|

시장보고서

상품코드

1740781

상업용 가스 비상 발전기 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Standby Commercial Gas Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

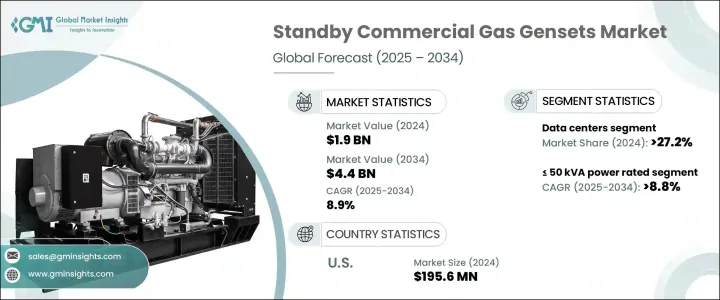

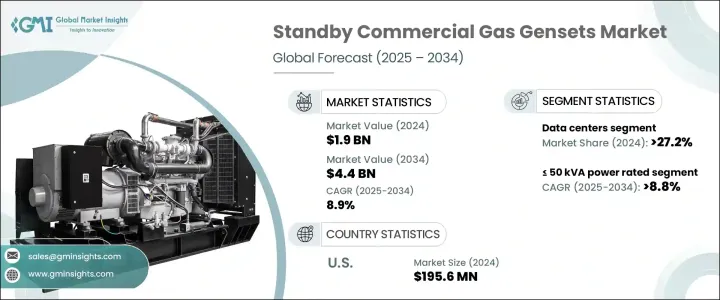

세계 상업용 가스 비상 발전기 시장은 2024년에 19억 달러로 평가되었고, CAGR 8.9%로, 2034년에는 44억 달러에 이를 것으로 추정되고 있습니다.

헬스케어, 소매업, 제조업 등 중요한 상업 분야에서 에너지의 신뢰성에 대한 주목이 높아지고 있다는 것이 비상 발전기 솔루션 수요를 촉진하고 있습니다. 전 세계의 기업들이 유틸리티 인프라의 노후화, 비정상적인 기상, 디지털 의존성 증가로 인한 전력 중단의 위험을 인식하는 동안 비상 발전기의 역할은 더욱 중요해지고 있습니다. 증가는 기존의 디젤 옵션보다 가스 기반 발전기로의 전환을 뒷받침합니다. 낮은 운영 비용, 엄격한 배출 기준 준수율 향상, 스마트 에너지 시스템과의 신속한 통합으로 인해 산업 전반에 걸쳐 미래에 대비한 인프라에 선호되는 선택이 되었습니다. 시장은 또한 IoT 기반 모니터링, 하이브리드 시스템 호환성, 예지보전 기능 등의 기술 혁신을 목격하고 있으며, 중요한 용도에 있어서의 가스발전기의 가치 제안을 더욱 강화하고 있습니다.

상업용 빌딩, 데이터센터, 소매 공간 증가로 전원 백업 요구가 재구성되어 중단 없는 작업을 우선하는 기업이 늘어나고 있습니다. 규제와 낮은 배출 가스 시스템에 대한 정부의 인센티브로 기존의 디젤 시스템에 비해 가스 발전기가 매력적인 솔루션이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 19억 달러 |

| 예측 금액 | 44억 달러 |

| CAGR | 8.9% |

정격 전력 125kVA - 200kVA 부문은 2034년까지 7억 달러의 매출이 예상됩니다. 이 카테고리는 특히 재난 복구 대비에 중점을 둔 모바일 타워와 상업용 허브의 경우 통신 인프라 전반에 걸쳐 여전히 수요가 많습니다. 지속 가능한 운영 및 재해 준비에 대한 의식이 높아짐에 따라 비용, 유연성 및 성능의 최적 균형을 제공하는 중용량 발전기에 대한 투자가 증가하고 있습니다.

2024년 데이터센터용 상업용 가스 비상 발전기 시장 점유율은 27.2%였습니다. 디지털 경제가 확장됨에 따라, 특히 엣지 컴퓨팅과 하이퍼스케일 클라우드 모델의 채택으로 인해 발전기는 데이터 연속성을 보장하는 데 중요한 역할을 하고 있습니다. 스마트 진단, 자동화 대응 컨트롤러, 고급 부하 관리 시스템의 통합으로, 다운타임 거의 제로를 목표로 하는 사업자에게 비상 발전기가 필수적입니다.

미국의 상업용 가스 비상 발전기 시장은 2024년에 1억 9,560만 달러를 창출하였습니다. 판매 부문의 가스 발전기 수요를 높이고 있습니다. 기업은 시동 시간 단축, 유지 보수 필요성 감소, 하이브리드 에너지 시스템과의 원활한 통합을 실현하는 저 배출 솔루션에 주목하고 있습니다.

