|

시장보고서

상품코드

1721423

저분자 API 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Small Molecule API Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

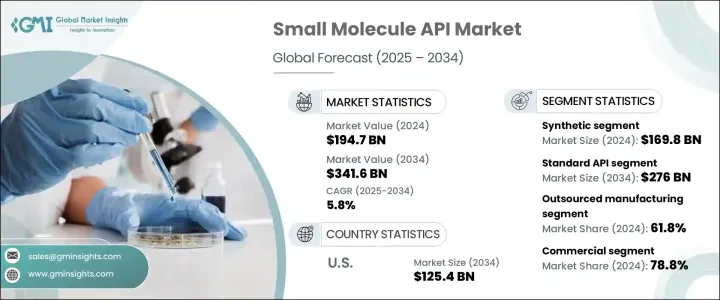

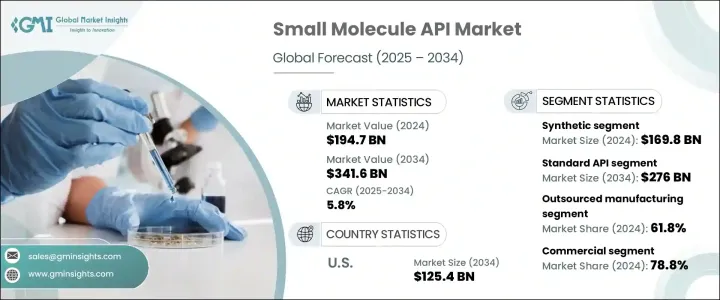

세계의 저분자 API 시장은 2024년 1,947억 달러로 평가되었고, 2034년에는 3,416억 달러에 이를 것으로 추정되며, CAGR 5.8%로 성장할 전망입니다. 저분자 활성 제약 성분(API)은 제형의 용이성, 경구 생체 이용률, 잘 정립된 제조 공정으로 인해 현대 치료법에서 계속해서 중추적인 역할을 담당하고 있습니다. 분자량이 낮은 것이 특징인 이러한 화합물은 세포막을 쉽게 투과하여 다양한 질병에 걸쳐 치료 효과를 제공합니다. 제약 업계가 정밀 의료와 신속한 신약 개발에 집중하면서 저분자 API에 대한 관심이 다시 높아지고 있습니다. 제약 회사들은 점점 더 인공지능과 고처리량 스크리닝 도구를 활용하여 신약 발견 및 개발 프로세스를 최적화하고 있습니다. 이러한 혁신은 신약 개발 일정을 단축하고, 표적화 효율성을 개선하며, 생산 비용을 크게 절감했습니다. 또한 만성 질환의 유병률 증가, 인구 고령화, 비용 효율적인 의약품에 대한 수요 증가와 같은 글로벌 의료 트렌드로 인해 제약 회사들은 API 생산 규모를 확대하고 있습니다. 주요 시장의 정부도 제네릭 의약품의 공급을 적극적으로 장려하여 API 제조에 우호적인 생태계를 조성하고 있습니다.

시장은 유형별로 바이오테크 및 합성 API로 분류되며, 합성 부문은 2024년에 1,698억 달러의 가치를 창출했습니다. 합성 API는 확장성, 경제성 및 광범위한 치료 응용 분야로 인해 시장을 지배하고 있습니다. 화학 합성을 통해 생산되는 이러한 API는 일관된 품질과 안정성을 제공하므로 대량 생산 시 신뢰성이 높습니다. 감염, 심혈관 질환, 대사 질환 등의 치료 분야에서 강력한 입지를 구축한 덕분에 글로벌 의약품 제형의 중추로 자리 잡았습니다. 의료 시스템이 더 낮은 비용으로 효과적인 솔루션을 제공해야 한다는 압박을 받고 있는 상황에서 합성 API는 품질이나 효능을 저하시키지 않으면서도 대량 생산을 보장함으로써 이러한 과제를 해결하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1,947억 달러 |

| 예측 금액 | 3,416억 달러 |

| CAGR | 5.8% |

효능을 바탕으로 저분자 API 시장은 표준 API와 고효능 API(HPAPI)로 나뉩니다. 표준 API 부문은 2024년 81.4%의 시장 점유율을 차지했으며 2034년에는 2760억 달러에 달할 것으로 예상됩니다. 이러한 API는 전 세계 의약품 소비의 상당 부분을 차지하는 제네릭 의약품을 제조하는 데 매우 중요합니다. 통증 관리부터 만성 질환 치료에 이르기까지 다양한 치료 범주에 걸쳐 비용 효율성과 적응성을 갖추고 있어 제약 회사는 폭넓고 수익성 있는 제품 파이프라인을 유지할 수 있습니다. 표준 API는 경제성과 치료의 다양성을 제공함으로써 전 세계 인구가 필수 의약품에 일관되게 접근할 수 있도록 보장합니다.

