|

시장보고서

상품코드

1740819

항공기 컴포넌트 MRO 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Aircraft Component MRO Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

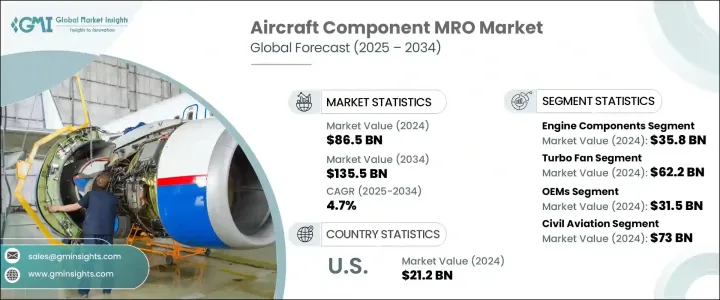

세계의 항공기 컴포넌트 MRO 시장은 2024년 865억 달러로 평가되었으며 국제 항공 운송량의 급증과 세계 항공기 보유수의 확대로 CAGR 4.7%로 성장하여 2034년까지 1,355억 달러에 이를 것으로 예측되고 있습니다.

민간항공이 회복되어 여행 수요가 급증하는 가운데 항공사는 운항 효율, 규제 준수, 승객의 안전을 확보하기 위해 MRO 서비스에 대한 투자를 강화하고 있습니다. 다양화되고 기술적으로 고도화되는 가운데, MRO 공급자는 최첨단 진단 도구, 예지 보전 기술, 첨단 재료 수리 기술을 활용하여 새로운 과제에 적응하고 있습니다. 시스템을 탑재한 연비효율이 높은 항공기에 대한 기호의 고조는 시장 전망을 재구성하고 있습니다. 경쟁이 격화되는 가운데, 운항회사는 보다 신속한 턴어라운드 타임, 보다 고도의 기술적 전문지식, 비용 효율적인 솔루션을 요구하고 있으며, MRO 기업은 능력의 확대, 디지털화에 대한 투자, 보다 스마트한 서비스 모델의 채용으로 우위에 서고 있습니다.

항공사는 운항의 안전 기준과 진화하는 규제의 의무에 대응하기 위해 MRO 서비스에 많은 투자를 실시했습니다. 차세대 엔진과 통합된 전자 시스템을 특징으로 하는 최신 항공기는 보다 고급 기술 전문 지식을 요구하고 있으며 전문 MRO 서비스에 대한 세계 수요에 더욱 박차를 가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 865억 달러 |

| 예측 금액 | 1,355억 달러 |

| CAGR | 4.7% |

세계 무역 정책의 변화는 MRO 사업자에게 추가적인 장애물을 가져오고 있습니다. 주요 항공 부품에 대한 수입 관세의 도입은 특히 미국에 기반을 둔 공급자에게 운영 비용을 증가시키고 있습니다. 이로 인해 항공사는 조달 전략과 유지 보수 계획을 검토해야합니다. 동시에 항공사는 규제에 대한 완벽한 준수를 보장하면서 비용 효율성을 높일 필요가 있습니다.

엔진 부품 부문은 2024년에 358억 달러를 창출하여 항공기 컴포넌트 MRO 시장을 독점했습니다. 차열 코팅, 플라즈마 용사, 레이저 클래딩과 같은 고급 수리 프로세스가 필요합니다.

항공기 유형별로 터보 팬 엔진 분야는 2024년에 622억 달러를 창출했습니다. 고압 터빈이나 팬블레이드와 같은 중요한 모듈에 대해 고정밀 레이저 드릴링 및 특수 보호 코팅이 종종 발생합니다.

미국 항공기 컴포넌트 MRO 시장은 견조한 국내 항공 산업에 힘입어 2024년에는 212억 달러에 이르렀습니다. 전략적 근대화 노력과 FAA 규제는 특히 엔진과 어비오닉스와 같은 중요한 시스템에 대한 MRO 능력의 발전을 촉진하고 있습니다.

