|

시장보고서

상품코드

1740797

뇌경색 치료 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Cerebral Infarction Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

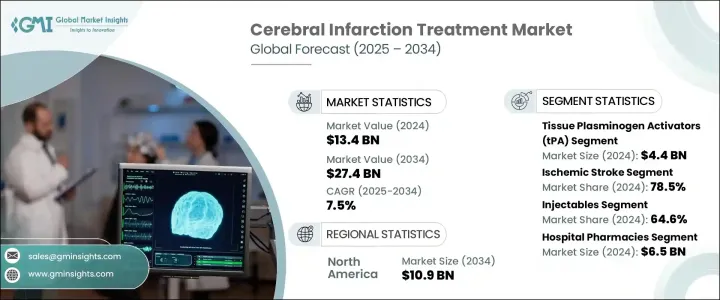

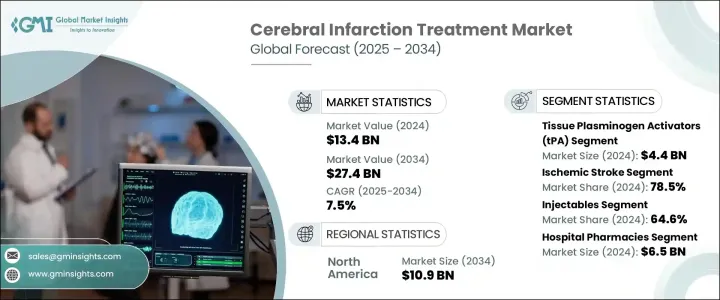

세계의 뇌경색 치료 시장 규모는 2024년에 134억 달러에 달했고, CAGR 7.5%로 성장해 2034년까지 274억 달러에 이를 것으로 예측되고 있습니다.

이 시장은 뇌졸중의 유병률 증가와 적시 치료의 중요성에 대한 의식 증가로 꾸준한 성장을 이루고 있습니다. 이 혈류 장애는 일반적으로 혈전이 혈관을 막고 뇌 세포에서 산소와 필수 영양소를 빼앗아서 발생합니다. 또한, 임상 연구의 진보나 신경 질환에 대한 보조금 증가에 의해 혁신적인 치료법이나 치료 옵션의 개발이 가속해, 시장 확대의 원동력이 되고 있습니다. 위험 요인이 급증하는 가운데, 보다 신속하고 효과적인 뇌경색 치료에 대한 수요는 계속 증가하고 있습니다.

약물 등급별로 조직 플라스미노겐 활성화제(tPA), 항응고제, 항혈소판제, 항경련제 및 기타 약물로 구분됩니다. 조직 플라스미노겐 활성화 약물은 혈전 형성에 관여하는 핵심 단백질인 피브린을 분해하여 혈전을 용해시키고 뇌로의 혈류를 재확립하고 산소 손실과 관련된 손상을 최소화합니다. 발증부터 수시간 이내에 tPA를 투여하면 회복이 현저하게 촉진되고 장애가 완화되며 전반적인 치료 성적이 향상되는 것으로 나타났습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 134억 달러 |

| 예측 금액 | 274억 달러 |

| CAGR | 7.5% |

시장을 유형별로 분류하면 허혈성 뇌졸중과 출혈성 뇌졸중으로 나눌 수 있습니다. 이 우위는 허혈성 뇌졸중의 세계적 발생률이 다른 유형에 비해 높기 때문입니다. 환자는 재발 예방을 위해 일상적으로 처방됩니다. 조기 치료는 운동, 언어 및 인지 회복을 크게 개선하고 장기적인 장애의 가능성을 줄이기 위해 시장 성장을 지원합니다.

투여 경로에 따라 시장은 경구 요법과 주사 요법으로 나뉘어져 있습니다. 의료 제공자는 혈전용해제를 신속하게 혈류에 직접 전달할 수 있어 일각을 다투는 긴급시에 신속한 치료효과를 얻을 수 있습니다.

