|

시장보고서

상품코드

1721410

도파민 작용제 시장 : 기회 및 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Dopamine Agonists Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

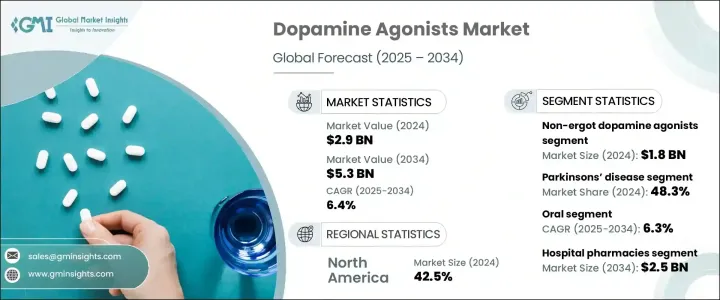

세계의 도파민 작용제 시장은 2024년 29억 달러로 평가되었고, 2034년에는 53억 달러에 이를 것으로 추정되며, CAGR 6.4%로 성장할 전망입니다. 이러한 꾸준한 성장은 파킨슨병과 하지불안증후군(RLS)과 같은 신경 퇴행성 질환의 전 세계적인 급증으로 인해 고급 신경 치료제에 대한 수요가 증가하고 있음을 반영합니다. 인구 고령화, 앉아서 생활하는 생활 방식, 스트레스 증가로 인해 신경 장애가 점점 더 흔해지면서 의료 서비스 제공자들은 조기 발견과 개입에 더욱 중점을 두고 있습니다.

환자들이 사용 가능한 치료 옵션에 대해 더 많이 알게 되면서 진단율이 높아지고 있으며, 환자들은 이전보다 더 빨리 효과적인 약물 요법을 받고 있습니다. 이와 동시에 제약 혁신은 계속해서 시장을 발전시키고 있습니다. 기업들은 우수한 효능과 부작용을 줄인 차세대 도파민 작용제에 적극적으로 투자하고 있습니다. 경피 패치 및 서방형 정제와 같은 약물 전달 시스템의 개선으로 치료 경험이 변화하고 복약 순응도가 향상되고 있습니다. 선진국과 신흥국 모두에서 의료 투자 증가와 기술 발전으로 신경계 질환 치료 환경이 재편되면서 도파민 작용제 분야의 지속적인 시장 성장에 유리한 조건이 조성되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 29억 달러 |

| 예측 금액 | 53억 달러 |

| CAGR | 6.4% |

비에르고트계 도파민 작용제는 2024년에 18억 달러의 가치를 창출하여 이 치료 분야에서 지배적인 약물군으로 자리매김했습니다. 현재 임상의들은 보다 안전한 프로파일과 심혈관 및 섬유성 합병증 위험이 현저히 낮기 때문에 기존의 에르고트 기반 옵션보다 이러한 약물을 선호하고 있습니다. 또한 1일 1회 투약의 편리함과 사용자 친화적인 경피 도포가 가능해지면서 더 많은 환자들이 비에르고트 대체제를 찾고 있습니다. 제약 회사들은 더 나은 내약성과 장기적인 혜택을 제공하는 혁신적인 화합물을 개발하기 위해 R&D에 집중하고 있습니다. 이러한 개선된 옵션이 더 널리 사용 가능해짐에 따라 의사들은 1차 치료제로 이를 점점 더 많이 추천하고 있으며, 이는 주요 시장에서 처방량을 늘리고 환자 치료 결과를 개선하고 있습니다.

파킨슨병 부문은 2024년 전체 시장에서 48.3%의 점유율을 차지하며 도파민 작용제의 최대 응용 분야로서의 입지를 유지할 것으로 예상됩니다. 파킨슨병은 전 세계적으로 두 번째로 흔한 신경 퇴행성 질환으로, 특히 노년층에서 발병률이 증가함에 따라 효과적인 치료제에 대한 수요가 계속 증가하고 있습니다. 신흥국에서는 의료 접근성이 향상되고 공중 보건 정책이 강화되며 질병에 대한 인식이 높아짐에 따라 치료법 채택률이 높아지고 있습니다. 의약품 개발자들은 피로, 수면 장애, 우울증과 같은 운동 및 비운동 증상을 모두 해결할 수 있는 새로운 제형에 집중하고 있습니다. 이러한 혁신은 파킨슨병 관리의 치료 격차를 해소하고 시장 잠재력을 더욱 증폭시키는 데 도움이 되고 있습니다.

