|

시장보고서

상품코드

1716674

산업용 펌프 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Industrial Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

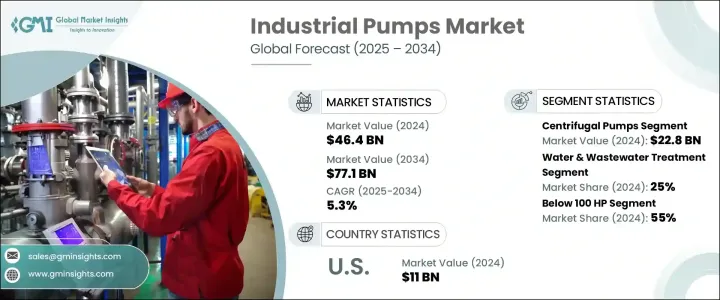

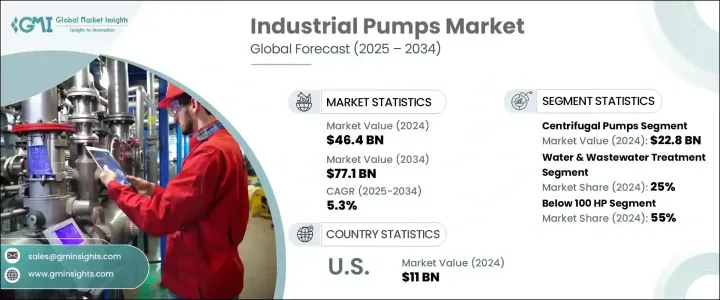

세계의 산업용 펌프 시장은 2024년 464억 달러로 평가되었으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.3%를 나타낼 것으로 예측됩니다.

이 성장의 주요 요인은 다양한 산업에서 수요 증가, 펌프 시스템의 기술 진보, 세계의 급속한 산업화입니다. 현재의 요구는 계속 증가하고 있으며, 석유, 가스, 폐수 처리, 광업, 화학 등의 분야에서의 용도가 증가하고 있는 것이 시장의 성장에 박차를 가하고 있습니다. 가능한 물 관리 기술로의 전환은 현대적이고 에너지 효율적인 펌프에 대한 요구를 더욱 강화하고 있습니다. 증가에 따라 산업용 펌프 수요가 급증하고 있습니다. 스마트팜프 기술과 IoT 대응 시스템의 채용이 업계 정세를 재구축하고 있으며, 산업계는 업무 효율의 향상과 에너지 소비의 삭감을 실현하고 있습니다.

시장은 원심 펌프, 용적 펌프, 다이어프램 펌프, 기어 펌프, 스크류 펌프 등을 포함한 펌프 유형별로 구분됩니다. 2024년 원심펌프 분야는 석유 및 가스, 물관리, 화학처리 등의 산업에서 널리 응용되었기 때문에 228억 달러를 창출하였습니다. 용적식 펌프는 점성이 높은 유체를 효율적으로 처리하는 것으로 알려져 있으며, 수압 파쇄에 있어서의 사용 증가나 노후화된 인프라의 갱신에 의해 꾸준한 성장이 전망되고 있습니다. 이 동향은 특히 에너지 부문에 많은 투자를 하고 있는 국가에서 두드러지며, 고성능 펌프는 채굴, 정제, 운송 공정 최적화에 필수적입니다. 산업계가 생산성 향상과 다운타임 최소화에 주력하는 동안 신뢰성과 운전 효율을 제공하는 고급 펌프 시스템에 대한 수요는 계속 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 464억 달러 |

| 예측 금액 | 771억 달러 |

| CAGR | 5.3% |

산업용 펌프 시장은 또한 상하수도처리, 화학, 석유화학, 광업, 식음료, 건설, 석유 및 가스, 의약품, 해양, 펄프·제지, 기타 등 최종 이용 산업별로 구분됩니다. 2024년 시장 점유율은 상하수도 처리가 25%를 차지했지만, 이는 급속한 도시화와 산업 성장 속에서 청결한 물 관리에 대한 요구가 높아지고 있음을 반영한 것입니다. 개발도상 지역에서 인구가 증가함에 따라 효율적인 수처리 및 폐수 관리 솔루션의 필요성이 점점 높아지고 있습니다.

미국의 산업용 펌프 시장은 80%의 점유율을 차지하며, 2024년에는 110억 달러를 창출했습니다. 이송과 같은 공정에서 광범위하게 사용되는 산업용 펌프 수요를 크게 견인하고 있습니다. 또한, 광업 부문의 미국 경제에 대한 공헌은 건설, 자동차, 항공우주 등의 산업에 필수적인 재료를 공급하는 중요한 역할과 함께 산업용 펌프의 견조한 수요를 더욱 뒷받침하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴적 혁신

- 향후 전망

- 제조업자

- 유통업체

- 공급자의 상황

- 기술적 전망

- 주요 뉴스 및 이니셔티브

- 규제 상황

- 영향요인

- 성장 촉진요인

- 최종 이용 산업에서의 수요 증가

- 세계의 산업화와 제조업의 확대

- 업계의 잠재적 위험 및 과제

- 높은 설비 투자

- 높은 에너지 소비

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계·예측 : 펌프 유형별(2021-2034년)

- 주요 동향

- 원심 펌프

- 양변위 펌프

- 다이어프램 펌프

- 기어 펌프

- 스크류 펌프

- 기타(피스톤 펌프, 프로그레시브 캐비티 펌프 등)

제6장 시장 추계·예측 : 동력원별(2021-2034년)

- 주요 동향

- 전기 및 태양열 펌프

- 디젤 펌프

- 기타(가솔린 태양열 등)

제7장 시장 추계·예측 : 유량별(2021-2034년)

