|

시장보고서

상품코드

1740743

아민 베이스 탄소 포집 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Amine-Based Carbon Capture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

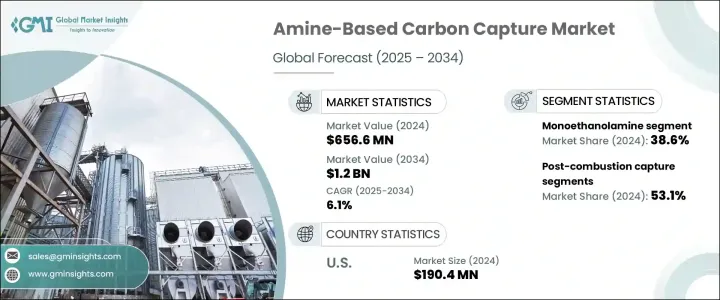

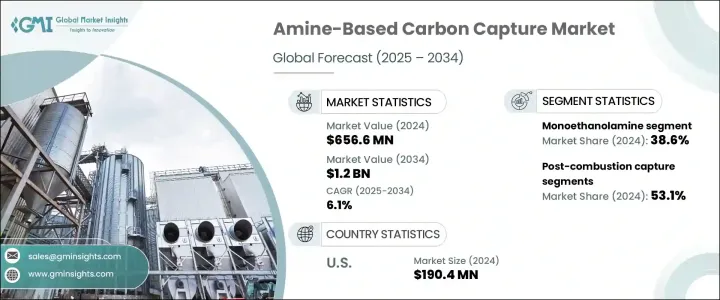

세계의 아민 베이스 탄소 포집 시장은 2024년 6억 5,660만 달러였고, 2034년까지 CAGR 6.1%로 성장해 12억 달러에 이를 것으로 추정됩니다.

각국이 야심찬 탄소 중립 목표를 세우는 동안 효율적이고 확장 가능하며 비용 효율적인 탄소 포집 기술에 대한 수요가 계속 증가하고 있습니다. 아민 기반 탄소 포집은 가장 신뢰할 수 있는 솔루션 중 하나로 부상하고 있으며 기존 인프라를 새롭게 하지 않고 배출량을 크게 줄이는 실용적인 방법을 제공합니다. 기업, 정부, 연구 기관은 에너지 및 제조 분야를 변화시킬 잠재력을 인식하고 첨단 아민 용매 및 시스템 개발에 많은 투자를 하고 있습니다.

이 시장을 견인하는 것은 규제 당국의 압력뿐만 아니라 지속 가능한 기술에 대한 투자자의 관심이 높아지고 있습니다. 지속가능성에 대한 헌신을 지원하면서 컴플라이언스를 보장할 수있는 신뢰할 수있는 장기적인 솔루션을 찾고 있습니다. 이러한 상황에서 아민 기반 탄소 포집은 입증된 성능과 유연성을 제공합니다. 재료 과학, 프로세스 공학, 자동화의 진보에 의해 이 시장은 급속한 확대를 계속해, 신규 참가 기업에도 기존 기업에게 큰 비즈니스 기회를 제공할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 6억 5,660만 달러 |

| 예측 금액 | 12억 달러 |

| CAGR | 6.1% |

아민 기반의 포착 기술은 특히 배기가스에 이산화탄소가 많이 포함되는 연소 후의 용도에 있어서 그 효율의 높이로 알려져 있습니다. 기후 변동 목표를 달성해, 산업계의 이산화탄소 배출량을 삭감하는 긴급성의 상승이, 용제의 성능 향상, CO2 부하 능력의 향상, 재생에 필요한 에너지의 삭감에 중점을 두어, 이 분야의 기술 혁신을

이 분야에서 가장 장래를 바라본 개발의 하나가 아민으로 강화한 고체 흡착제를 이용한 직접 공기 포착입니다. 이 기술은 대기로부터 직접 CO2를 추출함으로써 배출량을 역전시킬 가능성을 지니고 있습니다.

최근 연구개발에서는 아민계 용제의 선택성과 반응성을 향상시키는 데 중점을 두고 있으며, 포착 효율을 높이면서 전체적인 운용 비용을 삭감하는 것을 목표로 하고 있습니다. 에너지 전문가를 포함한 분야 횡단적인 협력에 의해 추진되고 있으며, 이러한 모든 것이 탄소 포집 시스템의 대규모 전개의 실현 가능성을 높이기 위해 노력하고 있습니다.

