|

시장보고서

상품코드

1721504

에어덕트 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Air Ducts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

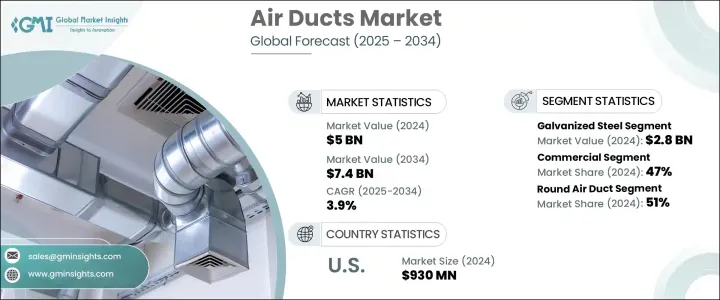

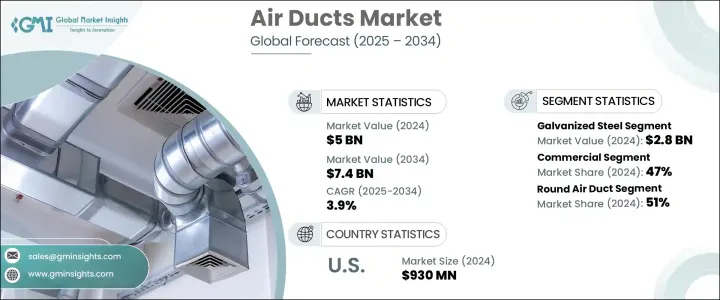

세계의 에어덕트 시장은 2024년에 50억 달러로 평가되었고 CAGR 3.9%를 나타내 2034년까지는 74억 달러에 이를 것으로 추정되고 있습니다.

이 성장의 주요 원동력은 세계 도시화의 급속한 페이스와 에너지 효율에 관한 엄격한 규제의 도입이 증가하고 있습니다. 실내 온도와 공기의 질을 유지하기 위해 에어 덕트에 크게 의존하고 있습니다.

HVAC 시스템은 현재 주로 열적 쾌적성과 에너지 효율을 확보하기 위해 새로운 건물의 핵심적인 기능이 되고 있습니다. 내구성이 높고 효율적인 에어덕트 시스템의 사용이 분명히 증가하고 있습니다. 오피스, 소매점, 교통기관, 복합시설 등, 사람의 출입이 많은 장소에서는 실내 공기의 질을 유지하는 것이 중요합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 50억 달러 |

| 예측 금액 | 74억 달러 |

| CAGR | 3.9% |

2024년에는 아연 도금 강판 에어덕트가 시장에서 가장 큰 점유율을 차지했으며, 28억 달러 이상의 수익을 올렸습니다. 으로 선호되는 선택입니다. 아연 도금 강철 덕트는 손질이 최소화되어 성능이 오래 지속되기 때문에 장기간에 걸쳐 비용 효과가 높습니다. 2025년부터 2034년까지의 CAGR은 약 3.6%를 나타낼 것으로 예상되고 있습니다. 설치가 쉽기 때문에 예산과 일정이 까다로운 프로젝트에 신뢰할 수 있는 솔루션을 제공합니다.

2024년 에어덕트 시장은 상업 부문이 세계 매출 점유율의 약 47%를 차지하고 압도적인 힘을 보였습니다. 관은 중요한 역할을 하며 현대적인 인테리어 디자인과 원활하게 융합되는 에어 덕트 수요를 밀어 올리고 있습니다.

형상별로는 원형의 에어덕트가 2024년 시장 전체의 51% 이상을 차지해, 선두에 섰습니다. 상업용 모두 이상적인 형상이 되고 있습니다. 또, 원형 덕트는 청소나 유지관리가 용이하고, 장기적인 신뢰성과 설치의 유연성이 뛰어납니다. 구조는 견고하고 표준화 된 건축 설계에 적합하기 때문에 대규모 상업 및 산업 프로젝트에 선호됩니다. 원형과 각형의 양쪽 모두의 특징을 아울러 타원 덕트의 인기도 높아지고 있습니다.

2024년 세계의 에어덕트 시장에서는 북미가 큰 점유율을 차지했으며 미국만으로 약 9억 3,000만 달러의 매출을 계상해 지역별 점유율의 80% 가까이를 차지했습니다. 건설 및 인프라 개발이 견조하게 늘어나고 있기 때문에 첨단 HVAC 설비, 특히 장기적인 지속가능성 목표를 지원하는 시스템에 대한 수요가 높아지고 있습니다. 또한, 스마트 HVAC 시스템의 채용이 증가하고 있기 때문에 접속 기술을 서포트하는 호환성이 있는 에어 덕트의 요구가 높아지고 있습니다.