미국의 도파민 작용제 시장은 탄탄한 의료 인프라와 전문 신경과 치료에 대한 광범위한 접근성을 바탕으로 2024년에 11억 달러에 달할 것으로 예상됩니다. 이 시장은 제약 연구의 지속적인 혁신과 의약품 승인을 가속화하는 지원적인 규제 환경의 혜택을 받고 있습니다. AI와 첨단 이미징 기술의 통합으로 조기 발견이 더욱 보편화되고 있으며, 인식 개선 캠페인을 통해 적극적인 신경과 검진을 장려하고 있습니다. 이러한 노력으로 전국적으로 환자들의 진단 시기가 빨라지고 임상 결과가 개선되고 있습니다.

Adamas Pharma, Sunovion Pharmaceuticals, Novartis, Teva Pharmaceutical Industries, Pfizer, AbbVie, UCB Pharma, Boehringer Ingelheim Pharmaceuticals, Avvisto Therapeutics(VeroScience), GlaxoSmithKline(GSK), Bertek Pharmaceuticals, Kirin Holdings 회사와 같은 주요 제약 회사는 경쟁 구도를 적극적으로 재구성하고 있습니다. 이러한 기업들은 최첨단 도파민 작용제 치료법, 약물 전달 메커니즘 개선, 고성장 지역에서의 입지 확대에 투자를 집중하고 있습니다. 생명공학 기업 및 학술 기관과의 전략적 파트너십은 R&D 파이프라인을 가속화하여 빠른 혁신을 가능하게 하고 글로벌 도파민 작용제 시장에서 장기적인 성공을 위한 입지를 다지고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향 요인

- 성장 촉진요인

- 파킨슨병 및 기타 신경질환의 유병률 증가

- 약물 개발 및 제형의 발전

- 신경질환에 대한 인식의 고조와 조기 진단

- 업계의 잠재적 위험 및 과제

- 규제상의 과제와 신약 승인 지연

- 대체 치료와의 경쟁

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장추계 및 예측 : 약제 유형별(2021-2034년)

- 주요 동향

- 에르고트계 도파민 작용제

- 비에르고트계 도파민 작용제

제6장 시장추계 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 파킨슨병

- 하지불안증후군(RLS)

- 고프로락틴혈증

- 기타 적응증

제7장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 경구

- 주사제

- 기타 투여 경로

제8장 시장추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 병원 약국

- 약국 및 소매 약국

- 온라인 약국

제9장 시장추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AbbVie

- Adamas Pharma

- Amneal Pharmaceuticals

- Avvisto Therapeutics(VeroScience)

- Boehringer Ingelheim Pharmaceuticals

- Bertek Pharmaceuticals(Mylan)

- GlaxoSmithKline(GSK)

- Kirin Holdings Company

- Novartis

- Pfizer

- Sunovion Pharmaceuticals

- Teva Pharmaceutical Industries

- UCB Pharma

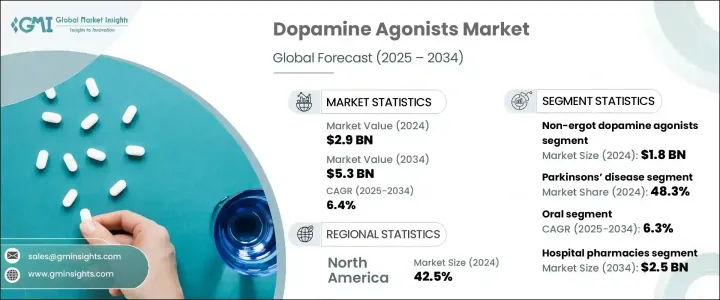

The Global Dopamine Agonists Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 5.3 billion by 2034. This steady growth reflects the increasing demand for advanced neurological therapies, driven by a global surge in neurodegenerative conditions like Parkinson's disease and restless legs syndrome (RLS). With neurological disorders becoming more common due to aging populations, sedentary lifestyles, and heightened stress levels, healthcare providers are placing greater emphasis on early detection and intervention.

