|

시장보고서

상품코드

1721457

혈장 프로테아제 C1 억제제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Plasma Protease C1-inhibitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

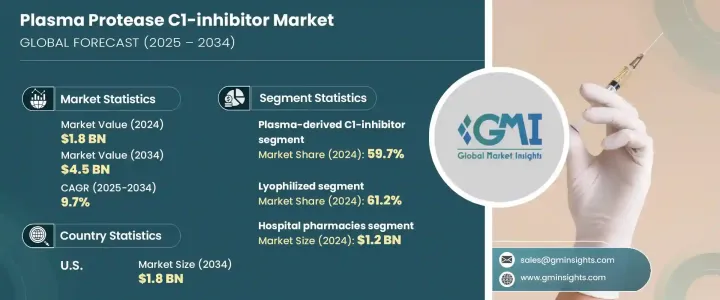

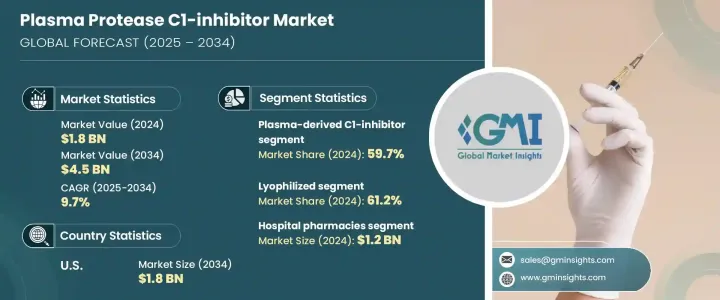

세계의 혈장 프로테아제 C1 억제제 시장은 2024년 18억 달러로 평가되었으며 CAGR 9.7%를 나타내 2034년에는 45억 달러에 이를 것으로 추정되고 있습니다. 성부종(HAE)과 같은 드문 유전성 질환의 치료에 있어 매우 중요합니다.

혈장 분획 및 채취 방법의 기술적 진보는 혈장 유래의 치료제의 수율과 순도를 높임으로써 생물학적 제제의 상황을 재구성하고 있습니다. 임상적 관심의 고조와 맞춤형 의료의 대두에 의해 시장은 염증성 질환이나 자가면역 질환 등의 새로운 치료 응용 분야에의 침투가 진행될 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 18억 달러 |

| 예측 금액 | 45억 달러 |

| CAGR | 9.7% |

약제 클래스별로는 혈장 유래의 C1 억제제 부문이 시장을 독점해, 2024년의 세계 점유율의 59.7%를 차지했습니다. 그런데 시장 내에서는 소규모 부문에 머물러 있습니다.혈장 유래의 제형은 그 확립된 안전성 프로파일과 HAE의 급성 치료 및 예방 치료에 있어서 입증된 효능에 의해 여전히 바람직한 옵션입니다.

제형을 보면 동결건조 C1 억제제가 2024년 점유율 61.2%로 계속 시장을 선도했습니다. 콜드체인 인프라에 대한 액세스가 제한된 지역에서 사용하기에 이상적입니다.

미국 시장은 강력한 성장을 이루고 있습니다. 개선, 조기 진단에 대한 의식이 높아지고, 희귀질환 치료에 대한 폭넓은 접근이 있습니다.

이 시장 주요 기업으로는 BioCryst Pharmaceuticals, 다케다 약품 공업, KalVista, Ionis Pharmaceuticals, CSL Behring, Fresenius Kabi, Pharming, Pharvaris, Astria 등이 있습니다. 이러한 기업은 특히 면역학과 염증 분야에서 C1 억제제의 새로운 적응증을 발견하기 위해 연구 개발에 많은 투자를 실시했습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 유전성 혈관부종(HAE) 및 보체 시스템 장애의 유병률 증가

- 바이오테크놀러지와 의약품 개발의 진보

- 유리한 정부규제와 상환정책

- 희소질환의 연구개발 투자 증가

- 업계의 잠재적 위험 및 과제

- C1 억제제 치료의 높은 비용

- 공급 부족과 공급 체인의 제약

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 갭 분석

- 특허 분석

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 약제 클래스별(2021-2034년)

