|

시장보고서

상품코드

1721474

침윤성 유관암 치료 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Invasive Ductal Carcinoma (IDC) Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

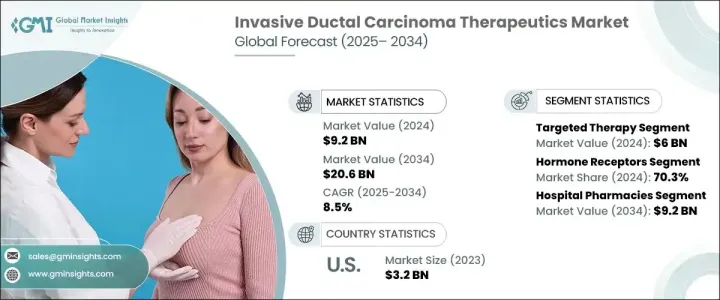

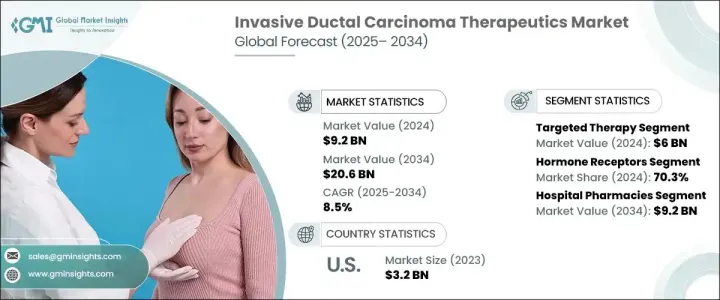

침윤성 유관암 치료 시장은 2024년에는 92억 달러로 평가되었고 CAGR 8.5%를 나타내 2034년에는 206억 달러에 이를 것으로 예측되고 있습니다. 침윤성 유관암은 침윤성 유방암 증례 전체의 80% 가까이를 차지하고 있으며, 종양학에서 중요한 영역이 되고 있습니다. 그 결과 생존율을 향상시킬 뿐만 아니라 삶의 질을 높이는 효과적이고 환자 중심의 치료에 대한 수요가 계속 증가하고 있습니다. 이 분야는 첨단 솔루션으로 그 필요를 충족시키기 위해 급속히 진화하고 있습니다.

기존의 화학요법이 IDC를 관리하는 데 중요한 요소라는 점은 변함이 없지만 혁신적인 표적 치료로의 전환이 가속화되고 있습니다. 감소로 인해 선호되는 치료 옵션이 되고 있습니다. 이 치료는 환자가 더 적은 부작용으로 더 나은 질병 통제를 달성하는 데 도움이되고 의사와 환자 모두가 이러한 선진적 접근에 기울이도록 촉구하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 92억 달러 |

| 예측 금액 | 206억 달러 |

| CAGR | 8.5% |

침윤성 유관암 치료 시장은 최종 용도별로 병원, 종양 클리닉, 기타 의료시설로 구분됩니다. 병원은 통합 암 치료, 최첨단 진단 시스템, 다학제 종양학 팀에 대한 접근성 덕분에 2034년까지 36억 달러의 수익을 창출할 것으로 예상됩니다. 이러한 환경은 화학요법, 면역요법, 정밀의료를 포함한 복잡한 치료요법의 종합적 관리를 지원하며 IDC치료의 유력한 선택이 되고 있습니다.

북미에서는 미국이 침윤성 유관암 치료 시장에서 톱 점유율을 차지하고 있지만, 이것은 이 지역의 높은 질환 이환율과 강력한 헬스케어 체제에 지지되고 있습니다.

이 분야의 주요 기업은 AbbVie, AstraZeneca, Bristol-Myers Squibb, Celldex Therapeutics, Eli Lilly, F. Hoffmann-La Roche, Janssen Pharmaceuticals, Macrogenics, Merck, Novartis, Pfizer 등이 있습니다. 이 회사는 더 나은 임상 결과와 부작용이 적은 최첨단 면역 요법과 병용 요법을 도입하기 위해 연구 개발에 많은 투자를하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 유방암의 이환율과 인지도의 향상

- 진단 기술 향상

- 치료 옵션의 확대

- 업계의 잠재적 위험 및 과제

- 높은 치료비

- 특정 치료법에 대한 부작용과 내성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 약제 유형별(2021-2034년)

- 주요 동향

- 표적 치료

- 아베마시클립

- 아드-트라스투주맙 엠탄신

- 에베롤리무스

- 트라스투주맙

- 리보시클리브

- 팔보시클리브

- 펠츠주맙

- 올라파리브

- 기타 표적요법

- 호르몬 요법

- 선택적 에스트로겐 수용체 조절제(SERM)

- 아로마타제 억제제

- 선택적 에스트로겐 수용체 분해제(SERD)

