|

시장보고서

상품코드

1740746

수술용 헬멧 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Surgical Helmet Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

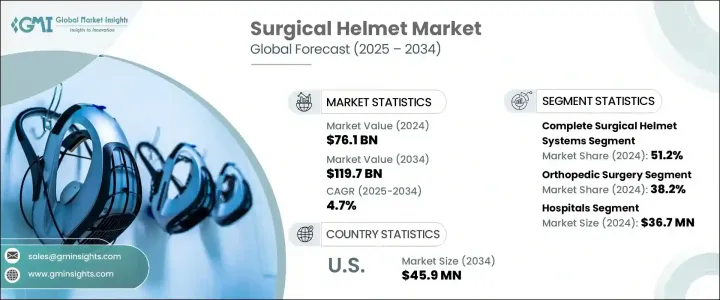

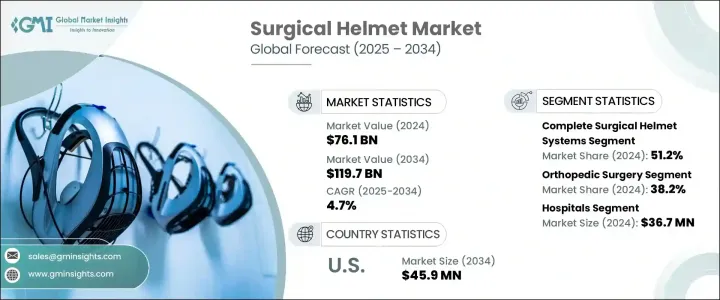

수술용 헬멧 세계 시장은 2024년에 7,610만 달러로 평가되었고, CAGR 4.7%로, 2034년까지는 1억 1,970만 달러에 이를 것으로 추정되고 있습니다.

이 성장은 보다 안전한 수술환경에 대한 수요 증가와 세계에서 실시되고 있는 복잡한 의료치료 증가로 인한 점이 커지고 있습니다. 엄격한 보호 기능을 제공하도록 설계되었으며 수술실 프로토콜의 필수적인 부분이 되었습니다.

시장의 확대는 수술이 필요한 상해의 세계 발생률 증가에 크게 영향을 받고 있습니다. 수술 공간을 확보 할 수있는 헤드 기어 수요도 증가하고 있습니다. 이러한 최신 헬멧은 공기 중의 병원체와 체액으로부터 수술 직원을 보호 할뿐만 아니라 인체 공학적 및 시각적 향상 기능이 통합되어있어 장기간의 치료 중 피로를 완화합니다. 뛰어난 통기성, 향상된 시인성, 경량 소재를 갖춘 고급 모델을 개발함으로써 대응하고 있으며, 모두 엄격한 위생 기준을 유지하면서 사용자 경험을 향상시키는 것을 목적으로 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 7,610만 달러 |

| 예측 금액 | 1억 1,970만 달러 |

| CAGR | 4.7% |

제품 유형별로, 완전한 수술용 헬멧 시스템이 2024년에 세계 시장의 51.2%를 차지해 탑이 되었습니다. 이 헬멧의 인기는 가혹한 수술 환경에서의 시인성을 향상시키는 LED 조명을 내장한 바리에이션이 있어 더욱 높아지고 있습니다.

시장은 또한 용도에 근거한 강력한 세분화을 나타내고 있습니다. 정형외과 수술은 2024년에 최대의 응용 분야를 차지해, 38.2% 시장 점유율을 획득했습니다. 수많은 감염에 노출되는 위험이 높기 때문에 보호 헤드 기어는 수술실 도구의 중요한 구성 요소가 되고 있습니다.

최종 용도에 의하면, 병원이 지배적인 부문으로서 부상해, 2024년에는 3,670만 달러를 차지했습니다. 통상, 병원은 다른 의료 시설에 비해 수술 건수가 많기 때문에 당연히 수술용 헬멧의 소비량도 많아집니다. 많은 감염 관리 규정을 준수하는 경향이 강하고, 많은 사람들이 개인보호구(PPE)의 사용을 의무화하고 있습니다.

미국의 수술용 헬멧 시장은 대폭적인 성장이 예측되어 2034년까지 매출액은 4,590만 달러에 이를 것으로 예측됩니다. 미국의 헬스케어 부문은 감염 대책과 안전 대책을 우선으로 하고 있어 수술용 헬멧은 수술실의 표준 부품이 되고 있습니다.

세계 시장은 경쟁이 치열하며 기존 브랜드와 신규 진출기업 모두 제품 제공의 혁신과 개선을 위해 노력하고 있습니다. Zimmer Biomet, Stryker, MAXAIR Systems, Ecolab, THI Total Healthcare Innovation과 같은 대기업은 시장 점유율의 약 30%를 차지하고 있습니다. 페이스 실드 등의 기능에 투자하고 있습니다. 기술 혁신이 시장 경쟁의 중심인 것에 변함이 없기 때문에 제조업체 각 사는 진화하는 수술 요건이나 규제 기준에 대응하기 위해, 항상 제품을 업그레이드하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 외과 수술 증가

- 도로나 스포츠에서의 사고 증가

- 수술용 헬멧의 기술적 진보

- 감염 대책의 중요성 증가

- 업계의 잠재적 리스크 및 과제

- 고도의 헬멧에 수반하는 고비용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 기술적 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 제품 유형별, 2021년-2034년