항공기 컴포넌트 MRO 업계의 유명한 기업은 General Electric Company, AAR, Lufthansa Technik, ST Engineering, SIA Engineering Company 등이 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 항공기 컴포넌트에 대한 관세의 영향 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측에 대한 영향

- 가격 변동

- 공급 체인 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향

- 최종 시장에의 가격 전달

- 소비자의 반응 패턴

- 공급측에 대한 영향

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 항공 여행 수요 증가

- 항공 당국의 규제 명령

- MRO 업무를 타사 제공업체에게 아웃소싱

- 저비용 항공사의 세계 사업 확대

- 예측보수기술 도입 확대

- 업계의 잠재적 위험 및 과제

- 부품 수리 비용이 높고 복잡

- 숙련된 MRO 기술자의 세계 부족

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 컴포넌트 유형별, 2021-2034년

- 주요 동향

- 엔진 부품

- 항공전자기기

- 착륙장치

- 기체 부품

- 전기 시스템

- 유압 시스템

- 공압 시스템

- 연료 시스템

- 기타

제6장 시장 추계 및 예측 : 기종별, 2021-2034년

- 주요 동향

- 터보 프롭

- 터보 샤프트

- 터보 제트

- 터보 팬

- 내로우 바디

- 와이드 바디

- 지역 제트

- 기타

제7장 시장 추계 및 예측 : 서비스 제공업체 유형별, 2021-2034년

- 주요 동향

- OEM

- 항공사(사내 MRO)

- 타사 MRO 공급자(독립)

- 군사 MRO 유닛

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 민간항공

- 군사항공

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Lufthansa Technik

- General Electric Company

- ST Engineering

- SIA Engineering Company

- AAR

- AFI KLM E&M

- MTU Aero Engines AG

- Hong Kong Aircraft Engineering Company Limited.

- Delta Air Lines, Inc.

- Pratt &Whitney

- Rolls-Royce plc

- Ameco

- Turkish Technic Inc.

- Guangzhou Aircraft Maintenance Engineering Co.,Ltd.

- SR Technics Switzerland Ltd.

- AFI KLM E&M

- TAP.

- AJ Walter Aviation Limited

- Aero Norway AS

- StandardAero

The Global Aircraft Component MRO Market was valued at USD 86.5 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 135.5 billion by 2034, driven by the surge in international air traffic and the expanding global fleet of aircraft. As commercial aviation recovers and travel demand skyrockets, airlines are ramping up investments in maintenance, repair, and overhaul services to ensure operational efficiency, regulatory compliance, and passenger safety. With fleets becoming increasingly diverse and technologically advanced, MRO providers are adapting to new challenges by leveraging cutting-edge diagnostic tools, predictive maintenance technologies, and advanced material repair techniques. The rising preference for fuel-efficient aircraft, equipped with next-generation engines and integrated systems, is reshaping the market landscape. As competition intensifies, operators are seeking faster turnaround times, greater technical expertise, and cost-effective solutions, pushing MRO firms to expand capabilities, invest in digitalization, and adopt smarter service models to stay ahead.

Airlines are heavily investing in MRO services to meet operational safety standards and evolving regulatory mandates. Increasing complexity in aircraft systems, particularly in avionics and propulsion components, is pushing MRO procedures toward the adoption of digital tools, smart diagnostics, and predictive maintenance technologies. Modern fleets featuring next-generation engines and integrated electronic systems demand a higher degree of technical expertise, further fueling the global demand for specialized MRO services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $86.5 Billion |

| Forecast Value | $135.5 Billion |

| CAGR | 4.7% |

Shifting global trade policies are creating additional hurdles for MRO operators. The introduction of import tariffs on key aviation parts has elevated operational costs, especially for U.S.-based providers. These tariffs are disrupting established supply chains and raising serious concerns over component availability, compelling airlines to rethink procurement strategies and maintenance planning. At the same time, carriers are under mounting pressure to enhance cost-efficiency while ensuring full regulatory compliance, driving greater reliance on long-term service agreements and the expansion of in-house component repair capabilities.

The engine component segment generated USD 35.8 billion in 2024, dominating the aircraft component MRO market. This leadership comes from the critical importance and high replacement cost of engine parts, which require meticulous servicing and strict overhaul schedules. Components like combustors, turbine blades, and fuel nozzles endure extreme thermal and mechanical stress, necessitating advanced repair processes including thermal barrier coatings, plasma spraying, and laser cladding. The integration of smart maintenance technologies such as digital twins and AI-driven diagnostics is revolutionizing traditional MRO workflows, helping providers predict wear patterns, minimize downtime, and significantly extend component lifespans.