- 주요 동향

- 혈장 유래 C1 억제제

- 선택적 브라디키닌 B2 수용체 길항제

- 칼리크레인 억제제

제6장 시장 추계·예측 : 제형별(2021-2034년)

- 주요 동향

- 동결 건조

- 주사제

제7장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 병원 약국

- 소매 약국

- 전자상거래

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Astria

- BioCryst Pharmaceuticals

- CSL Behring

- Fresenius Kabi

- Ionis Pharmaceuticals

- KalVista

- Pharming

- Pharvaris

- Takeda Pharmaceutical Company

The Global Plasma Protease C1-Inhibitor Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 4.5 billion by 2034. Plasma protease C1-inhibitors serve a vital role in controlling the activation of the complement and contact systems within the human body. These proteins, derived from blood plasma, are crucial in the treatment of rare genetic disorders such as Hereditary Angioedema (HAE). As healthcare systems continue to evolve, there is increasing awareness surrounding rare disease management, which is significantly contributing to the demand for effective and specialized therapies like C1-inhibitors.

Technological progress in plasma fractionation and collection methods is reshaping the landscape of biologics by enhancing the yield and purity of plasma-derived therapies. In turn, these developments are making treatments more accessible, affordable, and scalable for healthcare providers and patients alike. With growing clinical interest and the emergence of personalized medicine, the market is poised to witness greater penetration across new therapeutic applications, such as inflammatory and autoimmune diseases. Regulatory support and increasing healthcare infrastructure in both developed and emerging economies are further bolstering market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 9.7% |

In terms of drug classes, the plasma-derived C1-inhibitor segment dominated the market, accounting for 59.7% of the global share in 2024. While alternative options like selective bradykinin B2 receptor antagonists and Kallikrein inhibitors are also available, they currently serve as smaller segments within the market. Plasma-derived formulations remain the preferred option due to their established safety profiles and proven efficacy in managing acute and prophylactic treatment for HAE.

When looking at dosage forms, lyophilized C1-inhibitors continue to lead the market with a 61.2% share in 2024. These freeze-dried formulations are favored for their extended shelf life and do not require refrigeration, making them ideal for use in regions with limited access to reliable cold chain infrastructure. This advantage is particularly critical in rural healthcare settings and low-to-middle-income countries where consistent storage conditions can be a challenge.

The U.S. Plasma Protease C1-Inhibitor Market is experiencing robust growth. Valued at USD 729.4 million in 2024, it is projected to reach USD 1.8 billion by 2034. The expansion is driven by the rising prevalence of HAE, improvements in genetic screening, increased awareness of early diagnosis, and broader access to rare disease treatments. The U.S. FDA's continued support for orphan drugs, particularly for conditions like HAE, is accelerating product approvals and encouraging more innovation in this space.

Key players in the market include BioCryst Pharmaceuticals, Takeda Pharmaceutical Company, KalVista, Ionis Pharmaceuticals, CSL Behring, Fresenius Kabi, Pharming, Pharvaris, and Astria. These companies are heavily investing in R&D to discover new indications for C1-inhibitors, especially in the fields of immunology and inflammation. Strategic collaborations are also fueling growth by expanding product pipelines and fast-tracking next-generation therapies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of hereditary angioedema (HAE) and complement system disorders

- 3.2.1.2 Advancements in biotechnology and drug development

- 3.2.1.3 Favorable government regulations and reimbursement policies

- 3.2.1.4 Growing investment in rare disease research and development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of C1-inhibitor therapies

- 3.2.2.2 Limited availability and supply chain constraints

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Pipeline analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Plasma-derived C1-inhibitor

- 5.3 Selective bradykinin B2 receptor antagonist

- 5.4 Kallikrein inhibitor

Chapter 6 Market Estimates and Forecast, By Dosage Form, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Lyophilized

- 6.3 Injectables

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 E-commerce

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Astria

- 9.2 BioCryst Pharmaceuticals

- 9.3 CSL Behring

- 9.4 Fresenius Kabi

- 9.5 Ionis Pharmaceuticals

- 9.6 KalVista

- 9.7 Pharming

- 9.8 Pharvaris

- 9.9 Takeda Pharmaceutical Company