|

시장보고서

상품코드

1716681

전기 집진기 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Electrostatic Precipitator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

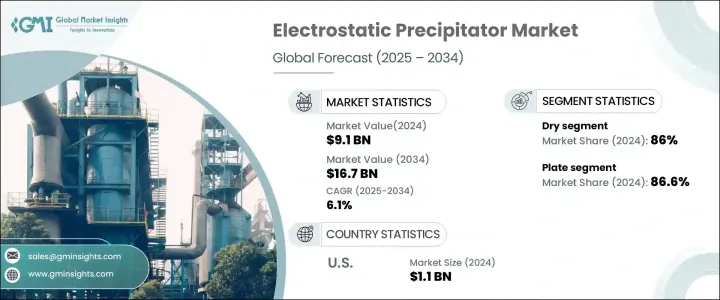

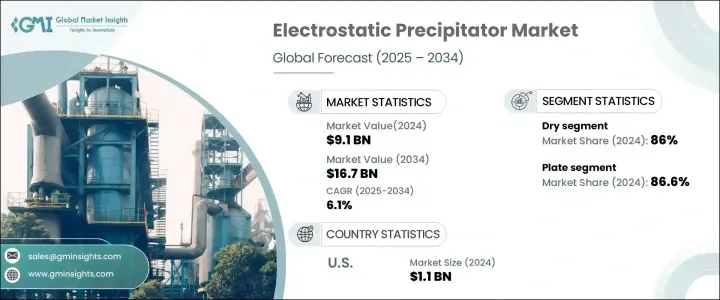

전기 집진기 세계 시장은 2024년에 91억 달러로 평가되며, 2025년부터 2034년까지 연평균 6.1%의 성장률을 보일 것으로 예상됩니다.

이러한 성장의 주요 원동력은 신흥국의 급속한 산업화로 제철, 화학 생산, 석탄 화력 발전과 같은 산업이 계속 확대되고 있습니다. 이러한 산업이 성장함에 따라 효율적인 배출가스 제어 시스템에 대한 수요가 점점 더 중요해지고 있습니다. 세계 각국 정부는 엄격한 환경 규제를 시행하고 있으며, 산업계는 대기 오염을 효과적으로 관리하기 위해 첨단 기술을 도입해야 합니다. 산업 배출물에서 미립자 물질을 효율적으로 제거하는 능력으로 잘 알려진 전기 집진기는 산업계가 이러한 엄격한 기준을 준수하기 위해 노력하는 가운데 많은 지지를 받고 있습니다. 또한, 환경 지속가능성과 유해 배출물 감소의 중요성에 대한 인식이 높아지면서 산업계는 신뢰할 수 있는 대기 오염 방지 기술에 대한 투자를 늘리고 있습니다.

지속가능한 산업 관행에 대한 관심이 높아지고 대기 질에 대한 대중의 인식이 높아지면서 전기 집진기에 대한 수요가 더욱 증가하고 있습니다. 다양한 산업 분야의 기업들은 진화하는 환경 기준을 충족하고 이산화탄소 배출을 최소화하기 위해 오염 방지 시스템을 현대화할 필요성을 인식하고 있습니다. 신흥 경제권, 특히 아시아태평양에서는 산업 활동의 확대와 각국 정부의 대기질 규제 강화로 인해 전기 집진기에 대한 수요가 급증하고 있습니다. 또한, 에너지 효율과 입자 제거 능력의 향상과 같은 전기 집진 기술의 발전은 업무 효율성과 환경 규정 준수를 동시에 추구하는 산업계에 전기 집진 시스템의 매력을 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 91억 달러 |

| 예상 금액 | 167억 달러 |

| CAGR | 6.1% |

건식 전기 집진기는 2024년 시장 점유율의 86%를 차지하며, 배기가스에서 미립자 물질을 효율적으로 제거해야 하는 산업에서 그 인기를 반영하고 있습니다. 이러한 시스템은 엄격한 환경 규제 준수가 필수적인 시멘트 및 철강 생산과 같은 분야에서 특히 선호되고 있습니다. 건식 전기 집진기는 낮은 운영 비용으로 고효율로 미립자를 포집할 수 있기 때문에 신뢰할 수 있는 배출 제어 솔루션을 원하는 산업 분야에서 선호되고 있습니다.

설계에 따라 시장은 판형과 관형 부문으로 나뉘며, 판형 전기 집진기는 2024년 86.6%의 점유율을 차지했습니다. 판형 전기 집진기는 최소한의 에너지 소비로 건식 및 습식 입자를 모두 포집할 수 있기 때문에 산업 응용 분야에서 널리 사용됩니다. 낮은 운영 비용과 높은 효율성으로 인해 신뢰할 수 있는 오염 방지 기술이 필요한 산업에 이상적인 솔루션입니다.

