|

시장보고서

상품코드

1721499

정형외과용 수술 로봇 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Orthopedic Surgical Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

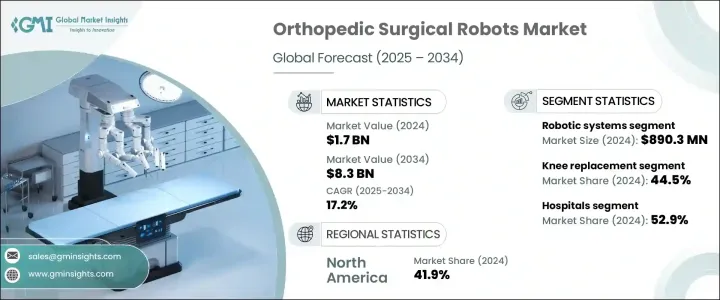

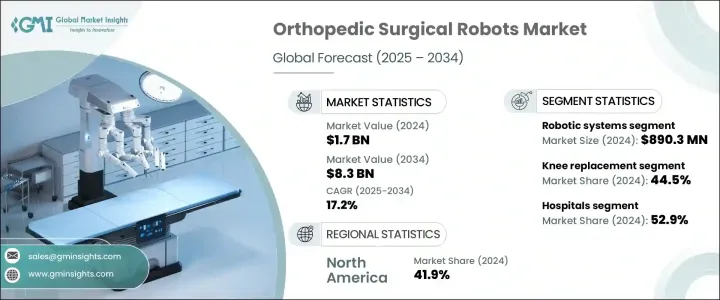

세계의 정형외과용 수술 로봇 시장 규모는 2024년에 17억 달러로 평가되었고, CAGR 17.2%를 나타내 2034년에는 83억 달러에 이를 것으로 예측되고 있습니다. 변형성 관절증, 인대 손상, 퇴행성 골질환, 골절 등의 정형외과 질환의 유병률이 세계적으로 상승을 계속하는 가운데, 외과적 개입을 로봇 플랫폼으로 실시하는 의료 시설이 증가하고 있습니다.

또한, 외과의사는 강화된 시각화 기능, 실시간 데이터 통합, 복잡한 수술 중 편의성 향상으로 로봇 시스템을 수용하고 있습니다. 로봇 공학이 AI와 머신러닝에 의해 진화함에 따라 이러한 시스템은 향후 10년간 정형외과 헬스케어에서 더 큰 역할을 할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 17억 달러 |

| 예측 금액 | 83억 달러 |

| CAGR | 17.2% |

구성 요소 분야에는 로봇 시스템, 액세서리, 소프트웨어, 서비스가 포함되어 있습니다. 로봇 플랫폼은 임플란트의 정렬을 개선하고 합병증의 위험을 줄이고 회복 시간을 단축하는 능력으로 병원과 전문 클리닉에서 선호되고 있습니다.

최종 용도별로는 병원 부문이 2024년에 52.9%의 점유율을 차지했습니다. 인적 실수를 줄이고 복잡한 사례를 더욱 효율적으로 관리하기 위해 로봇 시스템에 크게 의존하고 있습니다.

북미의 정형외과용 수술 로봇 시장은 2024년에 41.9%의 점유율을 차지했습니다. 외과 수술의 필요성이 증가함에 따라 변형성 관절증과 골다공증과 같은 관절 관련 질환이 계속 증가하고 있는 가운데 북미 병원과 수술센터는 차세대 로봇 시스템의 진료에 통합을 주도하고 있습니다.

세계의 정형외과용 수술 로봇 시장의 유력 기업은 Medtronic, Think Surgical, Globus Medical, Brainlab, Accuray, MicroPort Orthopedics, Intuitive, Johnson & Johnson, CUREXO, Smith & Nephew, Asen Biomet, Corin, Stryker, NUVASIVE 등이 있습니다. 이러한 기업은 연구 개발에 적극적으로 투자하고 수술 정밀도 향상, AI와 햅틱스의 통합, 다양한 임상 요구에 맞는 솔루션 개발에 종사하고 있으며, 대부분은 병원 및 유통업체와의 제휴를 통해 세계의 존재를 확대하는 한편, 유저의 도입과 퍼포먼스를 높이기 위해 견고한 판매 후 지원과 트레이닝을 제공합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 정형외과 질환 및 외상 증가