미국의 저분자 API 시장은 2034년까지 1,254억 달러에 이를 것으로 예측되고 있습니다. 미국은 선진 제약 생태계, 탄탄한 제네릭 의약품 제조업체 네트워크, 신속한 의약품 승인을 지원하는 규제 프레임워크의 혜택을 누리고 있습니다. 의료 인프라에 대한 지속적인 투자, 만성 질환 치료제에 대한 수요 증가, 저렴한 의약품 접근성을 위한 정책적 지원 등이 시장 성장을 촉진하고 있습니다.

Bristol-Myers, Johnson Matthey, AstraZeneca, Novartis, GILEAD Sciences, Merck, Boehringer Ingelheim, Hoffmann-La Roche, Teva Pharmaceuticals, GlaxoSmithKline, Curia Global, BASF, Pfizer, EUROAPI 및 Nanjing King-Friend Biochemical Pharmaceutical 등의 주요 기업은 R&D 확장, 첨단 합성 기술, AI 기반 신약 개발에 우선순위를 두고 있다. 많은 기업이 운영 규모를 확장하고 치료제를 확대하기 위해 라이선스 계약, 인수, 제조 확장을 추진하고 있습니다. 기업들이 글로벌 공급망을 강화하고 증가하는 수요를 충족하기 위해 노력함에 따라 규제 준수와 지속가능성 또한 가장 중요한 이슈로 떠오르고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성질환의 유병률 증가

- 의약품 개발 기술의 발전

- 제네릭 의약품과 바이오시밀러 시장 확대

- 업계의 잠재적 위험 및 과제

- 높은 제조 비용

- 엄격한 규제 시나리오

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 합성

- 바이오테크

제6장 시장추계 및 예측 : 효력별(2021-2034년)

- 주요 동향

- 표준 API

- 고효능 API(HPAPI)

제7장 시장추계 및 예측 : 제조 업종별(2021-2034년)

- 주요 동향

- 사내

- 아웃소싱

제8장 시장추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 임상용

- 상업용

제9장 시장추계 및 예측 : 치료 영역별(2021-2034년)

- 주요 동향

- 심혈관계

- 종양학

- 중추신경계 및 신경학

- 정형외과

- 내분비학

- 호흡기과

- 소화기내과

- 신장학

- 안과

- 기타 치료 영역

제10장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 제약 회사

- 생명 공학 기업

- 계약 개발 제조 조직(CDMO)

- 기타 최종 사용자

제11장 시장추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제12장 기업 프로파일

- AstraZeneca

- BASF

- Boehringer Ingelheim

- Bristol-Myers

- Curia Global

- EUROAPI

- GILEAD Sciences

- GlaxoSmithKline

- Hoffmann-La Roche

- Johnson Matthey

- Merck

- Nanjing King-Friend Biochemical Pharmaceutical

- Novartis

- Pfizer

- Teva Pharmaceuticals

The Global Small Molecule API Market was valued at USD 194.7 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 341.6 billion by 2034. Small molecule active pharmaceutical ingredients (APIs) continue to play a pivotal role in modern therapeutics due to their ease of formulation, oral bioavailability, and well-established manufacturing processes. These compounds, characterized by low molecular weight, easily penetrate cell membranes to deliver therapeutic benefits across a wide range of diseases. As the pharmaceutical industry intensifies its focus on precision medicine and rapid drug development, small molecule APIs are witnessing renewed interest. Pharmaceutical companies are increasingly leveraging artificial intelligence and high-throughput screening tools to optimize discovery and development processes. These innovations have shortened drug development timelines, improved targeting efficiency, and significantly reduced production costs. Additionally, global healthcare trends such as the increasing prevalence of chronic diseases, aging populations, and rising demand for cost-effective drugs are pushing pharmaceutical firms to scale up API production. Governments across key markets are also actively promoting generic drug availability, creating a favorable ecosystem for API manufacturing. The need for affordable, scalable, and effective treatments is further driving API manufacturers to invest in robust infrastructure, regulatory compliance, and R&D innovation.

