|

시장보고서

상품코드

1740786

동물용 정형외과 의약품 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Veterinary Orthopedic Medicine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

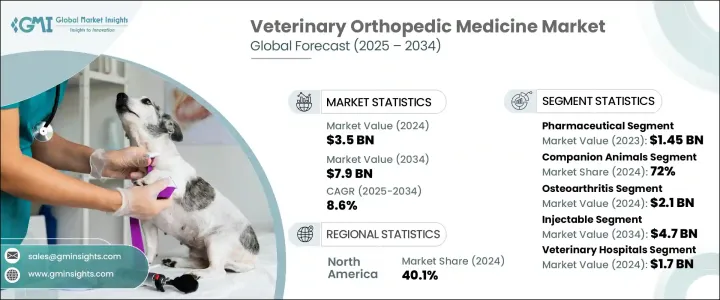

세계 동물용 정형외과 의약품 시장은 2024년에는 35억 달러로 평가되었으며 CAGR 8.6%로 2034년에는 79억 달러에 이를 것으로 추정되고 있습니다.

이 성장의 원동력은 반려동물과 가축 동물 모두에서 정형외과 질환의 유병률의 상승과 생물 제제와 재생 치료에서의 급속한 기술 혁신입니다. 수요가 급증하고 있습니다. 수의 진단, 예방 관리 및 통증 관리 솔루션의 진보로 주인은 조기 개입을 요구하고 동수처리의 장기적인 결과가 향상되었습니다. 반려동물의 고령화에 따라 운동 능력과 삶의 질의 중요성을 인식하고 있습니다. 습관 치료와 최첨단 재생 요법에 대한 강한 주목은 치료 프로토콜에 새로운 기준을 세우고 있습니다.

저침습의 치료법은 동물용 정형외과 치료의 전망을 급속히 바꾸고 있습니다. 질병의 위험이 낮고 치료 후 회복이 빠르기 때문에 널리 사용됩니다. 이 치료법은 만성 정형외과 질환 관리에 특히 유용하며 대규모 외과적 개입없이 지속적인 완화를 제공합니다. 동시에, 의약품은 일상적인 수의학에서 중요한 역할을 계속하고 있습니다. 새롭게 등장한 질환 수식성 변형성 관절증 치료제(DMOADs)는 운동기 질환으로 고통받는 동물들의 통증을 억제하고, 염증을 억제하며, 관절 기능 전체를 개선하는 데 도움이 됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 35억 달러 |

| 예측 금액 | 79억 달러 |

| CAGR | 8.6% |

의약품 부문은 2023년에 14억 5,000만 달러의 매출을 올렸으며, 정형외과 의료에서 매우 중요한 역할을 명확히 했습니다. AI 기반 이동성 평가 도구, 웨어러블 모니터, 첨단 영상 플랫폼을 통해 더 빠른 진단과 개인화된 치료 계획이 가능해지면서 기술은 시장을 더욱 재편하고 있습니다. 정형외과적 문제에 대한 주인의 의식의 고조는 재활 치료에의 액세스의 향상과 함께, 전문적인 정형외과적 개입에 대한 관심을 부추기고 있습니다. 생물 제제, 신규 의약품, 정밀 치료의 개발은 치료 기준을 재정의해 10년간 계속 시장 확대를 주도할 것으로 예측됩니다.

2024년에는 반려 동물 부문이 72%의 압도적인 시장 점유율을 차지하며 관절염과 인대 손상과 같은 관절 질환으로 진단되는 반려 동물 증가를 반영하고 있습니다. 이에 따라 연령 관련 퇴행성 질환이 만연하고 있습니다.

미국의 동물의료용 정형외과 의약 시장은 2024년에 40.1%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 8.5%로 안정적으로 성장할 것으로 예측되고 있습니다.

모듈 변전소 분야에서의 존재감을 높이기 위해 각 사는 스마트 그리드 기술의 채용과 디지털 인프라 통합에 대한 투자를 추진하고 있습니다. 각 회사는 설치에 소요되는 시간과 비용을 줄이는 동시에 도시와 농촌 지역의 응용 분야에서 적응성을 향상시키는 모듈식 설계 혁신에 중점을 둡니다. 에스유닛이 중시되어 공간에 제약이 있는 환경에서의 성능이 향상되고 있습니다. 또한, 주요 기업은 관세의 영향을 완화하고 공급 체인의 탄력성을 확보하기 위해 생산 현지화를 우선합니다. 원격 모니터링 툴과 예측 보전 플랫폼에 대한 투자는 신뢰성과 가동률을 향상시켜 모듈식 변전소가 신속한 송전망 현대화와 재생 가능 에너지 통합에 보다 매력적이 됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 반려동물 사육수 증가와 수의의료비 증가

- 동물복지와 정형외과 질환에 대한 의식의 고조

- 동물의 재생 의료와 통증 관리의 진보

- 업계의 잠재적 위험 및 과제

- 수의사 정형외과 치료의 고액의 비용

- 새로운 치료법이나 의약품에 대한 규제상의 장애물

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 국가별 대응

- 업계에 미치는 영향

- 공급측의 영향(제조 비용)

- 주요 원재료의 가격 변동

- 공급 체인 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(소비자의 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(제조 비용)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 바이오로직스

- 줄기세포

- 혈소판 농축 혈장(PRP)

- 기타

- 관절 내 보충 요법

- 의약품

- 스테로이드

- NSAIDs

- 기타 의약품

제6장 시장 추정 및 예측 : 동물 유형별, 2021-2034년

- 주요 동향

- 반려동물

- 가축

제7장 시장 추정 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 골관절염

- 변형성 관절 질환

- 기타 용도

제8장 시장 추정 및 예측 : 투여 경로별, 2021-2034년

- 주요 동향

- 경구

- 주사

- 국소

제9장 시장 추정 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 동물병원

- 수의사 클리닉

- 기타

제10장 시장 추정 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Ardent Animal Health