모노에탄올아민(MEA) 부문은 2024년 시장 점유율에서 38.6%를 차지했습니다. 이산화탄소에 대한 강한 친화도와 안정한 카르바마트 화합물을 형성하는 능력으로 알려진 MEA는 화학 흡수 시스템의 요점으로 계속되고 있습니다. 신뢰성, 운영 안정성 및 널리 이용 가능함으로 인해 특히 레거시 에너지 인프라에서 연소 후 회수의 유력한 선택이 되었습니다.

연소 후 회수 기술은 2024년에 53.1%의 점유율로 시장을 선도했으며, 그 주된 이유는 기존 시스템에의 원활한 통합입니다. 운영 중단을 최소화하면서 탄소 배출을 줄일 수 있기 때문에 산업계는 이 방법을 선호합니다. 수십 년에 걸친 조종사 시험, 상업 프로젝트, 엔지니어링 개선에 힘입어 연소 후 회수는 가장 실용적이고 널리 채택된 솔루션입니다.

미국의 아민 기반 탄소 포집 시장은 2024년 1억 9,040만 달러로 평가되었습니다. 세액공제 등 연방정부의 우대조치와 유연한 주수준의 규제가 결합되어 미국은 탄소회수기술 혁신의 주요 시장이 되고 있습니다. 환경보호청(Environmental Protection Agency)과 주 당국의 위임에 의한 클래스 VI 갱정의 신속한 허가는 프로젝트 일정을 단축하고 투자자의 신뢰를 높이고 도입을 더욱 가속화하고 있습니다.

업계의 주요 기업으로는 Toshiba Energy Systems & Solutions, Linde PLC, Mitsubishi Heavy Industries, Fluor Corporation, Koch-Glitsch, Shell CANSOLV, BASF SE, Pentair, Carbon Clean, and GEA 그룹 등이 있습니다. 이러한 기업은 용제 재생 효율의 향상, 모듈식 탄소 포집 장치의 시작, 파일럿 프로젝트에서 본격적인 상업 운전으로의 스케일 업에 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 주요 제조업체

- 리셀러

- 업계 전체의 이익률

- 공급의 혼란

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 석탄 화력 발전소에서의 연소 후 CO2 포집에서 모노에탄올아민 도입 확대

- 천연 가스 탈황용 메틸디에탄올아민 블렌드의 기술적 개량

- 아민 관능화 고체 흡착제를 사용한 직접 공기 회수(DAC)에 대한 투자 증가

- 업계의 잠재적 위험 및 과제

- 용매 재생에 따른 높은 에너지 페널티와 운용 비용

- 특정 아민의 부식성에 의해 공장의 인프라에 고가의 재료가 필요하게 됨

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 아민유형별, 2021-2034년

- 주요 동향

- 모노에탄올아민

- 디에탄올아민

- 메틸디에탄올아민

- 트리에탄올아민

- 기타

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 연소 후 회수

- 연소 전 회수

- 직접 공기 회수

- 기타

제7장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제8장 기업 프로파일

- BASF SE

- Carbon Clean

- Fluor Corporation

- GEA Group

- Koch-Glitsch

- Linde PLC

- Mitsubishi Heavy Industries

- Pentair

- Shell CANSOLV

- Toshiba Energy Systems & Solutions

The Global Amine-Based Carbon Capture Market was valued at USD 656.6 million in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 1.2 billion by 2034, as global efforts ramp up to combat greenhouse gas emissions, particularly carbon dioxide released from power plants and heavy industries. As countries set ambitious carbon neutrality goals, demand for efficient, scalable, and cost-effective carbon capture technologies continues to rise. Amine-based carbon capture is emerging as one of the most dependable solutions, offering a practical way to significantly reduce emissions without overhauling existing infrastructure. Companies, governments, and research institutions are heavily investing in the development of advanced amine solvents and systems, recognizing their potential to transform the energy and manufacturing sectors.