The market is segmented by type into biotech and synthetic APIs, with the synthetic category generating USD 169.8 billion in 2024. Synthetic APIs dominate the landscape due to their scalability, affordability, and broad-spectrum therapeutic applications. Produced through chemical synthesis, these APIs offer consistent quality and stability, making them highly reliable during mass production. Their strong foothold in treatments for infections, cardiovascular diseases, metabolic conditions, and more has positioned them as the backbone of global pharmaceutical formulations. With healthcare systems under pressure to deliver effective solutions at lower costs, synthetic APIs are meeting the challenge by ensuring large-scale production without compromising on quality or efficacy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $194.7 Billion |

| Forecast Value | $341.6 Billion |

| CAGR | 5.8% |

Based on potency, the small molecule API market is divided into standard APIs and high potency APIs (HPAPIs). The standard API segment held an 81.4% market share in 2024 and is forecasted to reach USD 276 billion by 2034. These APIs are crucial for manufacturing generic medications, which account for a significant portion of global drug consumption. Their cost-effective nature and adaptability across various therapeutic categories-from pain management to chronic disease treatment-allow pharmaceutical companies to maintain broad, profitable product pipelines. By delivering affordability and therapeutic versatility, standard APIs are ensuring consistent access to essential medications for global populations.

The U.S. Small Molecule API Market is projected to reach USD 125.4 billion by 2034. The country benefits from an advanced pharmaceutical ecosystem, a robust network of generic drug manufacturers, and a regulatory framework that supports accelerated drug approvals. Ongoing investments in healthcare infrastructure, rising demand for chronic illness treatments, and policy support for affordable medication access are propelling market growth.

Leading companies such as Bristol-Myers, Johnson Matthey, AstraZeneca, Novartis, GILEAD Sciences, Merck, Boehringer Ingelheim, Hoffmann-La Roche, Teva Pharmaceuticals, GlaxoSmithKline, Curia Global, BASF, Pfizer, EUROAPI, and Nanjing King-Friend Biochemical Pharmaceutical are prioritizing R&D expansion, advanced synthesis technologies, and AI-powered drug development. Many are pursuing licensing deals, acquisitions, and manufacturing expansions to scale operations and broaden therapeutic offerings. Regulatory compliance and sustainability are also at the forefront as companies strive to enhance global supply chains and meet escalating demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Advancements in drug development technologies

- 3.2.1.3 Expanding generic and biosimilar market

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs

- 3.2.2.2 Stringent regulatory scenario

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Synthetic

- 5.3 Biotech

Chapter 6 Market Estimates and Forecast, By Potency, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Standard API

- 6.3 HPAPI

Chapter 7 Market Estimates and Forecast, By Manufacturing Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 In-house

- 7.3 Outsourced

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Clinical

- 8.3 Commercial

Chapter 9 Market Estimates and Forecast, By Therapeutic Area, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Cardiovascular

- 9.3 Oncology

- 9.4 CNS and Neurology

- 9.5 Orthopedic

- 9.6 Endocrinology

- 9.7 Pulmonology

- 9.8 Gastroenterology

- 9.9 Nephrology

- 9.10 Ophthalmology

- 9.11 Other therapeutic areas

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Pharmaceutical companies

- 10.3 Biotechnology companies

- 10.4 Contract development and manufacturing organizations (CDMOs)

- 10.5 Other end users

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AstraZeneca

- 12.2 BASF

- 12.3 Boehringer Ingelheim

- 12.4 Bristol-Myers

- 12.5 Curia Global

- 12.6 EUROAPI

- 12.7 GILEAD Sciences

- 12.8 GlaxoSmithKline

- 12.9 Hoffmann-La Roche

- 12.10 Johnson Matthey

- 12.11 Merck

- 12.12 Nanjing King-Friend Biochemical Pharmaceutical

- 12.13 Novartis

- 12.14 Pfizer

- 12.15 Teva Pharmaceuticals