|

시장보고서

상품코드

1740754

하이브리드 전동 스쿠터 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Hybrid E-Scooter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

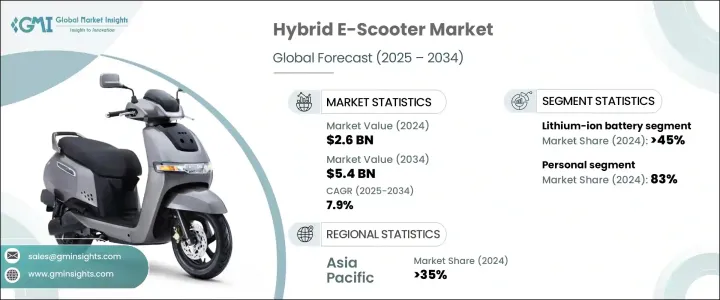

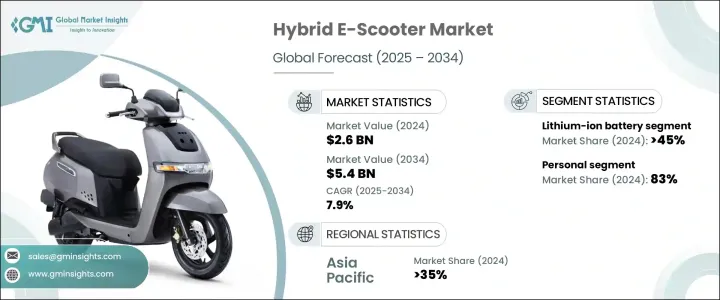

하이브리드 전동 스쿠터 세계 시장 규모는 2024년에는 26억 달러로 평가되었고, 배터리 기술의 진보, 모터 효율의 향상, 환경 의식의 고조를 배경으로, CAGR 7.9%로, 2034년에는 54억 달러에 이를 것으로 예측되고 있습니다.

하이브리드 전동 스쿠터 업계는 도시의 이동성이 지속가능성과 편의성에 강력하게 초점을 맞추면서 진화를 계속하고 있기 때문에 큰 기세를 늘리고 있습니다. 하이브리드 전동 스쿠터는 충전 인프라에 완전히 의존하지 않고 장거리 이동을 요구하는 개인에게 신뢰할 수 있는 솔루션으로 부상하고 있습니다.

깨끗한 운송 수단에 대한 투자 증가와 전동 이동성에 대한 정부의 지원 증가가 이 시장의 미래를 형성하고 있습니다. 인센티브, 보조금을 제공하고 동시에, 관민의 이해 관계자는 하이브리드 모빌리티를 서포트하는 통합 충전 및 급유 인프라를 구축하는 대처를 강화하고 있습니다. 오랫동안 마일리지 딜리버리 서비스의 채택 확대도 하이브리드 전동 스쿠터의 판매를 촉진하는데 있어 매우 중요한 역할을 하고 있습니다. 특히 인구 밀도가 높은 도시 허브에서 특히 두드러집니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 26억 달러 |

| 예측 금액 | 54억 달러 |

| CAGR | 7.9% |

하이브리드 전동 스쿠터는 라이더가 전기 모드와 연료 모드를 원활하게 전환할 수 있도록 하여 탁월한 이점을 제공합니다. 저렴한 경감, 교통량이 많은 존에서의 부드러운 승차 체험이 보장됩니다. 이런 이점에 특히 끌리고 있습니다.리튬 이온 배터리의 사용이 증가하고 있는 것도, 수요에 박차를 가하고 있습니다. 에너지 밀도가 높고, 충전 시간이 짧고, 수명이 긴 것으로 알려져 이 배터리는 하이브리드 스쿠터의 실용성을 크게 향상시킵니다.

환경에 대한 배려도 성장의 중요한 원동력입니다. 대기의 질이 악화되어, 기후 변화가 격화하는 가운데, 세계 각국의 정부는 자동차 공해를 억제하기 위해, 배출 가스 규제를 강화하고 있습니다. 주행 거리나 동력을 희생하지 않으면서도 더 깨끗한 운송에 대한 수요를 충족시켜, 배기가스 배출량이 많은 차량을 단속하는 지역에서는 매력적인 솔루션이 될 수 있습니다.