유통 채널별로는 병원 약국이 2024년에 최대의 매출 점유율을 차지해, 65억 달러를 낳았습니다. 이러한 환경에서는 의사 관리 하에서 구명약에 직접 액세스할 수 있기 때문에 특히 긴급성을 필요로 하는 치료에 중요합니다.

지역별로는 북미가 주요 시장의 지위를 차지하고 있으며, 2024년의 매출은 54억 달러, 2034년에는 109억 달러에 이를 것으로 예측되고 있습니다. 높은 헬스케어 지출, 첨단 의료 인프라, 뇌졸중 치료에 대한 의식이 높아지면서 이 지역의 지배적 지위를 유지하고 있습니다.

시장 전체의 약 45%를 차지하는 주요 기업으로는 Abbott Laboratories, Beringer Ingelheim, F. Hofman La Roche, Novo Nordisc 등의 기업이 포함됩니다. 지속적으로 건강 관리 기관 및 공중 보건 기관과의 파트너십은 연구 활동을 촉진하고 치료에 대한 액세스를 향상시키고 있으며, 계몽 캠페인과 디지털 플랫폼의 영향력이 증가함에 따라 더 많은 사람들이 적시에 치료를 받도록 촉진하고 시장 성장에 기여합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심혈관 질환의 유병률 상승

- 의약품 개발에 있어서의 혁신

- 뇌졸중 치료제의 연구개발 강화

- 고령자 인구 증가

- 업계의 잠재적 위험 및 과제

- 약의 부작용

- 엄격한 규제 틀

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 국가별 대응

- 업계에 미치는 영향

- 공급측의 영향(제조 비용)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(소비자의 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(제조 비용)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 파이프라인 분석

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 약제 클래스별, 2021-2034년

- 주요 동향

- 조직 플라스미노겐 활성화 인자(tPA)

- 항응고제

- 항혈소판제

- 항경련제

- 기타 약물 클래스

제6장 시장 추계 및 예측 : 유형별, 2021-2034년

- 주요 동향

- 허혈성 뇌졸중

- 출혈성 뇌졸중

제7장 시장 추계 및 예측 : 투여 경로별, 2021-2034년

- 주요 동향

- 경구

- 주사제

제8장 시장 추계 및 예측 : 유통채널별, 2021-2034년

- 주요 동향

- 병원 약국

- 소매 약국

- 온라인 약국

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Abbott Laboratories

- Amgen

- Amneal Pharmaceuticals

- AstraZeneca

- Boehringer Ingelheim

- Bayer

- Biogen

- Daiichi Sankyo Company

- F. Hoffmann-La Roche

- Merck &Co.

- Novartis

- Novo Nordisk

- Otsuka Holdings

- Pfizer

- Sanofi

The Global Cerebral Infarction Treatment Market was valued at USD 13.4 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 27.4 billion by 2034. This market is witnessing steady growth due to the increasing prevalence of stroke and rising awareness about the importance of timely treatment. Cerebral infarction, a form of stroke caused by an interruption in blood flow to the brain, leads to tissue damage and, if left untreated, can result in long-term disability or death. This interruption is typically caused by a blood clot blocking a vessel, depriving brain cells of oxygen and essential nutrients. As medical infrastructure and diagnostic capabilities improve globally, earlier detection and more effective treatments are becoming available, pushing the demand for therapeutic interventions. Additionally, advances in clinical research and increased funding for neurological disorders are accelerating the development of innovative therapies and treatment options, driving market expansion. With a growing geriatric population and a surge in risk factors like hypertension and diabetes, the demand for more responsive and effective cerebral infarction treatments continues to climb. The emergence of emergency care systems and rapid-response treatment options has significantly influenced patient outcomes, thus boosting the market's long-term potential.