- 로봇 지원 수술 기술의 진보

- 저침습 수술(MIS) 수요 증가

- 고령화 인구 증가

- 업계의 잠재적 위험 및 과제

- 로봇 수술 시스템과 수술 절차의 높은 비용

- 한정 환불 정책

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 규제 상황

- 기술 환경

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 로봇 시스템

- 액세서리

- 소프트웨어 및 서비스

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 무릎 관절 치환술

- 고관절 치환술

- 어깨 관절 치환술

- 척추 수술

- 기타 용도

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 전문 정형외과 클리닉

- 기타 용도

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Accuray

- Asensus Surgical

- Brainlab

- Corin

- CUREXO

- Globus Medical

- Intuitive

- Johnson &Joshnson

- Medtronic

- MicroPort Orthopedics

- NUVASIVE

- Smith &Nephew

- Stryker

- Think Surgical

- Zimmer Biomet

The Global Orthopedic Surgical Robots Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 17.2% to reach USD 8.3 billion by 2034. The demand for advanced robotic-assisted surgical systems continues to surge as healthcare providers look for ways to increase procedural accuracy, minimize complications, and ensure quicker patient recovery. As the prevalence of orthopedic disorders-including osteoarthritis, ligament injuries, degenerative bone diseases, and fractures-continues to rise globally, more healthcare facilities are shifting toward robotic platforms for surgical interventions. Aging populations, growing awareness about minimally invasive surgeries, and the increasing volume of joint and spinal procedures are further accelerating this shift.

In addition, surgeons are embracing robotic systems due to their enhanced visualization capabilities, real-time data integration, and improved dexterity during complex procedures. With robotics transforming the way orthopedic surgeries are performed, more hospitals and surgical centers are investing in these systems to optimize patient care. The push for value-based care and favorable insurance coverage in several countries is also supporting this trend. As robotics evolve with AI and machine learning, these systems are expected to play an even bigger role in orthopedic healthcare over the coming decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 17.2% |

The component segment includes robotic systems, accessories, software, and services. The robotic systems segment generated USD 890.3 million in 2024. These systems are gaining traction because they offer surgeons greater control and precision in performing delicate orthopedic surgeries, particularly in spinal and joint procedures. Their ability to improve implant alignment, reduce the risk of complications, and shorten recovery time makes them a preferred choice across hospitals and specialty clinics. With features like 3D visualization, haptic feedback, and advanced imaging support, robotic platforms are transforming the surgical workflow and enhancing overall outcomes.

By end use, the hospitals segment held a 52.9% share in 2024. Hospitals continue to dominate the market due to their strong clinical infrastructure, a high influx of orthopedic cases, and a growing emphasis on technological upgrades. They rely heavily on robotic systems to improve procedural consistency, reduce human error, and manage complex cases with greater efficiency. The rising number of geriatric patients and favorable reimbursement policies are also making it easier for hospitals to adopt and scale robotic-assisted surgical solutions.

North America Orthopedic Surgical Robots Market held a 41.9% share in 2024. The region's dominance is driven by its robust healthcare infrastructure, rising adoption of AI-powered technologies, and an increasing need for precision-based, minimally invasive orthopedic procedures. As joint-related conditions like osteoarthritis and osteoporosis continue to rise, North American hospitals and surgical centers are leading the charge in integrating next-gen robotic systems into their practices.

Prominent companies in the Global Orthopedic Surgical Robots Market include Medtronic, Think Surgical, Globus Medical, Brainlab, Accuray, MicroPort Orthopedics, Intuitive, Johnson & Johnson, CUREXO, Smith & Nephew, Asensus Surgical, Zimmer Biomet, Corin, Stryker, and NUVASIVE. These players are actively investing in R&D to refine surgical accuracy, integrate AI and haptics, and develop tailored solutions for diverse clinical needs. Many are expanding their global presence through partnerships with hospitals and distributors, while offering robust post-sales support and training to enhance user adoption and performance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of orthopedic disorders and injuries

- 3.2.1.2 Advancements in robotic-assisted surgery technology

- 3.2.1.3 Increasing demand for minimally invasive surgeries (MIS)

- 3.2.1.4 Rising geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of robotic surgical systems and procedures

- 3.2.2.2 Limited reimbursement policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Robotic systems

- 5.3 Accessories

- 5.4 Software and services

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Knee replacement

- 6.3 Hip replacement

- 6.4 Shoulder replacement

- 6.5 Spinal surgeries

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers (ASCs)

- 7.4 Specialty orthopedic clinics

- 7.5 Other end uses

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accuray

- 9.2 Asensus Surgical

- 9.3 Brainlab

- 9.4 Corin

- 9.5 CUREXO

- 9.6 Globus Medical

- 9.7 Intuitive

- 9.8 Johnson & Joshnson

- 9.9 Medtronic

- 9.10 MicroPort Orthopedics

- 9.11 NUVASIVE

- 9.12 Smith & Nephew

- 9.13 Stryker

- 9.14 Think Surgical

- 9.15 Zimmer Biomet