|

시장보고서

상품코드

1716609

심장 박동 관리(CRM) 장치 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Cardiac Rhythm Management Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

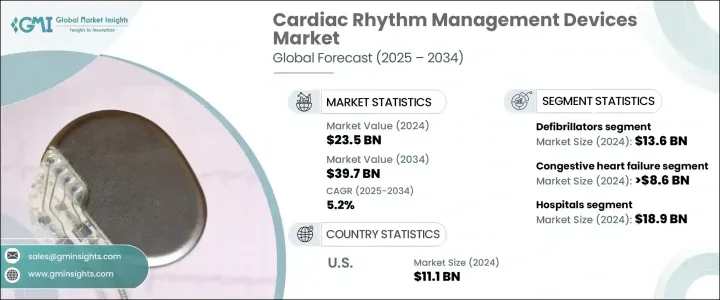

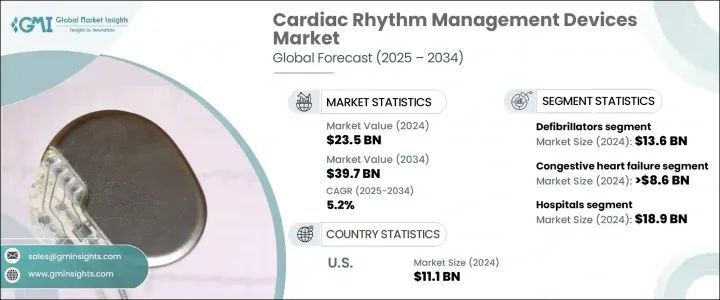

세계의 심장 박동 관리(CRM) 장치 시장은 2024년에 235억 달러에 이르렀고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.2%를 나타낼 것으로 예측됩니다.

이 시장의 성장에는 심부전, 부정맥, 기타 리듬 관련 질환 등 심혈관 질환의 세계 발생률의 상승이 기여하고 있습니다. 현실적인 증가도 시장 확대의 원동력이 되고 있습니다. 앉기 쉬운 라이프 스타일, 식생활의 혼란, 고혈압, 당뇨병, 비만 증가라고 하는 요인이, 첨단 심장 케어 솔루션의 필요성을 한층 더 높이고 있습니다.

심혈관계 질환이 여전히 세계 사망의 주인이기 때문에 환자의 예후를 개선하고 삶의 질을 높일 수 있는 혁신적이고 효과적인 심장 박동 관리(CRM) 장치에 대한 수요가 높아지고 있습니다. 늘어나고 있습니다. 헬스케어 지출의 급증은 조기 진단과 예방적 심장 케어에 대한 의식의 높아짐과 함께 시장 기업에게 새로운 기회를 가져올 것으로 기대되고 있습니다. 지능(AI)과 머신러닝(ML)을 심장 리듬 관리 시스템에 통합하면 예측 분석과 맞춤 치료 옵션을 가능하게 함으로써 향후 시장 동향을 이끌 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 235억 달러 |

| 예측 금액 | 397억 달러 |

| CAGR | 5.2% |

이 시장은 심박조율기, 제세동기, 심장재동기요법(CRT)기기 등 폭넓은 제품 분야로 구성되어 있습니다. 이 장치는 심장 리듬을 지속적으로 모니터링하고 비정상적인 리듬이 감지되면 전기 충격을주고 심장 갑작스런 사망을 예방하도록 설계되었습니다.

심장 박동 관리(CRM) 장치 시장은 용도별로는 울혈성 심부전, 부정맥, 서맥, 빈맥으로 구분됩니다. 이러한 장치는 심장 리듬 조정을 개선하고, 심박출량을 높이고, 피로와 답답함과 같은 증상을 완화하여 환자의 QOL을 향상시켜 심부전 관리에 중요한 역할을 합니다.

미국의 심장 박동 관리(CRM) 장치 시장은 2024년에 111억 달러를 창출해 세계 시장을 석권했습니다. 강력한 임상 연구, 지속적인 제품 혁신, 연구 개발에 많은 투자가 미국에서 심장 박동 관리(CRM) 장치의 급속한 보급을 가능하게 하고, 이 분야에서 세계적 리더로서의 지위를 확고하게 하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심부전 및 기타 심장 질환의 유병률 증가

- 심장 리듬 모니터링의 기술적 진보와 혁신적인 디바이스 도입

- 일반 시민 의식의 고조

- 앉기 쉬운 라이프 스타일 증가

- 유리한 상환 시나리오

- 비만의 유병률 상승과 함께 증가하는 노인 인구 기반

- 업계의 잠재적 위험 및 과제

- 기기의 고비용

- 제품 리콜

- 엄격한 규제 당국의 승인

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 상환 시나리오

- 기술 상황

- 향후 시장 동향

- 가격 분석(2024년)

- 파이프라인 제품

- 적응증의 전망

- 유닛수(2021-2034년)

- 심박 조율기

- 제세동기

- CRT 디바이스

- Porter's Five Forces 분석

- GAP 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 심박 조율기

- 이식형 심박 조율기

- 체외식 심박 조율기

- 제세동기

- 이식형 제세동기(ICD)

- 정맥 이식형 제세동기

- 피하 이식형 제세동기

- 단일 챔버 ICD

- 이중 챔버 ICD

- 체외식 제세동기

- 수동 체외식 제세동기

- 자동 체외식 제세동기

- 반자동 체외식 제세동기

- 전자동 체외식 제세동기

- 장착형 제세동기

- 이식형 제세동기(ICD)

- 심장 재동기 치료 장치

- 심장 재동기 치료 장비-D

- 심장 재동기 치료 장비-P

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 울혈성 심부전

- 부정맥

- 서맥

- 빈맥

- 기타 용도

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 심장치료센터

- 외래수술센터(ASC)

