|

시장보고서

상품코드

1716685

하이드로닉 펌프 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Hydronic Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

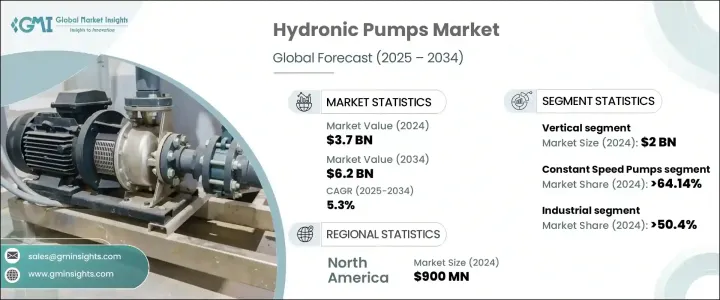

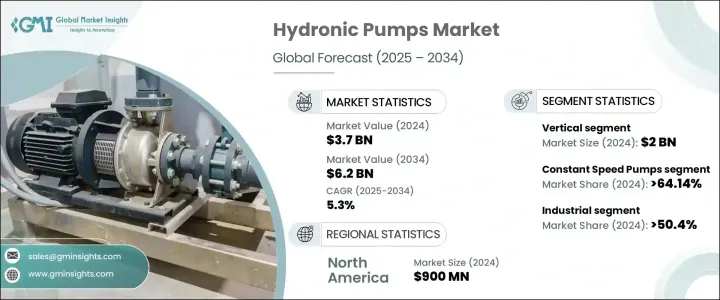

하이드로닉 펌프 세계 시장은 2024년 37억 달러로 평가되며, 2025년부터 2034년까지 연평균 5.3%로 성장할 것으로 예상됩니다.

에너지 효율과 지속가능성에 대한 요구가 높아지면서 특히 난방, 환기 및 공조(HVAC) 시스템에서 하이드로닉 펌프의 채택을 촉진하고 있습니다. 미국의 에너지 스타, 유럽연합(EU)의 에너지스타, 유럽연합(EU)의 유사한 지침 등 정부 및 규제 기관이 엄격한 환경 기준을 시행하는 가운데, 에너지 효율이 높은 기술을 요구하는 움직임은 계속 강화되고 있습니다. 이산화탄소 배출량과 운영 비용 절감에 대한 관심이 높아지면서 산업계는 주거 및 상업용 인프라에 하이드로닉 펌프 시스템을 통합하는 것을 장려하고 있습니다.

이러한 펌프는 효율적인 열 및 유체 순환을 보장하여 에너지 소비를 최적화하는 데 중요한 역할을 하며, 현대 건축 시스템에서 필수적인 구성요소로 자리 잡았습니다. 또한, IoT 기능을 갖춘 스마트 펌프와 같은 펌프 설계의 기술적 발전은 시스템 효율을 높이고 다운타임을 줄이는 실시간 모니터링 및 예지보전을 제공함으로써 상황을 변화시키고 있습니다. 전 세계적으로 그린 빌딩 개념의 채택이 증가함에 따라 시장 성장을 더욱 촉진하고 있습니다. 부동산 개발업체들이 에너지를 고려한 설계에 초점을 맞추고 있는 가운데, 하이드로닉 펌프는 지속가능성 목표를 달성하는 데 필수적인 요소로 자리 잡고 있습니다. 기후 변화에 대한 인식이 높아지고 에너지 절약 솔루션을 도입할 필요성이 높아지면서 시장의 장기적인 전망이 더욱 밝아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 37억 달러 |

| 예상 금액 | 62억 달러 |

| CAGR | 5.3% |

수직형 하이드로닉 펌프 부문은 2024년 20억 달러 규모에 달했으며, 2034년까지 연평균 5.4%의 성장률을 보일 것으로 예상됩니다. 수직형 펌프는 적은 공간에서 고압 시스템을 처리할 수 있는 능력으로 인해 인기를 끌고 있습니다. 컴팩트한 설계로 인해 공간 제약이 우려되는 상업, 산업 및 HVAC 환경에서 사용하기에 이상적입니다. 이 펌프는 제한된 환경에서 냉난방용 물과 기타 유체를 순환시키는 데 매우 효율적이기 때문에 신뢰할 수 있는 고압 성능을 필요로 하는 다양한 산업 분야에서 선호되고 있습니다. 도시화가 가속화되고 건물 설계가 공간 최적화를 우선시함에 따라 수직형 수열 펌프에 대한 수요는 크게 증가할 것으로 예상됩니다.

