|

시장보고서

상품코드

1740761

니들 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Needle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

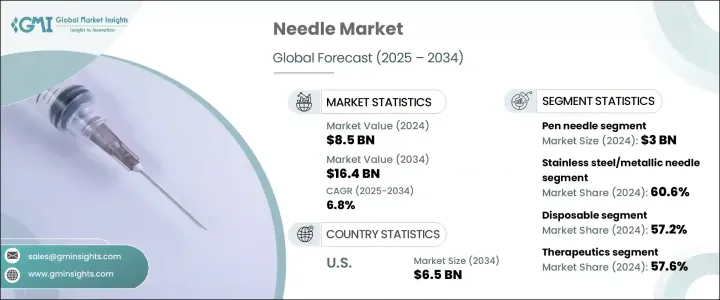

니들 세계 시장은 2024년에는 85억 달러로 평가되었고, 심혈관 질환, 암, 호흡기 합병증, 신경 질환 등의 만성 건강 상태의 만연 증가로 CAGR 6.8%로, 2034년에는 164억 달러에 달할 것으로 추정되고 있습니다.

세계의 건강 관리 상황이 가치 기반 치료로 이동하는 동안 더 나은 환자 결과를 얻고 수술 효율성을 높이고 의료 개입과 관련된 위험을 최소화하는 것이 중요 해졌습니다. 임상 정확성, 편안함 및 안전을 우선시하는 동안 고품질의 안전 설계된 바늘에 대한 수요는 계속 증가하고 있습니다.

니들의 소형화, 첨단부의 예리화, 안전기능의 통합을 추진하는 기술 혁신에 의해 이러한 디바이스는 병원 환경과 재택 간병 환경의 양쪽 모두에서 중심적인 역할을 담당하고 있습니다. 염증 대책이나 헬스 케어 종사자의 안전에 대한 세계의 의식이 높아짐에 따라, 안전 기구를 강화한 스마트 니들 시스템의 필요성이 한층 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 85억 달러 |

| 예측 금액 | 164억 달러 |

| CAGR | 6.8% |

오늘날의 건강 관리 제공업체는 합병증을 줄이고 치료를 합리화하기 위해 정밀하게 설계된 바늘에 의존하고 있습니다. 초극세 칩, 실리콘 코팅, 내장 안전 기구가 내장되어 사용자의 사용성을 향상시키고, 통증과 부상을 최소화하는 설계로 되어 있습니다. 환경에서 매우 중요합니다. 대부분의 니들은 주사기와 카테터와 함께 사용되기 때문에 호환성과 신뢰성은 원활한 치료를 보장하는 데 필수적입니다. 고급 니들 시스템 시장은 계속 성장하고 있습니다. 일상적인 주사와 혈액 채취부터 복잡한 외과 수술에 이르기까지 건강 관리 전문가는 진화하는 케어 요구에 부응하기 때문에 신뢰할 수 있고 무균이며 생체 적합성이 높은 니들 솔루션에 의존합니다.

제품 유형별로 보면 펜니들, 피하주사침, 봉합침, 치과용침, 채혈침, 침술 등이 있습니다. 2024년에는 펜니들의 매출은 30억 달러를 차지했으며, 2034년까지의 CAGR은 6.7%를 나타낼 것으로 예측되고 있습니다. 펜니들의 성장은 비용 효율성, 사용하기 쉬운 디자인, 당뇨병 치료에서 인슐린 투여에 대한 높은 채용률에 기인합니다. 손가락이 부족한 환자와 시력에 문제가 있는 환자, 특히 노인은 안전한 자가주사를 위해 특별히 고안된 펜니들이 제공하는 간편함과 편안함으로부터 혜택을 누리고 있습니다.

재료 유형별로 스테인레스 스틸 및 금속 니들은 2024년 시장 점유율의 60.6%를 차지했습니다. 그 인기는 뛰어난 내식성에서 유래하고 있으며, 고정밀 절차와 무균 상태에서 장시간 사용에 이상적입니다. 이러한 물질은 생체 적합성이 우수하고 부작용을 최소화하고 환자의 안전성을 높입니다. 고온 멸균 하에서의 내구성은 성능을 손상시키지 않고 반복적인 사용을 지원하며 병원과 임상 환경 모두에서 신뢰할 수있는 옵션이되었습니다.

