|

시장보고서

상품코드

1721441

수의 심장학 시장 기회 및 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Veterinary Cardiology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

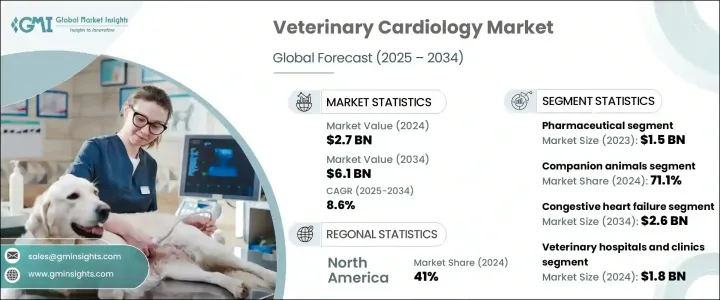

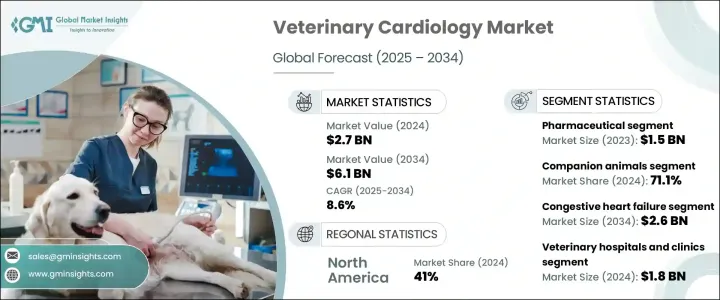

세계의 수의 심장학 시장은 2024년 27억 달러로 평가되었고, 2034년에는 61억 달러에 달할 것으로 추정되며, CAGR 8.6%로 성장할 전망입니다. 반려동물 소유의 증가와 동물 건강에 대한 높아진 인식이 이러한 시장 확대에 중추적인 역할을 하고 있습니다. 반려동물이 점점 더 필수적인 가족 구성원이 되면서 보호자들은 심혈관 질환을 비롯한 만성 질환에 대해 적시에 전문적인 치료를 받는 데 더욱 적극적으로 나서고 있습니다. 수의사들은 특히 노령화된 개와 고양이의 심장 관련 사례가 눈에 띄게 급증하는 것을 목격하면서 심장학 서비스에 대한 투자를 늘리고 있습니다.

또한 반려동물 보험의 보장 범위가 고급 진단 검사 및 치료를 포함하도록 점차 확대되고 있어 보호자들이 전문 치료를 선택하도록 장려하고 있습니다. 또한 수의학 전문의의 증가, 동물 의료 인프라의 확대, 반려동물의 심장학 치료 결과를 개선하기 위한 R&D 투자 증가로 시장이 탄력을 받고 있습니다. 수의학과 기술의 융합으로 업계는 동물의 심장 질환을 진단, 모니터링 및 치료하는 방법을 재정의하는 빠른 변화를 겪고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 27억 달러 |

| 예측 금액 | 61억 달러 |

| CAGR | 8.6% |

이러한 성장은 심장병을 앓는 반려동물의 수가 증가하고 진단 및 치료 방법이 발전함에 따라 이루어지고 있습니다.

시장은 의약품과 진단제로 나뉩니다. 의약품 부문은 2023년에 15억 달러의 수익을 창출했습니다. 이 주목할 만한 성과는 주로 치료 프로토콜의 지속적인 혁신과 노령 반려동물의 심혈관 질환 발병률 증가에 기인합니다. 동물의 심장 기능을 조절하고 체액 축적을 관리하며 혈압을 조절할 수 있는 약물에 대한 수요가 증가함에 따라 이 분야에 대한 투자와 제품 개발이 증가하고 있습니다.

수의 심장학 시장의 반려동물 부문은 71.1%의 점유율을 차지할 것으로 예상됩니다. 개, 고양이 및 기타 반려동물을 포함하는 이 카테고리는 입양률이 증가하고 반려동물이 나이가 들어감에 따라 심장 질환이 발생할 가능성이 높아짐에 따라 계속 우위를 점하고 있습니다. 오늘날 반려동물 보호자들은 질병의 조기 발견에 대한 의식이 높아지면서 전문 심장학 서비스를 추구하고 있습니다. 심초음파 및 심전도(ECG)와 같은 고급 진단에 대한 수요가 증가하고 있습니다.

북미의 수의 심장학 2024년에 41%의 점유율을 차지할 것으로 예상됩니다. 이 지역의 지배력은 많은 반려동물 인구, 진단 도구의 발전, 전문 동물 병원의 확장에 의해 뒷받침됩니다. 특히 미국 시장은 인공지능과 웨어러블 심장 모니터의 통합이 증가하면서 반려동물의 심장 건강을 모니터링하는 방식이 변화하고 있습니다.

