|

시장보고서

상품코드

1721574

생검 기기 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Biopsy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

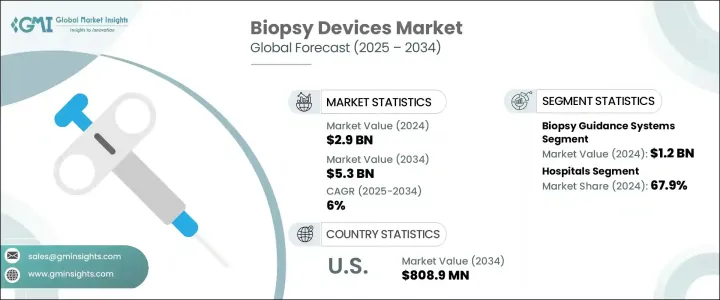

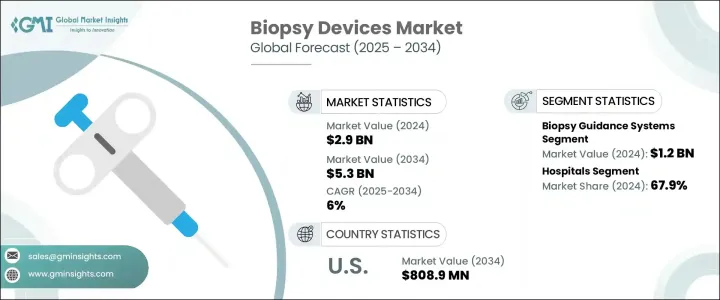

세계의 생검 기기 시장은 2024년 29억 달러에 달했고, CAGR 6%로 성장해 2034년까지 53억 달러에 이를 것으로 예측됩니다.

생검 기기는 진단 평가를 위한 조직 샘플의 추출을 가능하게 함으로써 현대의 건강 관리에서 중요한 역할을 하고 있습니다. 조기 발견, 정확한 진단, 시기 적절한 치료 계획이 중시되고, 생검 기기의 역할은 지금까지 이상으로 중요해지고 있습니다.

현재, 보다 많은 건강관리 전문가들이 정확성, 사용 편의성, 실시간 모니터링을 제공하는 장비로 이동하고 있습니다. 암 진단의 개선에 초점을 맞춘 정부의 대처나 헬스케어 개혁도 시장 확대에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 29억 달러 |

| 예측 금액 | 53억 달러 |

| CAGR | 6% |

시장은 제품 유형별로 바늘 생검 건, 생검 안내 시스템, 생검 집게, 생검 바늘, 기타 관련 기기로 구분됩니다. 생검 안내 시스템은 실시간 이미징과 정확한 타겟팅이 가능하기 때문에 정확성과 최소한의 침습성이 필요한 절차에 이상적입니다. 검증 및 샘플링에 효과적인 시각화가 필수적인 임상 워크플로에 필수적인 것으로 간주되고 있습니다. 이 도구는 병원이나 진단센터의 환경에 점점 짜넣어지고 있어, 그 다기능성에 의해 처리량이 향상해, 전체적인 치료 성적이 최적화되어 왔습니다.

최종 사용자의 관점에서 생검 기기 시장은 병원, 외래수술센터(ASC) 및 기타 환경으로 분류됩니다. 병원은 하이엔드의 화상 진단 기기와 고도의 생검 기술을 실시할 수 있는 숙련된 인재를 이용할 수 있기 때문에 계속 채용의 면에서 리드하고 있습니다.의 조직 샘플링의 필요성이 높아지고 있기 때문에 병원은 이러한 수술에 적합한 환경이 되고 있습니다. 로봇 지원과 저침습 절차의 이용이 현저하게 늘어나고 있으며, 효율과 환자 만족도 모두 향상되고 있습니다.

지역별로는 북미가 여전히 세계의 생검 기기 시장에 크게 공헌하고 있습니다. 특히 미국은 강력한 시장 성장을 나타내고 있으며, 생검 기기의 매출은 2023년 4억 5,190만 달러에서 2034년까지 8억 890만 달러로 증가할 것으로 예측되고 있습니다. 헬스케어 인프라, 높은 시술 건수, 고도의 진단 개입을 서포트하는 유리한 보험 적용이 있습니다. 적극적인 상환 환경에 의해 입원 환자 시설도 외래 환자 시설도 큰 경제적 장벽 없이 최신의 생검 기술을 도입할 수 있어, 복수의 의료 현장에서 널리 이용되도록 되어 있습니다.

경쟁 구도에는 기술, 제품 혁신, 전략적 인수에 대한 지속적인 투자를 통해 아성을 유지하는 세계 리더 기업이 여러 존재합니다. 신규 참가 기업과 중견 제조업체는 대상을 좁힌 임상 용도에 대응하는 비용 효율적인 전용 기기에 주력함으로써 지보를 굳히고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계에서 암 발생률이 상승

- 생검 기기에서의 기술 진보

- 유리한 상환 시나리오

- 유방암에 대한 의식 향상

- 업계의 잠재적 리스크 및 과제

- 생검 후 합병증의 위험

- 숙련된 헬스케어 전문가의 부족

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 생검 안내 시스템

- 매뉴얼

- 로봇

- 침식 생검 건

- 진공 보조 생검(VAB) 장치

- 세침 흡인 생검(FNAB) 장치

- 코어 바늘 생검(CNB) 장치

- 생검 침

- 일회용

- 재사용 가능

- 생검 집게

- 일반 생검 집게

- 핫 생검 집게

- 기타 제품 유형

- 브러쉬

- 큐렛

- 펀치

제6장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제7장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제8장 기업 프로파일