- 주요 동향

- 100m³/h 미만

- 100-500 m³/h

- 500m³/h 이상

제8장 시장 추계·예측 : 동력별(2021-2034년)

- 주요 동향

- 100HP 미만

- 100-500HP

- 500HP 이상

제9장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 기존

- 스마트

제10장 시장 추계·예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 물 및 폐수 처리

- 화학 및 석유화학

- 광업

- 식음료

- 건설

- 석유 및 가스

- 제약

- 해양

- 펄프 및 제지

- 기타(농업, 섬유 등)

제11장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 간접 판매

제12장 지역별 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- UAE

- 사우디아라비아

- 남아프리카

제13장 기업 프로파일

- Atlas Copco

- Ebara

- Flowserve

- Gardner Denver

- Gorman-Rupp

- Grundfos

- ITT

- Kirloskar

- KSB

- SPX Flow

- Sulzer

- Tsurumi

- Weir

- Wilo

- Xylem

The Global Industrial Pumps Market, valued at USD 46.4 billion in 2024, is projected to grow at a CAGR of 5.3% from 2025 to 2034. This growth is primarily driven by rising demand across various industries, technological advancements in pumping systems, and rapid industrialization worldwide. As economies expand and manufacturing sectors thrive, the need for efficient, durable, and high-performance industrial pumps continues to escalate. Increasing applications in sectors such as oil and gas, water and wastewater treatment, mining, and chemicals are fueling market growth. Moreover, the transition toward sustainable water management practices, coupled with rising environmental regulations, has further elevated the need for modern and energy-efficient pumps. Emerging markets, especially in Asia Pacific and Latin America, are witnessing surging demand for industrial pumps due to rapid urbanization and increasing investments in infrastructure development. The adoption of smart pump technologies and IoT-enabled systems is reshaping the landscape, allowing industries to improve operational efficiency and reduce energy consumption.

The market is segmented by pump type, including centrifugal pumps, positive displacement pumps, diaphragm pumps, gear pumps, screw pumps, and others. In 2024, the centrifugal pumps segment generated USD 22.8 billion, owing to its widespread application in industries such as oil and gas, water management, and chemical processing. Positive displacement pumps, known for their efficiency in handling viscous fluids, are expected to witness steady growth, driven by increasing use in hydraulic fracturing and the replacement of aging infrastructure. This trend is particularly noticeable in countries investing heavily in their energy sectors, where high-performance pumps are essential for optimizing extraction, refining, and transportation processes. As industries focus on enhancing productivity and minimizing downtime, the demand for advanced pumping systems that offer reliability and operational efficiency continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46.4 Billion |

| Forecast Value | $77.1 Billion |

| CAGR | 5.3% |

The industrial pumps market is further segmented by end-use industries, including water and wastewater treatment, chemicals, petrochemicals, mining, food and beverages, construction, oil and gas, pharmaceuticals, marine, pulp and paper, and others. Water and wastewater treatment accounted for a 25% market share in 2024, reflecting the growing need for clean water management amid rapid urbanization and industrial growth. As population increases, especially in developing regions, the need for efficient water treatment and wastewater management solutions continues to intensify. Pumps also play a critical role in the mining industry, where dewatering pumps remove excess water from mines to ensure safety and operational efficiency. Additionally, the food and beverage sector relies heavily on specialized pumps for hygienic processing and maintaining product integrity.

The United States Industrial Pumps Market commanded an 80% share, generating USD 11 billion in 2024. This dominance is attributed to technological advancements, growing industrial activity, and an increasing focus on sustainable water management. The U.S. oil and gas industry, particularly shale oil production, remains a significant driver of demand for industrial pumps, which are used extensively in processes such as extraction, refining, and transportation. Additionally, the mining sector's contributions to the U.S. economy, coupled with its critical role in supplying essential materials to industries like construction, automotive, and aerospace, further support the robust demand for industrial pumps.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Technological landscape

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand from end use industries

- 3.6.1.2 Global industrialization and manufacturing expansion

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High capital investment

- 3.6.2.2 High energy consumption

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Pump Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Centrifugal pumps

- 5.3 Positive displacement pumps

- 5.4 Diaphragm pumps

- 5.5 Gear pumps

- 5.6 Screw pumps

- 5.7 Others (piston pumps, progressive cavity pumps, etc.)

Chapter 6 Market Estimates & Forecast, By Power Source, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Electric & solar pumps

- 6.3 Diesel pumps

- 6.4 Others (gasoline solar etc.)

Chapter 7 Market Estimates & Forecast, By Flow Rate, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Below 100 m³/h

- 7.3 100 - 500 m³/h

- 7.4 Above 500 m³/h

Chapter 8 Market Estimates & Forecast, By Power, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Below 100 HP

- 8.3 100 - 500 HP

- 8.4 Above 500 HP

Chapter 9 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Conventional

- 9.3 Smart

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Water & wastewater treatment

- 10.3 Chemicals and petrochemicals

- 10.4 Mining

- 10.5 Food and beverages

- 10.6 Construction

- 10.7 Oil & gas

- 10.8 Pharmaceutical

- 10.9 Marine

- 10.10 Pulp & paper

- 10.11 Others (agricultural, textile etc.)

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct sales

- 11.3 Indirect sales

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 Saudi Arabia

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Atlas Copco

- 13.2 Ebara

- 13.3 Flowserve

- 13.4 Gardner Denver

- 13.5 Gorman-Rupp

- 13.6 Grundfos

- 13.7 ITT

- 13.8 Kirloskar

- 13.9 KSB

- 13.10 SPX Flow

- 13.11 Sulzer

- 13.12 Tsurumi

- 13.13 Weir

- 13.14 Wilo

- 13.15 Xylem