This market is driven not only by regulatory pressure but also by growing investor interest in sustainable technologies. As carbon pricing mechanisms tighten and decarbonization becomes central to corporate strategies, businesses are seeking reliable, long-term solutions that ensure compliance while supporting sustainability commitments. Moreover, the growing push for circular carbon economies is reinforcing the need for technologies that capture, recycle, and even permanently remove CO2 ,In this context, amine-based carbon capture offers a proven track record of performance and flexibility. It can be deployed at industrial scale today while also serving as a platform for innovation, including integration with carbon utilization and storage systems. With advancements in material science, process engineering, and automation, this market is expected to continue expanding rapidly, offering significant opportunities for new entrants and established players alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $656.6 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 6.1% |

Amine-based capture technology is known for its high efficiency, particularly in post-combustion applications where flue gases are rich in carbon dioxide. The process relies on aqueous amine solutions to chemically absorb CO2 which is then released during the regeneration phase, allowing the solvent to be reused in continuous cycles. This technology is especially well-suited for retrofitting existing coal and gas-fired power plants, as well as other industrial facilities, without the need for extensive modifications. The increasing urgency to meet climate targets and reduce industrial carbon footprints is pushing innovation in this field, with an emphasis on improving solvent performance, increasing CO2 loading capacity, and reducing the energy required for regeneration.

One of the most forward-looking developments in this space is direct air capture using solid sorbents enhanced with amines. Although more energy-intensive than capturing emissions at the source, this technology holds the potential to reverse emissions by extracting CO2 directly from the atmosphere. As attention shifts toward net-negative emission strategies, this approach is gaining traction among climate tech investors and governments alike.

Recent R&D efforts are focused on improving the selectivity and reactivity of amine-based solvents, aiming to reduce overall operational costs while enhancing capture efficiency. This includes the development of new solvent formulations with higher thermal stability and lower degradation rates. Innovations are being driven by cross-sector collaboration involving chemical engineers, environmental scientists, and clean energy specialists, all working toward making carbon capture systems more viable for large-scale deployment. These advancements are particularly important in hard-to-abate sectors like cement, steel, and refining, where electrification is not a feasible path to decarbonization.

The monoethanolamine (MEA) segment accounted for a dominant 38.6% market share in 2024. Known for its strong affinity to carbon dioxide and its ability to form stable carbamate compounds, MEA remains a cornerstone of chemical absorption systems. Its reliability, operational consistency, and widespread availability have made it a go-to choice for post-combustion capture, particularly in legacy energy infrastructure.

Post-combustion capture technologies led the market with a 53.1% share in 2024, largely because of their seamless integration into existing systems. Industries favor this method as it allows them to reduce carbon emissions with minimal disruption to operations. Supported by decades of pilot testing, commercial projects, and engineering improvements, post-combustion capture continues to be the most practical and widely adopted solution.

The United States Amine-Based Carbon Capture Market was valued at USD 190.4 million in 2024. Federal incentives like tax credits, coupled with flexible state-level regulations, have made the U.S. a leading market for carbon capture innovation. Fast-track permitting for Class VI wells by the Environmental Protection Agency and delegated state authorities has shortened project timelines and boosted investor confidence, further accelerating deployment.

Key industry players include Toshiba Energy Systems & Solutions, Linde PLC, Mitsubishi Heavy Industries, Fluor Corporation, Koch-Glitsch, Shell CANSOLV, BASF SE, Pentair, Carbon Clean, and GEA Group. These companies are focusing on enhancing solvent regeneration efficiency, launching modular carbon capture units, and scaling up pilot projects into full-scale commercial operations. Their efforts are helping to drive down costs and improve the scalability of next-generation amine systems across a wide range of industrial applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.1.4 Supply disruptions

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major Exporting Countries

- 3.3.2 Major Importing Countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing deployment of monoethanolamine in post-combustion CO2 capture in coal-fired power plants

- 3.7.1.2 Technological improvements in methyldiethanolamine blends for natural gas sweetening

- 3.7.1.3 Rising investments in direct air capture (DAC) using amine-functionalized solid sorbents

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High energy penalty and operational costs associated with solvent regeneration

- 3.7.2.2 Corrosiveness of certain amines, requiring expensive materials for plant infrastructure

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type of Amines, 2021–2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Monoethanolamine

- 5.3 Diethanolamine

- 5.4 Methyldiethanolamine

- 5.5 Triethanol amine

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021–2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Post-combustion capture

- 6.3 Pre-combustion capture

- 6.4 Direct air capture

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021–2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 BASF SE

- 8.2 Carbon Clean

- 8.3 Fluor Corporation

- 8.4 GEA Group

- 8.5 Koch-Glitsch

- 8.6 Linde PLC

- 8.7 Mitsubishi Heavy Industries

- 8.8 Pentair

- 8.9 Shell CANSOLV

- 8.10 Toshiba Energy Systems & Solutions