시장은 주로 배터리 유형에 따라 구분되며, 2024년에는 리튬 이온 배터리가 주도권을 잡고 10억 달러의 수익을 창출합니다. 성능을 발휘하는 능력으로 지지되고 있습니다. 리튬 이온 배터리는 보다 작고 경량인 유닛에 많은 전력을 담을 수 있기 때문에 전체적인 항속 거리를 늘려, 차량 중량을 줄일 수 있습니다.

최종 용도별로는 개인용 하이브리드 전동 스쿠터가 2024년에 83%의 점유율을 차지하고 시장을 독점했습니다. 이 스쿠터는 단거리는 전동으로, 장거리는 연료로 어시스트해주기 때문에 매일 도시 이동에 이상적입니다.

아시아태평양의 하이브리드 전동 스쿠터 시장은 2024년에 35%의 점유율을 차지했지만, 이 지역의 이륜차에 대한 의존도의 높이와 인구 밀도가 높은 도시 덕분에 교통 혼잡이 증가하고 주차 가능성이 제한됨에 따라 하이브리드 e-스쿠터는 매우 실용적이고 친환경적인 운송 대안을 제시합니다. 특히 중국은 강력한 현지 생산 능력, 견고한 공급망 및 유리한 정부 규정으로 업계를 선도하고 있습니다.

Yadea Group, Yamaha, Kymco, NIU Technologies와 같은 주요 기업들은 제품 혁신에 많은 투자를 하고, 생산 라인을 확대하고, 판매 채널을 강화하고 있습니다. 고급 기능을 갖춘 사용자 중심의 스쿠터 개발에 주력하고 있습니다. 세계 시장에서의 존재감을 높이고 경쟁 구도에서 우위를 차지하기 위해서는 현지 유통업체나 국제적인 공급업체와의 전략적 제휴가 필수적입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 부품 공급자

- 기술 공급자

- 최종 용도

- 이익률 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 기술과 혁신의 상황

- 특허 분석

- 가격 분석

- 지역

- 배터리

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 배송 및 물류에 있어서의 상용 이용

- 항속거리 불안과 인프라 갭

- 환경규제와 배출기준

- 배터리와 모터의 효율에 있어서의 기술적 진보

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용

- 유지보수 문제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정 및 예측 : 배터리별, 2021-2034

- 주요 동향

- 리튬 이온 배터리

- 납축전지

- 니켈 수소

- 전고체 전지

제6장 시장 추정 및 예측 : 거리별, 2021-2034

- 주요 동향

- 단거리(15-30 km)

- 중거리(31-60 km)

- 장거리(60 km 이상)

제7장 시장 추정 및 예측 : 판매 채널별, 2021-2034

- 주요 동향

- 온라인

- 오프라인

제8장 시장 추정 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 개인용

- 상업용

제9장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- Gogoro

- Green Tiger Mobility

- Honda

- Jiangsu Xinri E-Vehicle

- Kymco

- Meladath Auto Components

- NIU Technologies

- Okinawa Autotech

- Piaggio Group

- Sanyang Motor

- Silence Urban Ecomobility

- Sunra Electric Vehicle

- Verge Motors

- Yadea Group

- Yamaha

- Zhejiang Luyuan Electric Vehicle

The Global Hybrid E-Scooter Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 5.4 billion by 2034, driven by advancements in battery technology, improved motor efficiency, and rising environmental awareness. The hybrid e-scooter industry is gaining significant momentum as urban mobility continues to evolve with a strong focus on sustainability and convenience. With cities becoming more congested and fuel prices remaining volatile, consumers are actively looking for smarter, greener alternatives that do not compromise on performance or range. Hybrid e-scooters, which combine electric and fuel-powered technologies, are emerging as a reliable solution for individuals seeking extended travel distances without being entirely dependent on charging infrastructure. These dual-mode scooters provide unmatched flexibility for urban commuters, delivery personnel, and everyday users who demand efficiency, affordability, and a lower carbon footprint.