업계의 주요 기업은 시장의 존재를 확대하고 진화하는 고객의 요구에 대응하기 위해 기술 업그레이드, 시설 확장, 전략적 파트너십에 투자하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴적 혁신

- 향후 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 도시화와 인프라 개발

- 에너지 효율 규제

- 기후 변화

- 업계의 잠재적 리스크 및 과제

- 높은 설치 및 유지 보수 비용

- 기존 구조물 개수의 복잡성

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계·예측 : 재료별(2021-2034년)

- 주요 동향

- 아연 도금 강철

- 알루미늄

- 유리 섬유

- 폴리머

- 기타

제6장 시장 추계·예측 : 형상별(2021-2034년)

- 주요 동향

- 직사각형

- 원형

- 타원형

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 주택용

- 상업용

- 산업용

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제9장 기업 프로파일

- DC Duct &Sheet Metal

- Deflecto

- DUNDAS JAFINE

- Eastern Sheet Metal

- Lindab Group

- Lennox International

- M&M Manufacturing

- Novaflex Group

- Nuaire

- Rubber World Industries

- Ruskin Titus India

- Saint-Gobain

- Sisneros Bros

- Thermaflex

- Tin Man Sheet Metal

- Turnkey Duct Systems

- Zinger Sheet Metal

The Global Air Ducts Market was valued at USD 5 billion in 2024 and is estimated to grow a CAGR of 3.9% to reach USD 7.4 billion by 2034. This growth is largely driven by the rapid pace of urbanization worldwide and the rising adoption of stringent energy efficiency regulations. As global cities continue to expand, the need for residential, commercial, and industrial infrastructure has surged, directly impacting demand for advanced HVAC systems. These systems rely heavily on air ducts to maintain optimal indoor temperatures and air quality. The growing construction activity across developing and developed regions alike is boosting the installation of modern HVAC systems, consequently fueling the demand for air ducts that are efficient, sustainable, and easy to maintain.

HVAC systems are now a core feature in new buildings, primarily to ensure thermal comfort and energy efficiency. The growing emphasis on green construction practices is creating fresh opportunities in the air ducts industry, with a particular focus on products made from eco-friendly materials. In regions with extreme climates, especially where cooling and ventilation systems are indispensable, there is an evident rise in the use of durable and efficient air duct systems. Commercial buildings are leading adopters of these systems, as air ducts are critical to maintaining indoor air quality in high-traffic zones such as offices, retail stores, transit stations, and multi-use complexes. These areas require round-the-clock air circulation, increasing the necessity for high-performance ducts that are both functional and visually compatible with the architecture.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 3.9% |

In 2024, galvanized steel air ducts held the largest share of the market, generating revenue of over USD 2.8 billion. This material remains a preferred choice among contractors and builders due to its exceptional durability and resistance to wear over time. Galvanized steel ducts require minimal upkeep and offer prolonged performance, making them cost-effective over the long term. Polymer-based air ducts are also gaining traction and are expected to register a CAGR of around 3.6% from 2025 to 2034. These ducts are primarily made from cost-efficient and durable plastics such as PVC and polyethylene. They are lightweight, corrosion-resistant, and easy to install, providing a reliable solution for projects with tight budgets and strict timelines. Their smooth inner surfaces also minimize air resistance, leading to improved airflow and better overall HVAC performance.

The commercial sector dominated the air ducts market in 2024, accounting for about 47% of the global revenue share. Commercial facilities, especially those in urban centers, are prioritizing HVAC systems that support energy efficiency and air quality compliance. In these spaces, aesthetics also play a key role, pushing demand for air ducts that seamlessly integrate with modern interior designs. Ducts used in commercial setups must provide optimal airflow while being adaptable to various layouts and structural configurations.

By shape, round air ducts took the lead in 2024, capturing over 51% of the total market. Their aerodynamic design ensures efficient airflow with reduced noise and minimal pressure drop, making them ideal for both residential and commercial applications. Round ducts are also easier to clean and maintain, offering better long-term reliability and installation flexibility. Rectangular ducts, typically manufactured from metals like galvanized steel, are favored for large-scale commercial and industrial projects due to their structural robustness and compatibility with standardized building designs. These ducts are often integrated into ceilings or wall systems, offering a more compact footprint. Oval ducts, combining the features of both round and rectangular types, are also becoming increasingly popular. They offer a sleek appearance while maintaining strong airflow efficiency, making them ideal for modern buildings where performance and design go hand in hand.

North America represented a significant share of the global air ducts market in 2024, with the United States alone contributing approximately USD 930 million in revenue, which equated to nearly 80% of the regional share. The robust growth in construction and infrastructure development across the U.S. has spurred demand for advanced HVAC installations, particularly systems that support long-term sustainability goals. Builders are actively adopting ducts made from eco-conscious materials to comply with green building regulations and certifications. Moreover, the increased incorporation of smart HVAC systems is driving the need for compatible air ducts that can support connected technologies. This is resulting in a shift toward retrofitting older buildings with new-generation ductwork to enhance air quality, energy efficiency, and temperature control.

Key players in the industry are investing in technology upgrades, facility expansions, and strategic partnerships to expand their market presence and meet evolving customer needs. These moves are enabling them to deliver high-performance air duct solutions that align with changing building codes, energy norms, and design expectations across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Urbanization and infrastructure development

- 3.5.1.2 Energy efficiency regulation

- 3.5.1.3 Climate change

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High installation and maintenance costs

- 3.5.2.2 Complexity of retrofitting in existing structures

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Galvanized steel

- 5.3 Aluminum

- 5.4 Fiber glass

- 5.5 Polymers

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Shape, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Rectangular

- 6.3 Round

- 6.4 Oval

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 DC Duct & Sheet Metal

- 9.2 Deflecto

- 9.3 DUNDAS JAFINE

- 9.4 Eastern Sheet Metal

- 9.5 Lindab Group

- 9.6 Lennox International

- 9.7 M&M Manufacturing

- 9.8 Novaflex Group

- 9.9 Nuaire

- 9.10 Rubber World Industries

- 9.11 Ruskin Titus India

- 9.12 Saint-Gobain

- 9.13 Sisneros Bros

- 9.14 Thermaflex

- 9.15 Tin Man Sheet Metal

- 9.16 Turnkey Duct Systems

- 9.17 Zinger Sheet Metal