By aircraft type, the turbofan engines segment generated USD 62.2 billion in 2024. Turbofan engines' complex design and superior thrust efficiency make them essential across both commercial and military aviation sectors. Maintenance procedures for these engines often involve high-precision laser drilling and specialized protective coatings for critical modules like high-pressure turbines and fan blades. As the aviation industry pushes for quieter and more fuel-efficient aircraft, MRO service providers are scaling their operations to meet the needs of new-generation engines made with composite materials and geared architectures.

The U.S. Aircraft Component MRO Market reached USD 21.2 billion in 2024, supported by a robust domestic aviation industry. Hosting one of the world's largest commercial aircraft fleets, the U.S. boasts a dense network of certified repair stations and OEM-aligned facilities across key aviation hubs. Strategic modernization efforts and FAA regulations are driving advancements in MRO capabilities, especially for critical systems like engines and avionics. Digital recordkeeping, sustainability compliance, and integrated maintenance tracking are now central to U.S. MRO operations.

Prominent players in the aircraft component MRO industry include General Electric Company, AAR, Lufthansa Technik, ST Engineering, and SIA Engineering Company. Leading firms are expanding global networks, investing in digital maintenance tools, and enhancing vertically integrated service models. Long-term partnerships with airlines and OEMs, focus on sustainable repair technologies, and upskilling of technical teams remain key strategies to strengthen service reliability and align with evolving aviation industry trends.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs impact analysis on aircraft components

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-Side impact

- 3.2.1.3.1.1 Price volatility

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-Side impact

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Consumer response patterns

- 3.2.1.3.1 Supply-Side impact

- 3.2.1.4 Key Companies impacted

- 3.2.1.5 Strategic industry responses

- 3.2.1.5.1 Supply chain reconfiguration

- 3.2.1.5.2 Pricing and product strategies

- 3.2.1.5.3 Policy engagement

- 3.2.1.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand for air travel

- 3.3.1.2 Regulatory mandates from aviation authorities

- 3.3.1.3 Outsourcing MRO activities to third-party providers

- 3.3.1.4 Expansion of low-cost carrier operations globally

- 3.3.1.5 Increasing adoption of predictive maintenance technologies

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost and complexity of component repairs

- 3.3.2.2 Shortage of skilled MRO technicians globally

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Component Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Engine components

- 5.3 Avionics

- 5.4 Landing gear

- 5.5 Airframe components

- 5.6 Electrical systems

- 5.7 Hydraulic systems

- 5.8 Pneumatic systems

- 5.9 Fuel systems

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Aircraft Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Turboprops

- 6.3 Turbo shafts

- 6.4 Turbo jet

- 6.5 Turbo fan

- 6.5.1 Narrow-body

- 6.5.2 Wide-body

- 6.5.3 Regional jets

- 6.5.4 Others

Chapter 7 Market Estimates & Forecast, By Service Provider Type, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 OEMs

- 7.3 Airlines (In-house MRO)

- 7.4 Third-Party MRO Providers (Independent)

- 7.5 Military MRO Units

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Civil aviation

- 8.3 Military aviation

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Lufthansa Technik

- 10.2 General Electric Company

- 10.3 ST Engineering

- 10.4 SIA Engineering Company

- 10.5 AAR

- 10.6 AFI KLM E&M

- 10.7 MTU Aero Engines AG

- 10.8 Hong Kong Aircraft Engineering Company Limited.

- 10.9 Delta Air Lines, Inc.

- 10.10 Pratt & Whitney

- 10.11 Rolls-Royce plc

- 10.12 Ameco

- 10.13 Turkish Technic Inc.

- 10.14 Guangzhou Aircraft Maintenance Engineering Co.,Ltd.

- 10.15 SR Technics Switzerland Ltd.

- 10.16 AFI KLM E&M

- 10.17 TAP.

- 10.18 A J Walter Aviation Limited

- 10.19 Aero Norway AS

- 10.20 StandardAero