As patients become more aware of available treatment options, diagnosis rates are rising, and patients are being placed on effective medication regimens sooner than before. In parallel, pharmaceutical innovation continues to drive the market forward. Companies are actively investing in next-generation dopamine agonists with superior efficacy and reduced side effects. Improvements in drug delivery systems, such as transdermal patches and extended-release tablets, are transforming treatment experiences and improving medication adherence. Across both developed and emerging economies, rising healthcare investments and technological advancements are reshaping the treatment landscape for neurological disorders, creating favorable conditions for sustained market growth in the dopamine agonists space.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 6.4% |

Non-ergot dopamine agonists generated USD 1.8 billion in 2024, establishing themselves as the dominant drug class in this therapeutic area. Clinicians now prefer these over traditional ergot-based options due to their safer profiles and significantly lower risk of cardiovascular and fibrotic complications. The convenience of once-daily dosing and the availability of user-friendly transdermal applications are also pushing more patients toward non-ergot alternatives. Pharmaceutical companies are focusing heavily on R&D to develop innovative compounds that offer better tolerability and long-term benefits. As these improved options become more widely available, physicians are increasingly recommending them as first-line therapies, which is boosting prescription volumes and improving patient outcomes across key markets.

The Parkinson's disease segment held a 48.3% share of the overall market in 2024, maintaining its position as the largest application area for dopamine agonists. Given that Parkinson's is the second most prevalent neurodegenerative disorder worldwide, its rising incidence-especially among the elderly-continues to drive significant demand for effective treatments. In emerging countries, enhanced access to medical care, stronger public health policies, and increased disease awareness are contributing to higher treatment adoption. Drug developers are focusing on novel formulations that address both motor and non-motor symptoms, such as fatigue, sleep disturbances, and depression. These innovations are helping bridge therapeutic gaps in Parkinson's management, further amplifying market potential.

The U.S. Dopamine Agonists Market reached USD 1.1 billion in 2024, underpinned by robust healthcare infrastructure and widespread access to specialized neurology care. The market benefits from continuous innovation in pharmaceutical research and a supportive regulatory environment that accelerates drug approvals. The integration of AI and advanced imaging technologies is making early detection more common, while awareness campaigns encourage proactive neurological screenings. These efforts are driving more timely diagnoses and better clinical outcomes for patients nationwide.

Top pharmaceutical players, including Adamas Pharma, Sunovion Pharmaceuticals, Novartis, Teva Pharmaceutical Industries, Pfizer, AbbVie, UCB Pharma, Boehringer Ingelheim Pharmaceuticals, Avvisto Therapeutics (VeroScience), GlaxoSmithKline (GSK), Bertek Pharmaceuticals (Mylan), Amneal Pharmaceuticals, and Kirin Holdings Company, are actively reshaping the competitive landscape. These companies are channeling investments into cutting-edge dopamine agonist therapies, improving drug delivery mechanisms, and expanding their presence in high-growth regions. Strategic partnerships with biotech firms and academic institutions are accelerating R&D pipelines, enabling rapid innovation and positioning these players for long-term success in the global dopamine agonists market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of parkinson’s disease and other neurological disorders

- 3.2.1.2 Advancements in drug development and formulations

- 3.2.1.3 Growing awareness and early diagnosis of neurological disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory challenges and delay in approvals of new drugs

- 3.2.2.2 Competition from alternative therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Ergot dopamine agonists

- 5.3 Non-ergot dopamine agonists

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Parkinson’s disease

- 6.3 Restless legs syndrome (RLS)

- 6.4 Hyperprolactinemia

- 6.5 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectables

- 7.4 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Drug store and retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Adamas Pharma

- 10.3 Amneal Pharmaceuticals

- 10.4 Avvisto Therapeutics (VeroScience)

- 10.5 Boehringer Ingelheim Pharmaceuticals

- 10.6 Bertek Pharmaceuticals (Mylan)

- 10.7 GlaxoSmithKline (GSK)

- 10.8 Kirin Holdings Company

- 10.9 Novartis

- 10.10 Pfizer

- 10.11 Sunovion Pharmaceuticals

- 10.12 Teva Pharmaceutical Industries

- 10.13 UCB Pharma