|

시장보고서

상품코드

1740818

스티어링 타이로드 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Steering Tie Rod Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

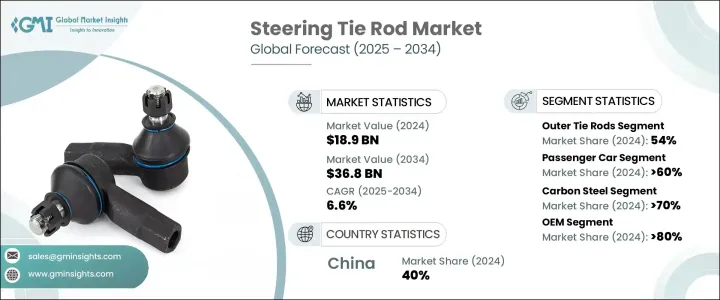

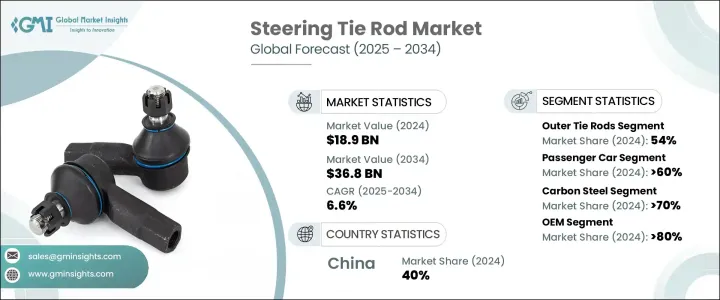

세계의 스티어링 타이로드 시장 규모는 2024년 189억 달러에 달하고, CAGR 6.6%로 성장해 2034년까지 368억 달러에 이를 것으로 예측되고 있습니다.

이러한 성장의 주요 요인은 자동차 산업의 급속한 확대이며, 특히 산업화와 도시 개발이 급속히 진행되고 있는 지역에서 현저합니다. 적절한 차량 제어를 유지하고 거리에서 안전을 확보하기 위해 필수적인 중요한 부품 수요 증가로 이어집니다.

스티어링 시스템은 자동차 기술의 혁신이 자동차 섹터의 형태를 계속 바꾸고 있기 때문에 현저한 변모를 이루고 있습니다. 최신의 발전은 더욱 널리 퍼지고 있습니다. 자동차가 더 스마트해지고 일렉트로닉스에 대한 의존도가 높아짐에 따라 스티어링 타이로드와 같은 정밀하게 설계된 부품에 대한 수요가 더욱 중요해지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 189억 달러 |

| 예측 금액 | 368억 달러 |

| CAGR | 6.6% |

제품 세분화에서 시장은 내부 타이로드와 외부 타이로드로 나뉩니다. 이러한 부품은 외부에 배치되어 교체 빈도가 높고 환경 노출과 마모에 더 취약합니다. 마모된 아우터 타이로드는 스티어링 응답의 저하와 타이어의 불균일한 마모의 원인이 됩니다.

시장을 차종별로 보면 승용차는 2024년 총 판매 대수의 60% 이상을 차지했고 2034년까지 약 6%의 연평균 복합 성장률(CAGR)로 계속 확대될 것으로 예측됩니다. 차량의 안전한 핸들링에 필수적이기 때문에 특히 주행거리가 많거나 악로를 주행하는 경우에는 정기적인 점검과 교환이 필요하게 되는 경우가 많습니다.

재료별로는 탄소강이 2024년에 스티어링 타이로드의 제조에 선호되는 선택지로서 부상해, 시장 점유율의 70% 이상을 차지했습니다. 이러한 대체 재료보다 비용면에서 유리하기 때문에 제조 업체는 고성능 부품을 경쟁력있는 가격으로 제공할 수 있습니다.

판매 채널의 관점에서 볼 때 OEM은 2024년 스티어링 타이로드 시장의 80% 이상을 차지하고 있습니다. 자동차 제조업체는 일관성, 품질 보증, 차량의 오리지널 엔지니어링 설계를 지원하는 능력에서 이러한 부품을 선호합니다.