- 기타 최종 용도

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott

- ABIOMED

- Amiitalia

- Asahi Kasei

- BIOTRONIK

- Boston Scientific

- BPL Medical Technologies

- CU Medical

- Defibtech

- LivaNova

- Medico

- Medtronic

- MicroPort

- Nihon Kohden

- Osypka Medical

- Pacetronix

- Philips

- Schiller

- Stryker

- Vitatron

The Global Cardiac Rhythm Management Devices Market reached USD 23.5 billion in 2024 and is projected to expand at a CAGR of 5.2% between 2025 and 2034. The growth of this market is fueled by the rising incidence of cardiovascular diseases worldwide, including heart failure, arrhythmias, and other rhythm-related disorders. The steady increase in aging populations across major economies is also driving market expansion, as older individuals are more prone to cardiac complications. Factors such as sedentary lifestyles, poor dietary habits, and rising cases of hypertension, diabetes, and obesity are further intensifying the need for advanced cardiac care solutions.

With cardiovascular diseases remaining the leading cause of mortality worldwide, there is a growing demand for innovative and effective cardiac rhythm management devices that can improve patient outcomes and enhance quality of life. Additionally, constant advancements in medical technology, including remote monitoring and next-generation implantable devices, are transforming the way healthcare providers manage and treat cardiac rhythm disorders. The surge in healthcare expenditure, coupled with greater awareness about early diagnosis and preventive cardiac care, is expected to open up new opportunities for market players. The integration of artificial intelligence (AI) and machine learning (ML) into cardiac rhythm management systems is also anticipated to drive future market trends by enabling predictive analytics and personalized treatment options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.5 Billion |

| Forecast Value | $39.7 Billion |

| CAGR | 5.2% |

The market comprises a wide range of product segments, including pacemakers, defibrillators, and cardiac resynchronization therapy (CRT) devices. Among these, defibrillators hold the largest market share, contributing significantly to the overall revenue. Defibrillators, especially implantable cardioverter defibrillators (ICDs), are vital for patients at high risk of life-threatening arrhythmias. These devices are designed to monitor heart rhythms continuously and deliver electric shocks when abnormal rhythms are detected, thereby preventing sudden cardiac death. The demand for defibrillators is expected to rise steadily as cardiovascular conditions continue to be a leading cause of morbidity and mortality globally.

In terms of application, the cardiac rhythm management devices market is segmented into congestive heart failure, arrhythmias, bradycardia, and tachycardia. Among these, congestive heart failure accounted for USD 8.6 billion in 2024. Devices like ICDs and CRT systems play a crucial role in managing heart failure by improving heart rhythm coordination, enhancing cardiac output, and alleviating symptoms such as fatigue and breathlessness, thereby improving patient quality of life.

The United States Cardiac Rhythm Management Devices Market generated USD 11.1 billion in 2024, dominating the global landscape. The country's advanced healthcare infrastructure, coupled with favorable reimbursement frameworks and broad access to state-of-the-art treatment options, continues to propel market growth. Strong clinical research, ongoing product innovations, and significant investments in R&D are enabling the rapid adoption of CRM devices in the U.S., solidifying its position as a global leader in this space.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of heart failure and other cardiac disorders

- 3.2.1.2 Technological advancements and introduction of innovative devices for cardiac rhythm monitoring

- 3.2.1.3 Increasing public awareness

- 3.2.1.4 Rising sedentary lifestyle

- 3.2.1.5 Favorable reimbursement scenario

- 3.2.1.6 Growing geriatric population base coupled with rising prevalence of obesity

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Product recalls

- 3.2.2.3 Stringent regulatory approvals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Pricing analysis, 2024

- 3.9 Pipeline products

- 3.10 Indication landscape

- 3.11 Number of units, 2021 - 2034

- 3.11.1 Pacemaker

- 3.11.2 Defibrillators

- 3.11.3 CRT devices

- 3.12 Porter's analysis

- 3.13 GAP analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Company market share analysis

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pacemakers

- 5.2.1 Implantable pacemakers

- 5.2.2 External pacemakers

- 5.3 Defibrillators

- 5.3.1 Implantable cardioverter defibrillator (ICDs)

- 5.3.1.1 Transvenous implantable cardioverter defibrillator

- 5.3.1.2 Subcutaneous implantable cardioverter defibrillator

- 5.3.1.2.1 Single-chamber ICDs

- 5.3.1.2.2 Dual-chamber ICDs

- 5.3.2 External defibrillator

- 5.3.2.1 Manual external defibrillator

- 5.3.2.2 Automated external defibrillator

- 5.3.2.2.1 Semi-automated external defibrillator

- 5.3.2.2.2 Fully automated external defibrillator

- 5.3.2.3 Wearable cardioverter defibrillator

- 5.3.1 Implantable cardioverter defibrillator (ICDs)

- 5.4 Cardiac resynchronization therapy devices

- 5.4.1 Cardiac resynchronization therapy devices- D

- 5.4.2 Cardiac resynchronization therapy devices- P

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Congestive heart failure

- 6.3 Arrhythmias

- 6.4 Bradycardia

- 6.5 Tachycardia

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cardiac care centers

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 ABIOMED

- 9.3 Amiitalia

- 9.4 Asahi Kasei

- 9.5 BIOTRONIK

- 9.6 Boston Scientific

- 9.7 BPL Medical Technologies

- 9.8 CU Medical

- 9.9 Defibtech

- 9.10 LivaNova

- 9.11 Medico

- 9.12 Medtronic

- 9.13 MicroPort

- 9.14 Nihon Kohden

- 9.15 Osypka Medical

- 9.16 Pacetronix

- 9.17 Philips

- 9.18 Schiller

- 9.19 Stryker

- 9.20 Vitatron