미국의 전기 집진기 시장은 오염 방지 기술에 대한 지속적인 투자와 대기질 규제 강화로 2024년 11억 달러 규모의 시장을 창출했습니다. 대기 질에 대한 사회적 관심이 높아짐에 따라 전기 집진기 채택이 더욱 증가하여 향후 몇 년 동안 지속적인 시장 성장에 기여할 것으로 예상됩니다. 깨끗한 공기에 대한 수요 증가와 산업계가 환경 준수 기준을 충족해야 하는 필요성이 미국 전기 집진기 시장의 성장을 뒷받침하는 주요 요인입니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계

- 규제 상황

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크와 과제

- 성장 가능성 분석

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 전략 대시보드

- 혁신과 테크놀러지 전망

제5장 시장 규모 및 예측 : 시스템별, 2021-2034년

- 주요 동향

- 건식

- 습식

제6장 시장 규모 및 예측 : 설계별, 2021-2034년

- 주요 동향

- 플레이트

- 튜블러

제7장 시장 규모 및 예측 : 발광 산업별, 2021-2034년

- 주요 동향

- 발전

- 화학·석유화학

- 시멘트

- 금속 가공·광업

- 제조업

- 해양

- 기타

제8장 시장 규모 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 인도네시아

- 호주

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 남아프리카공화국

- 나이지리아

- 앙골라

- 라틴아메리카

- 브라질

- 아르헨티나

- 칠레

- 페루

제9장 기업 개요

- Babcock and Wilcox Enterprises

- DURR Group

- DUCON

- FLSmidth

- Fuel Tech

- GEA Group

- GEECO Enercon

- KC Cottrell India

- Monroe Environmental

- Mitsubishi Heavy Industries.

- Sumitomo Heavy Industries

- Trion

- Valmet

- Wood

The Global Electrostatic Precipitator Market generated USD 9.1 billion in 2024 and is projected to grow at a CAGR of 6.1% between 2025 and 2034. This growth is primarily driven by the rapid industrialization of emerging economies, where industries such as steel manufacturing, chemical production, and coal-based power generation continue to expand. As these industries grow, the demand for efficient emissions control systems becomes increasingly critical. Governments worldwide are enforcing strict environmental regulations that require industries to implement advanced technologies to manage air pollution effectively. Electrostatic precipitators, known for their ability to efficiently remove particulate matter from industrial emissions, are gaining traction as industries strive to comply with these stringent standards. Additionally, growing awareness about environmental sustainability and the importance of reducing harmful emissions is pushing industries to invest in reliable air pollution control technologies.

The increasing focus on sustainable industrial practices, along with heightened public awareness of air quality concerns, is further amplifying the demand for electrostatic precipitators. Companies across various industries are recognizing the need to modernize their pollution control systems to meet evolving environmental standards and minimize their carbon footprint. Emerging economies, particularly in Asia-Pacific, are witnessing a surge in demand for electrostatic precipitators as industrial operations expand and governments enforce more rigorous air quality regulations. Moreover, advancements in ESP technology, including improvements in energy efficiency and particle removal capacity, are enhancing the appeal of these systems for industries aiming to balance operational efficiency with environmental compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.1 Billion |

| Forecast Value | $16.7 Billion |

| CAGR | 6.1% |

The dry electrostatic precipitator segment accounted for 86% of the market share in 2024, reflecting its popularity in industries that require efficient removal of particulate matter from flue gases. These systems are particularly favored in sectors such as cement and steel production, where maintaining compliance with strict environmental regulations is essential. Dry electrostatic precipitators offer high efficiency in capturing fine particles while keeping operational costs low, making them a preferred choice for industries seeking reliable emissions control solutions.

By design, the market is divided into plate and tubular segments, with plate electrostatic precipitators capturing an 86.6% share in 2024. Plate ESPs are widely used in industrial applications due to their ability to capture both dry and wet particles with minimal energy consumption. Their low operating costs and high efficiency make them an ideal solution for industries that need dependable pollution control technologies.

The US electrostatic precipitator market generated USD 1.1 billion in 2024, driven by continued investments in pollution control technologies and the implementation of stricter air quality regulations. As public concern about air quality intensifies, the adoption of electrostatic precipitators is expected to increase further, contributing to sustained market growth in the coming years. The rising demand for cleaner air and the need for industries to meet environmental compliance standards are key factors supporting the expansion of the US electrostatic precipitator market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By System, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Dry

- 5.3 Wet

Chapter 6 Market Size and Forecast, By Design, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Plate

- 6.3 Tubular

Chapter 7 Market Size and Forecast, By Emitting Industry, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Power generation

- 7.3 Chemicals and petrochemicals

- 7.4 Cement

- 7.5 Metal processing & mining

- 7.6 Manufacturing

- 7.7 Marine

- 7.8 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Indonesia

- 8.4.6 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.5.4 Nigeria

- 8.5.5 Angola

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 Babcock and Wilcox Enterprises

- 9.2 DURR Group

- 9.3 DUCON

- 9.4 FLSmidth

- 9.5 Fuel Tech

- 9.6 GEA Group

- 9.7 GEECO Enercon

- 9.8 KC Cottrell India

- 9.9 Monroe Environmental

- 9.10 Mitsubishi Heavy Industries.

- 9.11 Sumitomo Heavy Industries

- 9.12 Trion

- 9.13 Valmet

- 9.14 Wood