Rising investments in clean transportation, coupled with growing government support for electric mobility, are shaping the future of this market. Numerous state and federal policies now offer tax rebates, incentives, and subsidies that reduce the cost burden for consumers and manufacturers alike. At the same time, public and private stakeholders are ramping up efforts to create integrated charging and refueling infrastructure to support hybrid mobility. The growth of shared mobility platforms and the increasing adoption of last-mile delivery services have also played a pivotal role in driving hybrid e-scooter sales. This trend is particularly noticeable in densely populated urban hubs where quick, affordable, and emission-compliant transport is in high demand. Hybrid e-scooters are not just a lifestyle upgrade-they're fast becoming a strategic tool for achieving smarter urban mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 7.9% |

Hybrid e-scooters offer a distinct edge by allowing riders to switch seamlessly between electric and fuel modes. This dual functionality ensures a longer range, reduced charging anxiety, and a smoother riding experience in traffic-heavy zones. Urban riders and gig economy workers are especially drawn to these benefits, as they need vehicles that are low-maintenance yet high-performing. The rising use of lithium-ion batteries has further fueled the demand. Known for their higher energy density, faster charging time, and extended lifespan, these batteries significantly enhance the practicality of hybrid scooters. Their lightweight and compact design improves handling and boosts energy efficiency, aligning perfectly with the needs of modern-day commuters.

Environmental concerns are another key growth driver. As air quality worsens and climate change intensifies, governments worldwide are enforcing stricter emission norms to curb vehicular pollution. Hybrid e-scooters, which emit significantly less than their gasoline-only counterparts, are quickly becoming the go-to option for eco-conscious consumers. These scooters meet the demand for cleaner transport without compromising on range or power, making them an attractive solution in regions that are clamping down on high-emission vehicles. Consumers are increasingly choosing hybrid e-scooters as a cost-effective and environmentally friendly alternative for short to mid-range travel.

The market is primarily segmented by battery type, with lithium-ion batteries taking the lead in 2024, generating USD 1 billion in revenue. These batteries are favored for their energy efficiency, durability, and ability to deliver consistent performance. They pack more power into a smaller, lighter unit, helping boost the overall range and reducing the vehicle's weight, which in turn improves fuel efficiency and maneuverability-critical features for urban use.

By end-use, personal hybrid e-scooters dominated the market with an 83% share in 2024. Urbanization and rising demand for flexible commuting options are pushing consumers toward personal transport solutions that are both cost-efficient and low-emission. These scooters offer electric riding for short distances and fuel-powered assistance for longer routes, making them ideal for daily city travel. Budget-conscious consumers are especially drawn to them due to their lower fuel and maintenance costs compared to traditional scooters or cars.

The Asia Pacific Hybrid E-Scooter Market accounted for 35% share in 2024, thanks to the region's heavy reliance on two-wheelers and its densely populated urban centers. With increasing traffic congestion and limited parking availability, hybrid e-scooters present a highly practical and eco-friendly transport alternative. China, in particular, continues to lead the way due to its strong local manufacturing capabilities, robust supply chain, and favorable government regulations.

Key players such as Yadea Group, Yamaha, Kymco, and NIU Technologies are investing heavily in product innovation, expanding their production lines, and strengthening distribution channels. These companies focus on creating energy-efficient, user-centric scooters with advanced features, aiming to meet rising consumer expectations. Strategic partnerships with both local distributors and international suppliers are central to boosting their global market presence and staying ahead in the competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component suppliers

- 3.2.3 Technology providers

- 3.2.4 End-use

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Pricing analysis

- 3.7.1 Region

- 3.7.2 Battery

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Commercial use in delivery & logistics

- 3.10.1.2 Range anxiety & infrastructure gaps

- 3.10.1.3 Environmental regulations & emission norms

- 3.10.1.4 Technological advancements in battery and motor efficiency

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost

- 3.10.2.2 Maintenance issues

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Lithium-ion battery

- 5.3 Lead-acid batter

- 5.4 Nickel-metal hydride

- 5.5 Solid-state battery

Chapter 6 Market Estimates & Forecast, By Range Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Short range (15-30 km)

- 6.3 Medium range (31-60 km)

- 6.4 Long range (above 60 km)

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Gogoro

- 10.2 Green Tiger Mobility

- 10.3 Honda

- 10.4 Jiangsu Xinri E-Vehicle

- 10.5 Kymco

- 10.6 Meladath Auto Components

- 10.7 NIU Technologies

- 10.8 Okinawa Autotech

- 10.9 Piaggio Group

- 10.10 Sanyang Motor

- 10.11 Silence Urban Ecomobility

- 10.12 Sunra Electric Vehicle

- 10.13 Verge Motors

- 10.14 Yadea Group

- 10.15 Yamaha

- 10.16 Zhejiang Luyuan Electric Vehicle