- 주요 동향

- 완전한 수술용 헬멧 시스템

- LED 첨부

- LED 없음

- 통기성이 있는 수술용 헬멧

- 기타 제품 유형

제6장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 정형외과

- 뇌신경외과

- 심장 수술

- 이비인후과 수술

- 일반 외과

- 기타 용도

제7장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

제8장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- AresAir

- Beijing ZKSK Technology

- Ecolab

- Kaiser Technology

- Maharani Medicare

- MAXAIR Systems

- Prodancy

- Stryker

- THI Total Healthcare Innovation

- Zimmer Biomet

The Global Surgical Helmet Market was valued at USD 76.1 million in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 119.7 million by 2034. This growth is largely driven by the increasing demand for safer surgical environments and the rising number of complex medical procedures being performed worldwide. As surgical practices continue to evolve, there's a growing emphasis on protective equipment that minimizes the risk of contamination and infection during operations. Surgical helmets have become an essential part of operating room protocols, designed to maintain sterility and offer advanced protective features. These helmets not only cover the surgeon's head but often come equipped with additional functionalities such as built-in lighting, ventilation systems, and powered air supply mechanisms, enhancing both safety and surgeon comfort during long procedures.

Market expansion is significantly influenced by the increased global incidence of injuries requiring surgery. The rising number of emergency surgeries, particularly those involving trauma, has amplified the need for effective protective gear. As surgical volumes climb, so does the demand for headgear that can ensure a sterile and contamination-free operating space. Additionally, improvements in surgical helmet design and technology have made them more accessible and effective for daily use in high-risk surgical environments. These modern helmets not only shield the surgical staff from airborne pathogens and bodily fluids but also reduce fatigue during long procedures by integrating ergonomic and visual enhancements. Manufacturers are responding by developing advanced models with better airflow, improved visibility, and lightweight materials, all aimed at enhancing user experience while maintaining strict hygiene standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $76.1 Million |

| Forecast Value | $119.7 Million |

| CAGR | 4.7% |

In terms of product type, complete surgical helmet systems took the lead in 2024, accounting for 51.2% of the global market. Their dominance is due to the all-in-one nature of these systems, which offer comprehensive protection. These helmets typically cover the entire head and upper body, creating a sealed barrier that minimizes the chances of cross-contamination. Their popularity is further boosted by the availability of variations featuring integrated LED lighting, which supports better visibility in challenging surgical environments. This added feature not only improves the precision of procedures but also reduces visual strain on the surgical team.

The market also shows strong segmentation based on application. Orthopedic surgeries represented the largest application area in 2024, capturing a 38.2% market share. The growing number of procedures related to joint reconstruction, spinal corrections, and other musculoskeletal conditions is fueling this demand. These surgeries often involve long hours and carry a high risk of exposure to infection, making protective headgear a crucial component of operating room gear. The increased frequency of such procedures across both developed and emerging economies highlights the essential role of surgical helmets in modern medicine.

Based on end-use settings, hospitals emerged as the dominant segment, accounting for USD 36.7 million in 2024. Hospitals typically perform a larger volume of surgeries compared to other healthcare facilities, which naturally translates to higher consumption of surgical helmets. Additionally, hospitals are more likely to follow stringent infection control regulations, many of which mandate the use of personal protective equipment. With more financial and infrastructural resources at their disposal, hospitals can invest in higher-quality surgical helmets, reinforcing their leadership position in the market.

The U.S. surgical helmet market is projected to experience considerable growth, with revenues expected to reach USD 45.9 million by 2034. The demand is bolstered by the country's extensive surgical activity and strict regulatory framework regarding surgical safety. The U.S. healthcare sector continues to prioritize infection control and safety measures, making surgical helmets a standard component in operating rooms. This trend is further supported by increasing investments in medical infrastructure and safety technologies.

The global market is competitive, with both established brands and new entrants striving to innovate and improve product offerings. Leading players such as Zimmer Biomet, Stryker, MAXAIR Systems, Ecolab, and THI Total Healthcare Innovation collectively hold around 30% of the market share. These companies are investing in features like advanced ventilation, anti-fog technologies, and integrated face shields to enhance comfort, visibility, and overall surgical performance. As innovation remains central to market competitiveness, manufacturers are constantly upgrading their products to meet evolving surgical requirements and regulatory standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of surgical procedures

- 3.2.1.2 Increasing number of road and sports accidents

- 3.2.1.3 Technological advancements in surgical helmets

- 3.2.1.4 Rising emphasis on infection control

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with advanced helmets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Complete surgical helmet systems

- 5.2.1 With LED

- 5.2.2 Without LED

- 5.3 Ventilated surgical helmets

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Orthopedic surgery

- 6.3 Neurosurgery

- 6.4 Cardiac surgery

- 6.5 ENT surgery

- 6.6 General surgery

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers (ASCs)

- 7.4 Specialty clinics

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AresAir

- 9.2 Beijing ZKSK Technology

- 9.3 Ecolab

- 9.4 Kaiser Technology

- 9.5 Maharani Medicare

- 9.6 MAXAIR Systems

- 9.7 Prodancy

- 9.8 Stryker

- 9.9 THI Total Healthcare Innovation

- 9.10 Zimmer Biomet