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Semi-Autonomous vehicles

- 8.3 Fully Autonomous vehicles

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alphabet

- 10.2 Audi

- 10.3 Bayerische Motoren Werke (BMW)

- 10.4 Daimler

- 10.5 Didi Chuxing

- 10.6 Ford Motor

- 10.7 General Motors

- 10.8 Harman International Industries

- 10.9 Honda Motor

- 10.10 Intel

- 10.11 International Business Machines (IBM)

- 10.12 Microsoft

- 10.13 NVIDIA

- 10.14 Qualcomm

- 10.15 Tesla

- 10.16 Toyota Motor

- 10.17 Uber Technologies

- 10.18 Volvo Car

- 10.19 Waymo

- 10.20 Xilinx