- Argon Medical Devices

- B. Braun Melsungen

- Becton, Dickinson, and Company

- Boston Scientific

- Cardinal Health

- Cook Group

- Devicor Medical Products

- FUJIFILM

- Hologic

- INRAD

- Medtronic

- Olympus Corporation

- Stryker Corporation

The Global Biopsy Devices Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 5.3 billion by 2034. Biopsy devices serve a critical role in modern healthcare by allowing the extraction of tissue samples for diagnostic evaluation. These tools support the identification and analysis of a wide range of medical conditions, often being instrumental in detecting and confirming malignancies. The increasing global burden of chronic diseases, particularly cancer, is pushing the demand for advanced diagnostic solutions. With rising emphasis on early detection, accurate diagnosis, and timely treatment planning, the role of biopsy devices has become more important than ever. The growing preference for image-guided and minimally invasive procedures has led to continuous innovation in biopsy technologies, further improving accuracy and reducing patient recovery time.

More healthcare professionals are now shifting toward devices that offer precision, ease of use, and real-time monitoring. Hospitals and diagnostic centers are also adapting quickly to this shift, which is helping streamline workflows and improve outcomes. Increasing global awareness and access to advanced diagnostic care are fueling the adoption of biopsy equipment across developed and emerging economies. Government initiatives and healthcare reforms focused on improving cancer diagnostics are also contributing to market expansion. Moreover, as procedural volumes continue to rise, providers are investing in efficient, patient-centric biopsy solutions that align with modern clinical demands.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 6% |

The market is segmented by product type into needle-based biopsy guns, biopsy guidance systems, biopsy forceps, biopsy needles, and other associated devices. Among these, biopsy guidance systems held the largest share, generating revenue worth USD 1.2 billion in 2024. Their rising use is largely due to their ability to deliver real-time imaging and precise targeting, making them ideal for procedures requiring accuracy and minimal invasiveness. These systems are now seen as integral to clinical workflows where effective visualization is essential for locating and sampling tissues that are small or difficult to reach. With enhanced compatibility across different imaging modalities, biopsy guidance systems are helping healthcare professionals reduce procedural errors and boost patient safety. These tools are increasingly being integrated into hospital and diagnostic center environments, where their multi-functional capabilities are improving throughput and optimizing overall outcomes.

From the end-user perspective, the biopsy devices market is categorized into hospitals, ambulatory surgical centers, and other settings. Hospitals emerged as the dominant user segment, accounting for 67.9% of the overall market revenue in 2024, with projections estimating the value to reach USD 3.6 billion by 2034. Hospitals continue to lead in terms of adoption due to their access to high-end imaging equipment and skilled personnel capable of performing advanced biopsy techniques. The increasing need for accurate, real-time tissue sampling in complex diagnostic cases makes hospitals a preferred setting for these procedures. The rise in admissions related to chronic diseases and advanced diagnostics is pushing hospitals to invest in more sophisticated biopsy systems. Additionally, there has been significant growth in the use of robotic-assisted and minimally invasive procedures within these environments, improving both efficiency and patient satisfaction. Hospitals are also becoming central hubs for multidisciplinary treatment approaches, where precise diagnostics play a foundational role.

In regional terms, North America remains a leading contributor to the global biopsy devices market. The United States, in particular, has demonstrated strong market growth, with biopsy device revenue expected to rise from USD 451.9 million in 2023 to USD 808.9 million by 2034. This growth can be attributed to a well-established healthcare infrastructure, high procedural volumes, and favorable insurance coverage that supports advanced diagnostic interventions. Positive reimbursement environments enable both in-patient and out-patient facilities to adopt the latest biopsy technologies without significant financial barriers, promoting widespread use across multiple care settings.

The competitive landscape features several global leaders who maintain a stronghold through continued investments in technology, product innovation, and strategic acquisitions. Established players hold a considerable portion of the market thanks to their robust portfolios and commitment to integrated diagnostic solutions. At the same time, newer entrants and mid-tier manufacturers are gaining ground by focusing on cost-effective, specialized devices catering to targeted clinical applications. With growing interest in precision-guided, less invasive diagnostic tools, the biopsy devices industry is expected to see ongoing advancements tailored to the evolving demands of modern healthcare.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of cancer across the globe

- 3.2.1.2 Technological advancements in biopsy devices

- 3.2.1.3 Favorable reimbursement scenario

- 3.2.1.4 Increasing awareness regarding breast cancer

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of complications after biopsy

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Biopsy guidance systems

- 5.2.1 Manual

- 5.2.2 Robotic

- 5.3 Needle based biopsy guns

- 5.3.1 Vacuum-assisted biopsy (VAB) devices

- 5.3.2 Fine needle aspiration biopsy (FNAB) devices

- 5.3.3 Core needle biopsy (CNB) devices

- 5.4 Biopsy needles

- 5.4.1 Disposable

- 5.4.2 Reusable

- 5.5 Biopsy forceps

- 5.5.1 General biopsy forceps

- 5.5.2 Hot biopsy forceps

- 5.6 Other product types

- 5.6.1 Brushes

- 5.6.2 Curettes

- 5.6.3 Punches

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Argon Medical Devices

- 8.2 B. Braun Melsungen

- 8.3 Becton, Dickinson, and Company

- 8.4 Boston Scientific

- 8.5 Cardinal Health

- 8.6 Cook Group

- 8.7 Devicor Medical Products

- 8.8 FUJIFILM

- 8.9 Hologic

- 8.10 INRAD

- 8.11 Medtronic

- 8.12 Olympus Corporation

- 8.13 Stryker Corporation