정속 펌프는 2024년 64%의 시장 점유율을 차지했으며, 2034년까지 5%의 안정적인 성장률을 유지할 것으로 예상됩니다. 이 펌프는 주거용 및 상업용 냉난방 시스템과 같이 일정한 유량이 필요한 시스템에서 일반적으로 사용됩니다. 일정한 속도로 작동하도록 설계된 정속 펌프는 예측 가능하고 신뢰할 수 있는 유체 순환을 제공하여 저수요 환경에 이상적입니다. 특히, 주거용 및 상업용 분야에서 신뢰할 수 있는 HVAC 시스템에 대한 요구가 증가함에 따라 정속 펌프의 작동 안정성과 효율성이 지속적으로 채택의 원동력이 되고 있습니다.

북미 수열 펌프 시장은 26.4%의 점유율을 차지하며 2024년 9억 달러 규모의 시장을 형성했습니다. 이 지역에서는 에너지 효율 규제가 강화되고 있으며, 이는 건설 부문이 고성능 수열 펌프를 포함한 에너지 절약 기술을 채택하는 원동력이 되고 있습니다. 건축 프로젝트에서 지속가능성에 대한 중요성이 계속 강조됨에 따라, 진화하는 에너지 표준을 충족하는 펌프에 대한 수요가 계속 증가하고 있습니다. 또한, 아시아태평양에서는 특히 농업 분야에서 눈에 띄는 성장을 보이고 있으며, 농법의 현대화 및 기계화로 인해 수열 펌프의 사용이 증가하고 있습니다. 다양한 산업 분야에서 수열 펌프의 적용 범위가 확대됨에 따라 향후 몇 년 동안 세계 시장의 성장 궤도에 힘을 실어줄 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 가격 분석

- 테크놀러지와 혁신 전망

- 주요 뉴스와 이니셔티브

- 규제 상황

- 제조업체

- 판매업체

- 소매업체

- 영향요인

- 성장 촉진요인

- 에너지 효율에 관한 규제와 기준

- 건설 활동 확대

- 재생에너지의 통합

- 도시화와 인프라 개발

- 업계의 잠재적 리스크와 과제

- 시장 포화와 치열한 경쟁

- 고액의 초기 투자

- 성장 촉진요인

- 성장 가능성 분석

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정과 예측 : 유형별, 2021-2034년

- 주요 동향

- 수직형

- 수평형

제6장 시장 추정과 예측 : 속도별, 2021-2034년

- 주요 동향

- 정속 펌프

- 가변속 펌프

제7장 시장 추정과 예측 : GPM 유량별, 2021-2034년

- 주요 동향

- 1 GPM 미만

- 1-2 GPM 미만

- 2-5GPM

- 5-10GPM

- 10-15 GPM

- 15 GPM 이상

제8장 시장 추정과 예측 : 전력별, 2021-2034년

- 주요 동향

- 100W 미만

- 100-500W

- 500W 이상

제9장 시장 추정과 예측 : 용도별, 2021-2034년

- 주요 동향

- 온수

- 냉수

- 증기

제10장 시장 추정과 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 주거용

- 상업용

- 산업용

제11장 시장 추정과 예측 : 유통 채널별, 2021-2034년

- 주요 동향

- 직접

- 간접 판매

제12장 시장 추정과 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제13장 기업 개요

- Armstrong Fluid Technology

- Biral AG

- DAB Pumps

- Danfoss

- Flowserve Corporation

- Franklin Electric

- Grundfos

- ITT Inc.

- KSB Group

- Pentair plc

- Sulzer Ltd.

- Taco Comfort Solutions

- Uponor Corporation

- Wilo

- Xylem Inc.

The Global Hydronic Pumps Market was valued at USD 3.7 billion in 2024 and is projected to grow at a CAGR of 5.3% between 2025 and 2034. Increasing demand for energy efficiency and sustainability is driving the adoption of hydronic pumps, particularly in heating, ventilation, and air conditioning (HVAC) systems. As governments and regulatory bodies enforce stringent environmental standards, such as Energy Star in the United States and similar directives in the European Union, the push for energy-efficient technologies continues to intensify. The growing emphasis on reducing carbon emissions and operational costs is encouraging industries to integrate hydronic pump systems into both residential and commercial infrastructure.