- Bimeda

- Bioiberica

- Boehringer Ingelheim

- Ceva Sante Animale

- Contipro

- Contura Vet US

- Elanco Animal Health

- Hester Biosciences

- MEDREGO

- Merck

- PetVivo Holdings

- T-Cyte Therapeutics

- Vetoquinol

- VetStem

- Virbac

- Zoetis

The Global Veterinary Orthopedic Medicine Market was valued at USD 3.5 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 7.9 billion by 2034. This growth is driven by the rising prevalence of orthopedic conditions in both companion and livestock animals, coupled with rapid innovations in biologics and regenerative therapies. As pet ownership rises globally and livestock healthcare gains greater attention, the demand for effective orthopedic solutions continues to surge. Advancements in veterinary diagnostics, preventive care, and pain management solutions are pushing owners to seek early intervention, enhancing long-term outcomes in animal care. Modern pet owners are increasingly prioritizing the overall wellness of their animals, recognizing the importance of mobility and quality of life as pets age. Improved accessibility to veterinary specialists, increasing insurance penetration for animal healthcare, and the booming trend of pet humanization are creating new opportunities for veterinary orthopedic solutions. Furthermore, the strong focus on minimally invasive procedures and cutting-edge regenerative therapies is setting a new standard in treatment protocols. As technology integration deepens, orthopedic medicine for animals is rapidly evolving, creating a dynamic landscape for clinicians, researchers, and pharmaceutical companies alike.

Minimally invasive treatment methods are rapidly transforming the veterinary orthopedic care landscape. Techniques such as viscosupplementation, platelet-rich plasma (PRP) therapy, and stem cell-based regenerative medicine are witnessing widespread adoption thanks to their lower risk of complications and faster post-treatment recovery. These therapies are particularly valuable for managing chronic orthopedic conditions, offering sustained relief without the need for extensive surgical intervention. At the same time, pharmaceutical solutions continue to play a crucial role in daily veterinary care. Non-steroidal anti-inflammatory drugs (NSAIDs), corticosteroid injections, and emerging disease-modifying osteoarthritis drugs (DMOADs) help control pain, reduce inflammation, and improve overall joint function in animals suffering from musculoskeletal disorders.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 8.6% |

The pharmaceutical segment generated USD 1.45 billion in 2023, underscoring its pivotal role in orthopedic care. Technology is further reshaping the market, with AI-enabled mobility assessment tools, wearable monitors, and advanced imaging platforms enabling faster diagnosis and more personalized treatment plans. Growing awareness among pet owners about orthopedic issues, coupled with better access to rehabilitation therapies, is fueling interest in specialized orthopedic interventions. Developments in biologics, novel pharmaceuticals, and precision therapies will continue to redefine treatment standards, driving market expansion over the next decade.

In 2024, the companion animals segment held a dominant 72% market share, reflecting the growing number of pets diagnosed with joint conditions like arthritis and ligament injuries. As veterinary healthcare advances and pets live longer, age-related degenerative diseases are becoming more prevalent. Rehabilitation options such as hydrotherapy and physiotherapy are increasingly available and often covered by pet insurance, making advanced orthopedic care more accessible.

The United States veterinary orthopedic medicine market accounted for a 40.1% share in 2024 and is projected to grow steadily at a CAGR of 8.5% through 2034. The country's leadership stems from widespread pet ownership, a heightened focus on animal wellness, and rising awareness about early diagnosis and specialized orthopedic treatments among pet owners.

To strengthen their presence in the modular substation space, companies are adopting smart grid technologies and investing in digital infrastructure integration. Strategic collaborations with power utilities and infrastructure developers are helping secure large-scale deployments. Firms are focusing on modular design innovations that reduce setup time and cost while improving adaptability in both urban and rural applications. Increased emphasis on compact, gas-insulated units enhances performance in space-constrained settings. Additionally, key players prioritize localization of production to mitigate tariff impacts and ensure supply chain resilience. Investments in remote monitoring tools and predictive maintenance platforms boost reliability and operational uptime, making modular substations more appealing for rapid grid modernization and renewable energy integration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership and increased spending on veterinary care

- 3.2.1.2 Growing awareness of animal welfare and orthopedic disorders

- 3.2.1.3 Advancements in regenerative medicine and pain management for animals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary orthopedic treatments

- 3.2.2.2 Regulatory hurdles for new therapies and pharmaceuticals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Biologics

- 5.2.1 Stem cells

- 5.2.2 Platelet-rich plasma (PRP)

- 5.2.3 Other biologics

- 5.3 Viscosupplements

- 5.4 Pharmaceuticals

- 5.4.1 Steroids

- 5.4.2 NSAIDs

- 5.4.3 Other pharmaceuticals

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Companion animals

- 6.3 Livestock animals

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Osteoarthritis

- 7.3 Degenerative joint disease

- 7.4 Other applications

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Topical

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals

- 9.3 Veterinary clinics

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Ardent Animal Health

- 11.2 Bimeda

- 11.3 Bioiberica

- 11.4 Boehringer Ingelheim

- 11.5 Ceva Sante Animale

- 11.6 Contipro

- 11.7 Contura Vet US

- 11.8 Elanco Animal Health

- 11.9 Hester Biosciences

- 11.10 MEDREGO

- 11.11 Merck

- 11.12 PetVivo Holdings

- 11.13 T-Cyte Therapeutics

- 11.14 Vetoquinol

- 11.15 VetStem

- 11.16 Virbac

- 11.17 Zoetis