미국의 니들 시장은 헬스케어 기술의 끊임없는 진보와 개인화 치료에 대한 수요 증가에 힘입어 2034년까지 65억 달러에 이를 것으로 예측됩니다. 특히 당뇨병, 암, 기타 만성질환에 의한 질병 부담이 크므로 선진적인 주사침 기반 시스템에 대한 수요가 높아지고 있습니다. 헬스케아이노베이터, 연구기관, 세계 제조업체의 견고한 네트워크를 통해 미국은 최첨단 의료기기의 제품 개발과 신속한 상업화를 이끌고 있습니다. 지원 규제 프레임워크, 건강 관리 인프라에 대한 정부 투자 증가, 안전성과 효율성에 대한 국민 의식 증가가 시장 상승 궤도에 더욱 기여하고 있습니다. 가정 및 원격 의료가 주류가 됨에 따라 사용자 친화적이고 안전하게 최적화된 니들 장비의 사용은 다양한 의료 현장에서 급속히 확대되고 있습니다.

세계 니들 업계의 주요 기업은 Thermo Fisher Scientific, Owen Mumford, B. Braun Medical, Terumo, Merck, Hamilton, Schreiner Group, Cardinal Health, Nipro, Novo Nordisk, Smiths Medical(ICU Medical), Stryker, Becton, Dickinson and Company, Albert David 등이 있습니다. 이러한 기업은 바늘 찌르기 상해의 위험을 줄이기 위해 안전 기능을 강화한 인체공학을 기반으로 한 고정밀 니들 시스템의 개발에 주력하고 있습니다. 연구개발에 엄청난 투자를 하고 지속가능한 제조방법을 도입하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성질환의 유병률 증가

- 주사용 생물제제 수요 증가

- 바늘의 설계에 있어서의 기술적 진보

- 외과 수술 증가

- 업계의 잠재적 위험 및 과제

- 대체 약물전달 방법에 대한 액세스

- 엄격한 규제 요건

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 제품별 2021-2034

- 주요 동향

- 펜니들

- 피하 니들

- 봉합침

- 채혈침

- 치과용 바늘

- 침술침

- 기타 제품

제6장 시장 추정 및 예측 : 재료별 2021-2034

- 주요 동향

- 유리 바늘

- 플라스틱 바늘

- 스테인레스 스틸/금속 바늘

- 폴리에테르에테르케톤(PEEK) 바늘

제7장 시장 추정 및 예측 : 이용 형태별, 2021-2034

- 주요 동향

- 일회용

- 재사용 가능/멸균 가능

제8장 시장 추정 및 예측 : 용도별, 2021-2034

- 주요 동향

- 진단

- 채혈

- 생검

- 샘플 전송

- 기타 진단

- 치료법

- 예방접종

- 약물전달

- 미용처리

- 인슐린 투여

- 치과

- 수술 수술

- 기타 치료법

제9장 시장 추정 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 클리닉

- 진단센터

- 외래수술센터(ASC)

- 재택 케어 환경

- 연구실

제10장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Albert David

- B. Braun Medical

- Becton, Dickinson and Company

- Cardinal Health

- Hamilton

- Merck

- Nipro

- Novo Nordisk

- Owen Mumford

- Schreiner Group

- Smiths Medical (ICU Medical)

- Stryker

- Terumo

- Thermo Fisher Scientific

The Global Needle Market was valued at USD 8.5 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 16.4 billion by 2034, driven by the increasing prevalence of chronic health conditions such as cardiovascular diseases, cancer, respiratory complications, and neurological disorders. As the global healthcare landscape shifts toward value-based care, there's a growing emphasis on delivering better patient outcomes, enhancing procedural efficiency, and minimizing risks associated with medical interventions. The demand for high-quality, safety-engineered needles continues to rise as both healthcare providers and patients prioritize clinical precision, comfort, and safety. Modern medical practices depend on advanced needle technologies to support critical procedures, from diagnostics to drug delivery.

With innovations driving miniaturization, sharper needle tips, and integrated safety features, these devices play a central role in both hospital settings and home care environments. The market also benefits from the expanding elderly population, growing preference for minimally invasive treatments, and increasing adoption of self-administered therapies. As global awareness of infection control and healthcare worker safety intensifies, the need for smart needle systems with enhanced safety mechanisms becomes even more apparent. Surge in outpatient procedures, remote care models, and personalized medicine is further accelerating the evolution of needle products across clinical applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.5 Billion |

| Forecast Value | $16.4 Billion |

| CAGR | 6.8% |

Healthcare providers today rely on precision-engineered needles to reduce complications and streamline care delivery. Whether it's for administering medication, collecting blood samples, or closing surgical wounds, these tools are indispensable to modern medical workflows. Their designs now incorporate ultra-fine tips, silicone coatings, and built-in safety mechanisms to improve user experience and minimize pain or injury. These features significantly improve procedural accuracy and patient comfort, which is crucial in high-stress medical environments. Since most needles are used in conjunction with syringes or catheters, their compatibility and reliability are critical for ensuring seamless care delivery. With rising demand for outpatient services, chronic disease management, and home-based care, the market for advanced needle systems continues to grow. From everyday injections and blood draws to complex surgical procedures, healthcare professionals depend on reliable, sterile, and biocompatible needle solutions to meet evolving care needs.