수의 심장학 주요 기업으로는 TriviumVet, ESAOTE, Bionet America, Medtronic, Jurox, Siemens Healthineers, Fujifilm, Zoetis, Antech Diagnostics, General Electric Company, IDEXX, Merck, Boehringer Ingelheim International, Ceva, GSK 등이 있습니다. 기업들은 심초음파 및 카테터 기반 치료법과 같은 첨단 진단 도구를 도입하는 등 혁신적인 제품 개발에 주력하고 있습니다. 동물 병원, 연구 기관, 기술 기업과의 전략적 협업을 통해 글로벌 시장에서 영향력을 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 반려동물 입양 증가 및 동물 건강 관리에 대한 지출 증가

- 수의 심장학 진단 및 치료 기술의 발전

- 반려 동물의 심혈관 질환 유병률 증가

- 업계의 잠재적 위험 및 과제

- 고급 수의 심장학 치료 및 장치의 높은 비용

- 전문 수의학 심장 전문의의 제한된 가용성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 의약품

- 피모벤단

- 스피로노락톤과 염산베나제프릴

- 기타 의약품

- 진단제

- 신체 검사

- 흉부 X선 검사

- 심전도(ECG)

- 기타 진단

제6장 시장추계 및 예측 : 동물 유형별(2021-2034년)

- 주요 동향

- 반려동물

- 개

- 고양이

- 기타 반려동물

- 가축

- 소

- 가금

- 기타 가축

제7장 시장추계 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 울혈성 심부전

- 심근 질환

- 부정맥

- 기타 적응증

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 동물병원 및 진료소

- 학술 연구기관

- 기타 최종 사용자

제9장 시장추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Antech Diagnostics

- Boehringer Ingelheim International

- Jurox

- Ceva

- Merck

- IDEXX

- General Electric Company

- FUJIFILM

- ESAOTE

- Medtronic

- Siemens Healthineers

- TriviumVet

- Zoetis

- Bionet America

The Global Veterinary Cardiology Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 6.1 billion by 2034. The rise in pet ownership and heightened awareness of animal health are playing a pivotal role in this expansion. As pets increasingly become integral family members, owners are more proactive in seeking timely and specialized care for chronic conditions, including cardiovascular diseases. Veterinarians are witnessing a notable surge in heart-related cases, especially among aging dogs and cats, prompting increased investments in cardiology services.

Moreover, pet insurance coverage is gradually expanding to include advanced diagnostic tests and treatments, which is further encouraging owners to opt for specialized care. The market is also gaining momentum with the growing presence of veterinary specialists, expanding infrastructure in animal healthcare, and rising R&D investments aimed at improving cardiology outcomes in companion animals. With the convergence of veterinary medicine and technology, the industry is undergoing a rapid transformation that is redefining how heart conditions in animals are diagnosed, monitored, and treated.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 8.6% |

This growth is driven by a rising number of pets with heart disease and advancements in diagnostic and treatment methods. Minimally invasive procedures, such as balloon valvuloplasty and pacemaker implantation, are gaining popularity due to reduced risks and quicker recovery times. Newer medications like pimobendan, ACE inhibitors, and beta-blockers are also helping extend the lifespan of pets diagnosed with heart conditions.

The market is divided into pharmaceuticals and diagnostics. The pharmaceuticals segment generated USD 1.5 billion in 2023. This notable performance is mainly attributed to ongoing innovation in treatment protocols and a growing incidence of cardiovascular conditions in senior pets. There is a rising demand for medications that can regulate heart function, manage fluid buildup, and control blood pressure in animals, leading to increased investments and product development in this space.

The companion animal segment in the veterinary cardiology market held a 71.1% share in 2024. This category, which includes dogs, cats, and other domestic pets, continues to dominate due to increasing adoption rates and the higher likelihood of pets developing heart issues as they age. Pet owners today are far more conscious about the early detection of diseases, prompting them to pursue specialized cardiology services. Advanced diagnostics such as echocardiograms and electrocardiograms (ECGs) are seeing growing demand.

North America Veterinary Cardiology Market held a 41% share in 2024. The region's dominance is supported by a large population of companion animals, advancements in diagnostic tools, and the expansion of specialty veterinary hospitals. The U.S. market, in particular, is seeing growing integration of artificial intelligence and wearable heart monitors, which are changing how cardiac health is monitored in pets.

Major players involved in the veterinary cardiology market include TriviumVet, ESAOTE, Bionet America, Medtronic, Jurox, Siemens Healthineers, Fujifilm, Zoetis, Antech Diagnostics, General Electric Company, IDEXX, Merck, Boehringer Ingelheim International, Ceva, and GSK among others. Companies are focusing on innovative product development, introducing advanced diagnostic tools like echocardiograms and catheter-based therapies. Strategic collaborations with veterinary clinics, research bodies, and tech firms are helping them expand their reach and influence across global markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet adoption and increasing expenditure on animal healthcare

- 3.2.1.2 Advancements in veterinary cardiology diagnostics and treatment technologies

- 3.2.1.3 Increasing prevalence of cardiovascular diseases in companion animals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced veterinary cardiology treatments and devices

- 3.2.2.2 Limited availability of specialized veterinary cardiologists

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmaceuticals

- 5.2.1 Pimobendan

- 5.2.2 Spironolactone and benazepril hydrochloride

- 5.2.3 Other pharmaceuticals

- 5.3 Diagnostics

- 5.3.1 Physical exam

- 5.3.2 Chest X-rays

- 5.3.3 Electrocardiogram (ECG)

- 5.3.4 Other diagnostics

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Companion animals

- 6.2.1 Dogs

- 6.2.2 Cats

- 6.2.3 Other companion animals

- 6.3 Livestock animals

- 6.3.1 Cattle

- 6.3.2 Poultry

- 6.3.3 Other livestock animals

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Congestive heart failure

- 7.3 Myocardial (heart muscle) disease

- 7.4 Arrhythmias

- 7.5 Other indications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 Academic and research institutions

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Antech Diagnostics

- 10.2 Boehringer Ingelheim International

- 10.3 Jurox

- 10.4 Ceva

- 10.5 Merck

- 10.6 IDEXX

- 10.7 General Electric Company

- 10.8 FUJIFILM

- 10.9 ESAOTE

- 10.10 Medtronic

- 10.11 Siemens Healthineers

- 10.12 TriviumVet

- 10.13 Zoetis

- 10.14 Bionet America