상업용 가스 비상 발전기 세계 시장에서 주요 기업는 Wartsila, Caterpillar, Atlas Copco, ASHOK LEYLAND, JC Bamford Excavators, Cooper, Kirloskar, MAHINDRA POWEROL, Rolls Royce, Cumins, Siemens Energy, Aggreko International, Mitsubishi Heavy Industries, Rehlko, Sudhir Power 등 각 회사는 혁신, 하이브리드 연료 대응, 현지 생산 확대, 전략적 OEM 제휴, IoT 대응 솔루션에 주력하여 시장에서의 존재감을 높이고 진화하는 고객 수요에 부응하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 전략적 전망

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 출력별, 2021-2034년

- 주요 동향

- 50kVA 이하

- 50kVA-125kVA

- 125kVA-200kVA

- 200kVA-330kVA

- 330kVA-750kVA

- 750kVA 이상

제6장 시장 규모와 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 통신

- 헬스케어

- 데이터센터

- 교육기관

- 정부 센터

- 접객

- 소매

- 부동산

- 상업시설

- 인프라

- 기타

제7장 시장 규모와 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 러시아

- 영국

- 독일

- 프랑스

- 스페인

- 오스트리아

- 이탈리아

- 아시아태평양

- 중국

- 호주

- 인도

- 일본

- 한국

- 인도네시아

- 말레이시아

- 태국

- 베트남

- 필리핀

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 튀르키예

- 이란

- 오만

- 아프리카

- 이집트

- 나이지리아

- 알제리

- 남아프리카

- 앙골라

- 케냐

- 모잠비크

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 칠레

제8장 기업 프로파일

- Aggreko

- ASHOK LEYLAND

- Atlas Copco

- Caterpillar

- Cooper

- Cummins

- Generac Power System

- Genesal Energy

- Green Power International

- JC Bamford Excavators

- Kirloskar

- MAHINDRA POWEROL

- Mitsubishi Heavy Industries

- Rehlko

- Rolls Royce

- Siemens Energy

- Sudhir Power

- Wartsila

The Global Standby Commercial Gas Gensets Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 4.4 billion by 2034. Increasing focus on energy reliability across critical commercial sectors like healthcare, retail, and manufacturing is driving the demand for standby genset solutions. These systems continue to gain strong traction for their ability to deliver consistent backup power during grid failures, blackouts, or emergencies. As businesses worldwide recognize the rising risks of power disruptions due to aging utility infrastructure, extreme weather events, and growing digital dependency, the role of standby gensets becomes even more critical. Shifts toward sustainable operations, surging investments in energy-efficient systems, and rising environmental consciousness are fueling the transition toward gas-based gensets over conventional diesel options. Standby commercial gas gensets are no longer seen as optional but essential components in modern resilience planning. Their lower operational costs, better compliance with tightening emission norms, and quicker integration with smart energy systems have made them a preferred choice for future-ready infrastructure across industries. The market is also witnessing technological innovations like IoT-based monitoring, hybrid system compatibility, and predictive maintenance capabilities, further strengthening the value proposition of gas gensets in critical applications.

The growth of commercial buildings, data centers, and retail spaces is reshaping power backup needs, with businesses increasingly prioritizing uninterrupted operations. Frequent grid instability, outdated power frameworks, and weather-related outages are pushing broader adoption across sectors. Regulatory emphasis on cleaner combustion technologies and government incentives for lower-emission systems are making gas gensets an attractive solution compared to traditional diesel systems. Businesses are favoring gas gensets not only for operational efficiency but also for their lower maintenance needs, improved lifecycle value, and readiness to meet next-generation energy standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $4.4 Billion |

| CAGR | 8.9% |

The >125 kVA to 200 kVA power rating segment is expected to generate USD 700 million by 2034. This category remains in demand across telecom infrastructure, particularly for mobile towers and commercial hubs focused on disaster recovery preparedness. Rising awareness around sustainable operations and disaster readiness is boosting investments in medium-capacity gensets, which offer an optimal balance between cost, flexibility, and performance.

Standby commercial gensets serving data centers accounted for a 27.2% market share in 2024. As the digital economy expands, especially with the adoption of edge computing and hyper-scale cloud models, gensets are becoming vital for ensuring data continuity. Integration of smart diagnostics, automation-ready controllers, and advanced load management systems is making standby gensets indispensable for operators aiming for near-zero downtime.

The U.S. Standby Commercial Gas Gensets Market generated USD 195.6 million in 2024. Stricter emissions regulations, growing sustainability commitments, and increased vulnerability to extreme weather are pushing demand for gas gensets across healthcare, finance, and retail sectors. Businesses are turning to low-emission solutions that deliver faster start times, reduced maintenance needs, and seamless integration with hybrid energy systems.

Key market players in the Global Standby Commercial Gas Gensets Market include Wartsila, Caterpillar, Atlas Copco, ASHOK LEYLAND, JC Bamford Excavators, Cooper, Kirloskar, MAHINDRA POWEROL, Rolls Royce, Cummins, Siemens Energy, Aggreko, Generac Power System, GENSEAL ENERGY, Green Power International, Mitsubishi Heavy Industries, Rehlko, and Sudhir Power. Companies are focusing on innovation, hybrid fuel readiness, local manufacturing expansion, strategic OEM alliances, and IoT-enabled solutions to strengthen market presence and meet evolving customer demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2021 - 2034 ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Telecom

- 6.3 Healthcare

- 6.4 Data centers

- 6.5 Educational institutions

- 6.6 Government centers

- 6.7 Hospitality

- 6.8 Retail sales

- 6.9 Real estate

- 6.10 Commercial complex

- 6.11 Infrastructure

- 6.12 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.6.6 Kenya

- 7.6.7 Mozambique

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 Aggreko

- 8.2 ASHOK LEYLAND

- 8.3 Atlas Copco

- 8.4 Caterpillar

- 8.5 Cooper

- 8.6 Cummins

- 8.7 Generac Power System

- 8.8 Genesal Energy

- 8.9 Green Power International

- 8.10 JC Bamford Excavators

- 8.11 Kirloskar

- 8.12 MAHINDRA POWEROL

- 8.13 Mitsubishi Heavy Industries

- 8.14 Rehlko

- 8.15 Rolls Royce

- 8.16 Siemens Energy

- 8.17 Sudhir Power

- 8.18 Wartsilä