Based on product type, the market includes pen needles, hypodermic needles, suture needles, dental needles, blood collection needles, acupuncture needles, and others. In 2024, pen needles accounted for USD 3 billion in revenue and are projected to grow at a CAGR of 6.7% through 2034. Their growth stems from their cost-efficiency, user-friendly design, and high adoption rate for insulin administration in diabetic care. Patients with limited dexterity or vision challenges, particularly elderly individuals, benefit from the ease and comfort provided by pen needles, which are specifically designed for safe self-injection.

The material type segment is led by stainless steel and metallic needles, which captured 60.6% of the market share in 2024. Their popularity comes from superior corrosion resistance, making them ideal for high-precision procedures and extended use in sterile conditions. These materials offer excellent biocompatibility, ensuring minimal adverse reactions and enhancing patient safety. Their durability under high-temperature sterilization also supports repeated usage without compromising performance, making them a reliable choice in both hospital and clinical environments.

The United States Needle Market alone is projected to reach USD 6.5 billion by 2034, fueled by continuous advancements in healthcare technologies and growing demand for personalized treatment approaches. The country's high disease burden-particularly from diabetes, cancer, and other chronic illnesses-drives strong demand for advanced needle-based systems. With a robust network of healthcare innovators, research institutions, and global manufacturers, the US leads in product development and rapid commercialization of cutting-edge medical devices. Supportive regulatory frameworks, increased government investment in healthcare infrastructure, and rising public awareness around safety and efficiency further contribute to the market's upward trajectory. As homecare and telehealth become more mainstream, the use of user-friendly, safety-optimized needle devices is expanding rapidly across various care settings.

Some of the leading players in the Global Needle Industry include Thermo Fisher Scientific, Owen Mumford, B. Braun Medical, Terumo, Merck, Hamilton, Schreiner Group, Cardinal Health, Nipro, Novo Nordisk, Smiths Medical (ICU Medical), Stryker, Becton, Dickinson and Company, and Albert David. These companies are focused on developing ergonomic, high-precision needle systems with enhanced safety features to reduce the risk of needlestick injuries. To stay competitive, key players are expanding their global reach through strategic partnerships, investing heavily in R&D, and embracing sustainable manufacturing practices. With healthcare needs evolving rapidly, market participants are actively innovating to deliver smarter, safer, and more cost-effective needle solutions across the globe.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Growing demand for injectable biologics

- 3.2.1.3 Technological advancements in needles design

- 3.2.1.4 Rising number of surgical procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Access to alternative drug delivery methods

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pen needles

- 5.3 Hypodermic needles

- 5.4 Suture needles

- 5.5 Blood collection needles

- 5.6 Dental needles

- 5.7 Acupuncture needles

- 5.8 Other products

Chapter 6 Market Estimates and Forecast, By Material 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Glass needles

- 6.3 Plastic needles

- 6.4 Stainless steel/metallic needles

- 6.5 Polyetheretherketone (PEEK) needles

Chapter 7 Market Estimates and Forecast, By Usage Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Disposable

- 7.3 Reusable/Sterilizable

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostics

- 8.2.1 Blood collection

- 8.2.2 Biopsy

- 8.2.3 Sample transfer

- 8.2.4 Other diagnostics

- 8.3 Therapeutics

- 8.3.1 Vaccination

- 8.3.2 Drug delivery

- 8.3.3 Aesthetic procedures

- 8.3.4 Insulin administration

- 8.3.5 Dental

- 8.3.6 Surgical

- 8.3.7 Other therapeutics

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Clinics

- 9.4 Diagnostic center

- 9.5 Ambulatory surgical centers

- 9.6 Home care setting

- 9.7 Research laboratories

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Albert David

- 11.2 B. Braun Medical

- 11.3 Becton, Dickinson and Company

- 11.4 Cardinal Health

- 11.5 Hamilton

- 11.6 Merck

- 11.7 Nipro

- 11.8 Novo Nordisk

- 11.9 Owen Mumford

- 11.10 Schreiner Group

- 11.11 Smiths Medical (ICU Medical)

- 11.12 Stryker

- 11.13 Terumo

- 11.14 Thermo Fisher Scientific