지역적으로는 중국이 2024년 세계 점유율의 40% 가까이를 차지해 시장을 선도해 약 164억 달러의 매출을 낳았습니다. 중국은 제조업체와 공급업체의 강력한 기반의 혜택을 누리고 있으며, 스티어링 타이 로드의 효율적인 생산과 광범위한 유통을 가능하게 하고 있습니다.

세계 기업은 제품 라인을 확장하고 첨단 기술을 통합하기 위해 투자를 계속하고 있습니다. 혁신 기술을 채택하여 최신 자동차 시장의 진화하는 수요에 맞는 제품을 제공합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 자동차 OEM

- 공급자

- 재료 및 단조 회사

- 애프터마켓의 유통업체 및 소매업체

- 최종 용도

- 공급자의 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 주요 원재료의 가격 변동

- 공급 체인 재구성

- 최종 시장에의 가격 전달

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 무역에 미치는 영향

- 가격 동향

- 지역

- 제품

- 코스트 내역 분석

- 이익률 분석

- 기술과 혁신의 상황

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 세계 자동차 생산 증가

- 스티어링 시스템의 기술적 진보

- 차량의 안전성과 규제 준수를 중시

- 전기차와 자율주행차의 성장

- 업계의 잠재적 위험 및 과제

- 전기자동차와 자동 운전 기술에 의한 파괴적 변화

- 원재료 가격의 변동과 공급망의 혼란

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 이너 타이로드

- 아우터 타이로드

제6장 시장 추계 및 예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 경형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제7장 시장 추계 및 예측 : 재료별, 2021-2034년

- 주요 동향

- 탄소강

- 스테인레스 스틸

제8장 시장 추계 및 예측 : 판매채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- ACDelco

- APA Industries

- BorgWarner

- Bosch Group

- Crown Automotive Sales

- CTR

- Delphi Technologies

- Dorman Products

- First Line

- HL Mando

- Ingalls Engineering

- JTEKT

- Mando

- Moog

- Motorcraft

- Nexteer Automotive Group Limited

- NSK

- Sankei Industry

- Synergy Manufacturing

- ZF Friedrichshafen

The Global Steering Tie Rod Market was valued at USD 18.9 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 36.8 billion by 2034. This growth is primarily fueled by the rapid expansion of the automotive industry, especially in regions undergoing fast-paced industrialization and urban development. As more people gain access to higher disposable incomes and infrastructure improves, the demand for vehicles rises significantly. The surge in vehicle production naturally translates into higher demand for crucial components like steering tie rods, which are essential for maintaining proper vehicle control and ensuring safety on the road. With growing expectations for vehicle performance and longevity, automakers and consumers alike are demanding advanced, durable steering systems that can withstand modern driving conditions.

The steering system is undergoing a notable transformation as innovations in vehicle technology continue to reshape the automotive sector. Modern advancements such as electric power steering, steer-by-wire configurations, and the incorporation of sensors are becoming more widespread. These developments are not just enhancing vehicle performance-they are also making cars more fuel-efficient and safer to drive. As vehicles become smarter and more reliant on electronics, the demand for precisely engineered parts like steering tie rods becomes even more important. These components must now meet higher standards of accuracy and reliability to ensure optimal integration with advanced steering systems. The shift toward automation and electronic driving assistance has intensified the need for parts that can deliver precision, minimal mechanical complexity, and improved handling.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.9 Billion |

| Forecast Value | $36.8 Billion |

| CAGR | 6.6% |

In terms of product segmentation, the market is divided into inner and outer tie rods. Outer tie rods held the dominant position in 2024, accounting for around 54% of the market, and are projected to grow at a CAGR of 7.2% throughout the forecast period. These components face more frequent replacements due to their external position, which makes them more vulnerable to environmental exposure and wear. Being constantly subjected to road debris, moisture, and harsh elements leads to quicker degradation. When not replaced in time, worn-out outer tie rods can contribute to poor steering response and uneven tire wear. This naturally increases demand within the automotive aftermarket, making outer tie rods a crucial revenue-driving segment.

When examining the market by vehicle type, passenger cars represented more than 60% of total sales in 2024 and are expected to continue expanding at a CAGR of approximately 6% through 2034. Passenger vehicles tend to remain in service longer and require ongoing maintenance as they age, leading to consistent demand for replacement parts. Steering tie rods, being critical to safe vehicle handling, often need periodic inspection and substitution, especially in high-mileage or rough-road driving scenarios. The growing number of passenger cars in operation globally ensures a sustained need for both OEM and aftermarket tie rod products, reinforcing this segment's leading position in the overall market.