By drug class, the cerebral infarction treatment market is segmented into tissue plasminogen activators (tPA), anticoagulants, antiplatelets, anticonvulsants, and other drugs. The total market revenue for 2023 was USD 12.6 billion. The tPA segment alone generated USD 4.4 billion in 2024 and is expected to grow at a CAGR of 7.8% throughout the forecast period. Tissue plasminogen activators help dissolve blood clots by breaking down fibrin, a core protein involved in clot formation, thus reestablishing blood flow to the brain and minimizing oxygen loss-related damage. Administering tPA within the first few hours of symptom onset has been shown to significantly improve recovery, reduce disability, and enhance overall treatment outcomes. These therapies are now considered essential in emergency stroke protocols due to their efficiency and ability to reduce long-term neurological impairment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.4 Billion |

| Forecast Value | $27.4 Billion |

| CAGR | 7.5% |

When categorized by type, the market is divided into ischemic stroke and hemorrhagic stroke. Ischemic stroke dominated the segment with a revenue of USD 10.5 billion in 2024, accounting for 78.5% of the total market. This dominance is attributed to the high global incidence of ischemic strokes compared to other types. Treatments like thrombolysis and thrombectomy are increasingly adopted to restore blood flow and limit neurological damage. Medications such as antiplatelets (aspirin, clopidogrel) and anticoagulants (including dabigatran and rivaroxaban) are routinely prescribed to prevent recurrence, particularly in patients with underlying cardiovascular risk factors. Early treatment greatly improves motor, speech, and cognitive recovery, which helps reduce the chances of long-term disability, thereby supporting market growth.

Based on the route of administration, the market is segmented into oral and injectable therapies. Injectables accounted for a significant 64.6% share of the total market in 2024. These therapies are favored in emergency settings due to their fast action and precise dosage control, essential for acute stroke treatment. Intravenous administration allows healthcare providers to quickly deliver clot-dissolving medications directly into the bloodstream, providing rapid therapeutic effects when time is critical. Their suitability in ambulances and hospital environments enhances their value in modern stroke care systems, making injectables a cornerstone of immediate intervention strategies.

In terms of distribution channels, hospital pharmacies held the largest revenue share in 2024, generating USD 6.5 billion. These settings offer direct access to life-saving drugs under medical supervision, particularly important for treatments requiring urgent attention. Hospital pharmacies also play a key role in patient education, offering guidance on medication types, administration methods, and side effects. Their integration with healthcare teams ensures better adherence to treatment plans, improving patient outcomes. Additionally, services such as medication management and support programs foster long-term treatment success.

Regionally, North America emerged as a leading market, with a revenue of USD 5.4 billion in 2024 and a projected rise to USD 10.9 billion by 2034. The United States was the largest contributor, with USD 4.7 billion in revenue in 2023. The region's high healthcare expenditure, advanced medical infrastructure, and increased awareness about stroke care have helped it maintain its dominant position. The growing incidence of cardiovascular conditions in this region further fuels the need for effective treatments.

Key market players-accounting for roughly 45% of the total share-include companies such as Abbott Laboratories, Boehringer Ingelheim, F. Hoffmann-La Roche, and Novo Nordisk. These companies continue to lead the market through strategic product innovations, robust distribution networks, and regulatory expertise. Partnerships with healthcare institutions and public health organizations are facilitating research efforts and improving treatment accessibility. Awareness campaigns and the growing influence of digital platforms are also encouraging more individuals to seek timely treatment, thus contributing to market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases

- 3.2.1.2 Innovation in drug development

- 3.2.1.3 Increasing R&D for stroke therapeutics

- 3.2.1.4 Growing number of geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects of medications

- 3.2.2.2 Stringent regulatory framework

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of Manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to Consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of Manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Pipeline analysis

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Tissue plasminogen activators (tPA)

- 5.3 Anticoagulants

- 5.4 Antiplatelets

- 5.5 Anticonvulsants

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Ischemic stroke

- 6.3 Hemorrhagic stroke

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Amgen

- 10.3 Amneal Pharmaceuticals

- 10.4 AstraZeneca

- 10.5 Boehringer Ingelheim

- 10.6 Bayer

- 10.7 Biogen

- 10.8 Daiichi Sankyo Company

- 10.9 F. Hoffmann-La Roche

- 10.10 Merck & Co.

- 10.11 Novartis

- 10.12 Novo Nordisk

- 10.13 Otsuka Holdings

- 10.14 Pfizer

- 10.15 Sanofi