These pumps play a crucial role in optimizing energy consumption by ensuring efficient heat and fluid circulation, making them a vital component in modern building systems. Additionally, technological advancements in pump designs, such as smart pumps with IoT capabilities, are transforming the landscape by offering real-time monitoring and predictive maintenance, which enhances system efficiency and reduces downtime. The rising adoption of green building initiatives across the globe is further propelling market growth. As property developers focus on energy-conscious designs, hydronic pumps are becoming essential in meeting sustainability goals. The growing awareness about climate change and the need to implement energy-saving solutions is boosting the market's long-term prospects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 5.3% |

The vertical hydronic pump segment accounted for USD 2 billion in 2024 and is expected to grow at a CAGR of 5.4% through 2034. Vertical pumps are gaining traction due to their ability to handle high-pressure systems while occupying less space. Their compact design makes them ideal for applications in commercial, industrial, and HVAC settings where space constraints are a concern. These pumps are highly efficient in circulating water or other fluids for heating and cooling in confined environments, which makes them a preferred choice in various industries that require reliable, high-pressure performance. As urbanization accelerates and building designs prioritize space optimization, the demand for vertical hydronic pumps is set to increase significantly.

Constant speed pumps held a 64% market share in 2024 and are expected to maintain a steady growth rate of 5% through 2034. These pumps are commonly used in systems requiring a consistent flow rate, such as residential and commercial heating and cooling systems. Designed to operate at a fixed speed, constant-speed pumps provide predictable and reliable fluid circulation, making them ideal for low-demand environments. Their operational stability and efficiency continue to drive their adoption, particularly as the need for reliable HVAC systems grows in both residential and commercial sectors.

North America hydronic pumps market accounted for a 26.4% share and generated USD 900 million in 2024. Stricter energy efficiency regulations in the region are driving the construction sector to adopt energy-saving technologies, including high-performance hydronic pumps. The ongoing emphasis on sustainability in building projects continues to fuel demand for these pumps, ensuring compliance with evolving energy standards. In addition, the Asia Pacific region has witnessed remarkable growth, particularly in the agricultural sector, where modernization and mechanization of farming practices have increased the use of hydronic pumps. The expanding scope of hydronic pump applications in diverse industries is expected to bolster the global market's growth trajectory over the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.4.2.1 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.3 Pricing analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Manufacturers

- 3.8 Distributors

- 3.9 Retailers

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Energy efficiency regulations and standards

- 3.10.1.2 Growing construction activities

- 3.10.1.3 Renewable energy integration

- 3.10.1.4 Urbanization and infrastructure development

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Market saturation and intense competition

- 3.10.2.2 High initial investment

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Vertical

- 5.3 Horizontal

Chapter 6 Market Estimates & Forecast, By Speed, 2021-2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Constant speed pumps

- 6.3 Variable speed pumps

Chapter 7 Market Estimates & Forecast, By GPM Flow, 2021-2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Below 1GPM

- 7.3 1-2 GPM

- 7.4 2-5 GPM

- 7.5 5-10 GPM

- 7.6 10-15 GPM

- 7.7 Above 15 GPM

Chapter 8 Market Estimates & Forecast, By Power, 2021-2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Upto 100W

- 8.3 100-500W

- 8.4 Above 500W

Chapter 9 Market Estimates & Forecast, By Usage, 2021-2034 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Heated water

- 9.3 Chilled water

- 9.4 Steam

Chapter 10 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial

- 10.4 Industrial

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Armstrong Fluid Technology

- 13.2 Biral AG

- 13.3 DAB Pumps

- 13.4 Danfoss

- 13.5 Flowserve Corporation

- 13.6 Franklin Electric

- 13.7 Grundfos

- 13.8 ITT Inc.

- 13.9 KSB Group

- 13.10 Pentair plc

- 13.11 Sulzer Ltd.

- 13.12 Taco Comfort Solutions

- 13.13 Uponor Corporation

- 13.14 Wilo

- 13.15 Xylem Inc.