- 화학 치료

- 면역 치료

제6장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 호르몬 수용체

- HER2+

- 삼중 음성 유방암(TNBC)

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 종양학 클리닉

- 기타 용도

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- AbbVie

- AstraZeneca

- Bristol-Myers Squibb Company

- Celldex Therapeutics

- Eli Lilly and Company

- F. Hoffmann-La Roche

- Gilead Sciences

- Janssen Pharmaceuticals

- Macrogenics

- Merck

- Novartis

- Pfizer

The Global Invasive Ductal Carcinoma Therapeutics Market was valued at USD 9.2 billion in 2024 and is projected to grow at a CAGR of 8.5% to reach USD 20.6 billion by 2034. This robust growth outlook is fueled by the consistently rising prevalence of breast cancer worldwide, with invasive ductal carcinoma being the most frequently diagnosed subtype. IDC accounts for nearly 80% of all invasive breast cancer cases, making it a significant area of focus in oncology. As breast cancer screening programs expand and early detection improves, healthcare providers are witnessing a notable increase in the number of IDC diagnoses. This, in turn, continues to drive demand for effective, patient-centric therapies that not only improve survival rates but also enhance the quality of life. The growing burden of cancer has accelerated the need for treatment innovation, and the IDC therapeutics space is rapidly evolving to meet that need with advanced solutions. Increasing awareness among patients and clinicians, favorable reimbursement scenarios, and expanding healthcare infrastructure across developed and emerging economies are also contributing to this market's sustained momentum.

While conventional chemotherapy remains a key component in managing IDC, the shift toward innovative and targeted therapies is gaining speed. Hormone-based therapies and biologics are becoming the preferred treatment options due to their enhanced efficacy and reduced toxicity profiles. Therapies such as aromatase inhibitors and selective estrogen receptor degraders (SERDs) are especially effective in hormone receptor-positive (HR+) IDC cases, which represent a significant portion of diagnoses. These treatments are helping patients achieve better disease control with fewer side effects, prompting both physicians and patients to lean toward such advanced approaches. As a result, targeted therapeutics are becoming an indispensable element in IDC care protocols, further reinforcing the market's upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.2 Billion |

| Forecast Value | $20.6 Billion |

| CAGR | 8.5% |

The IDC therapeutics market is segmented by end-use into hospitals, oncology clinics, and other healthcare facilities. Hospitals are expected to generate USD 3.6 billion by 2034, owing to their ability to provide integrated cancer care, state-of-the-art diagnostic systems, and access to multidisciplinary oncology teams. These environments support comprehensive management of complex treatment regimens involving chemotherapy, immunotherapy, and precision medicines, thereby remaining the go-to option for IDC treatment.

In North America, the U.S. holds a leading share of the invasive ductal carcinoma therapeutics market, backed by the region's high disease prevalence and strong healthcare framework. The presence of renowned cancer treatment centers and widespread access to novel therapeutics are driving the adoption of IDC treatments.

Leading companies in this space include AbbVie, AstraZeneca, Bristol-Myers Squibb, Celldex Therapeutics, Eli Lilly, F. Hoffmann-La Roche, Janssen Pharmaceuticals, Macrogenics, Merck, Novartis, and Pfizer. These players are investing heavily in R&D to introduce cutting-edge immunotherapies and combination therapies that deliver better clinical outcomes and fewer side effects.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence and awareness of breast cancer

- 3.2.1.2 Improved diagnostic technologies

- 3.2.1.3 Expanding therapeutic options

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Side effects and resistance to certain therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Targeted therapy

- 5.2.1 Abemaciclib

- 5.2.2 Ado-trastuzumab emtansine

- 5.2.3 Everolimus

- 5.2.4 Trastuzumab

- 5.2.5 Ribociclib

- 5.2.6 Palbociclib

- 5.2.7 Pertuzumab

- 5.2.8 Olaparib

- 5.2.9 Other targeted therapies

- 5.3 Hormone therapy

- 5.3.1 Selective estrogen receptor modulators (SERMs)

- 5.3.2 Aromatase inhibitors

- 5.3.3 Selective estrogen receptor degraders (SERDs)

- 5.4 Chemotherapy

- 5.5 Immunotherapy

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hormone receptor

- 6.3 HER2+

- 6.4 Triple-negative breast cancer (TNBC)

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Oncology clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 AstraZeneca

- 9.3 Bristol-Myers Squibb Company

- 9.4 Celldex Therapeutics

- 9.5 Eli Lilly and Company

- 9.6 F. Hoffmann-La Roche

- 9.7 Gilead Sciences

- 9.8 Janssen Pharmaceuticals

- 9.9 Macrogenics

- 9.10 Merck

- 9.11 Novartis

- 9.12 Pfizer