Material-wise, carbon steel emerged as the preferred choice for manufacturing steering tie rods in 2024, accounting for over 70% of the market share. Its popularity stems from a combination of high strength and durability, allowing it to endure continuous stress and road shocks over time. Carbon steel also offers a cost advantage over alternative materials like aluminum or titanium, enabling manufacturers to deliver high-performance parts at competitive pricing. This balance of quality and cost-effectiveness makes carbon steel a practical option for both OEMs and aftermarket suppliers, especially in a price-sensitive market like automotive components.

From a sales channel perspective, OEMs captured more than 80% of the steering tie rod market in 2024. The strong presence of OEMs can be attributed to the need for original parts during vehicle assembly. OEM components are designed to match the exact specifications of new vehicles and come with warranties that assure performance and compatibility. Automakers prefer these components for their consistency, quality assurance, and the ability to support the vehicle's original engineering design. The growth in global vehicle production has significantly driven demand from this segment.

Geographically, China led the market in 2024 with nearly 40% of the global share, generating around USD 16.4 billion in revenue. This leadership is supported by the country's high volume of vehicle production and a well-established supply chain for automotive components. China benefits from a strong base of manufacturers and suppliers, enabling efficient production and widespread distribution of steering tie rods. Competitive pricing, combined with high-quality standards, has allowed local producers to meet both domestic and international demands effectively.

Global players continue to invest in expanding their product lines and integrating advanced technologies. Strategic partnerships and R&D initiatives are being used to enhance product performance and durability. These companies are embracing innovations like steer-by-wire and electric steering systems, ensuring their offerings align with the evolving demands of the modern automotive market. Meanwhile, regional manufacturers focus on tailoring their products to local requirements, offering customized solutions that resonate with specific vehicle types and driving environments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Automotive OEMs

- 3.1.2 Suppliers

- 3.1.3 Material and forging companies

- 3.1.4 Aftermarket distributors and retailers

- 3.1.5 End use

- 3.2 Supplier landscape

- 3.3 Impact of trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on the industry

- 3.3.2.1 Price volatility in key materials

- 3.3.2.2 Supply chain restructuring

- 3.3.2.3 Price transmission to end markets

- 3.3.3 Strategic industry responses

- 3.3.3.1 Supply chain reconfiguration

- 3.3.3.2 Pricing and product strategies

- 3.3.1 Impact on trade

- 3.4 Price trend

- 3.4.1 Region

- 3.4.2 Product

- 3.5 Cost breakdown analysis

- 3.6 Profit margin analysis

- 3.7 Technology & innovation landscape

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising global automotive production

- 3.10.1.2 Technological advancements in steering systems

- 3.10.1.3 Emphasis on vehicle safety and regulatory compliance

- 3.10.1.4 Growth in electric and autonomous vehicles

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Disruption from electric and autonomous vehicle technologies

- 3.10.2.2 Fluctuating raw material prices and supply chain disruptions

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034, ($Bn, Units)

- 5.1 Key trends

- 5.2 Inner tie rods

- 5.3 Outer tie rods

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021-2034, ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicle (LCV)

- 6.3.2 Medium commercial vehicle (MCV)

- 6.3.3 Heavy commercial vehicle (HCV)

Chapter 7 Market Estimates & Forecast, By Material, 2021-2034, ($Bn, Units)

- 7.1 Key trends

- 7.2 Carbon steel

- 7.3 Stainless steel

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021-2034, ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ACDelco

- 10.2 APA Industries

- 10.3 BorgWarner

- 10.4 Bosch Group

- 10.5 Crown Automotive Sales

- 10.6 CTR

- 10.7 Delphi Technologies

- 10.8 Dorman Products

- 10.9 First Line

- 10.10 HL Mando

- 10.11 Ingalls Engineering

- 10.12 JTEKT

- 10.13 Mando

- 10.14 Moog

- 10.15 Motorcraft

- 10.16 Nexteer Automotive Group Limited

- 10.17 NSK

- 10.18 Sankei Industry

- 10.19 Synergy Manufacturing

- 10.20 ZF Friedrichshafen