|

시장보고서

상품코드

1740829

전기자동차 배터리 냉각 플레이트 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Electric Vehicle Battery Cooling Plate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

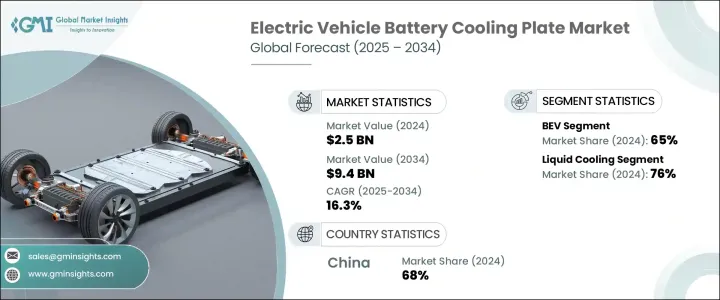

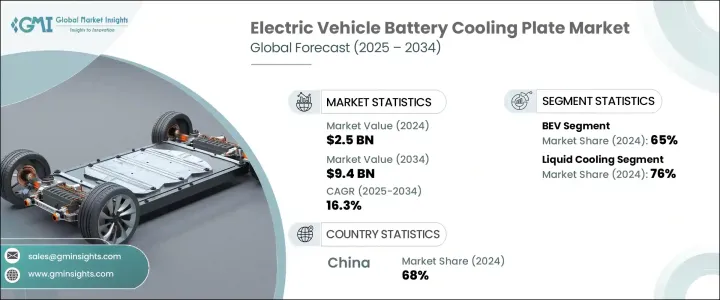

세계의 전기자동차 배터리 냉각 플레이트 시장은 2024년 25억 달러로 평가되었고, 전동 이동성으로의 이동 가속화, 세계 배출 규제 강화, EV 생산을 지원하는 정부의 인센티브, 적극적인 탈탄소화 목표가 원동력이 되어 CAGR 16.3%로 성장해 2034년까지 94억 달러에 달할 것으로 보입니다.

전기자동차의 보급이 주류가 됨에 따라, 고효율의 열 관리 시스템 수요가 급증하고 있습니다.

EV 생태계의 성숙에 따라 열 관리 솔루션은 더 이상 단순한 옵션이 아니며 경쟁력있는 항속 거리, 배터리 내구성 및 소비자 신뢰를 달성하는 데 필수적입니다. 네트워크의 확대는 자동차 제조업체나 배터리 제조업체가 고도의 냉각 기술에 다액의 투자를 실시하는 것을 더욱 뒷받침하고 있습니다. 또한, 차량의 경량화와 스페이스 최적화의 추진에 의해 컴팩트하고 고효율인 배터리 냉각 설계의 기술 혁신이 진행되어, 차세대 EV 플랫폼에 불가결한 것이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 25억 달러 |

| 예측 금액 | 94억 달러 |

| CAGR | 16.3% |

세계 정부는 EV 기술, 특히 배터리 열 관리 시스템의 진보에 중요한 역할을 하고 있습니다. 항속거리를 늘리는 데 도움이 되는 액냉 배터리 플레이트와 같은 첨단 냉각 시스템의 개발을 향한 경우가 많습니다.

전기자동차 배터리 냉각 플레이트 시장은 차량 유형별로 BEV, PHEV, HEV로 구분됩니다. 내연 기관이 없기 때문에 최적의 성능과 배터리 수명을 보장하기 위해 뛰어난 열 관리 시스템이 요구되고 있습니다.

기술별로 시장은 공냉, 액냉, PCM 냉각으로 구분됩니다.

2024년 세계 시장은 중국이 68%의 점유율을 차지했고 약 8억 4,000만 달러의 수익을 올려 리드하고 있습니다.

세계 전기자동차 배터리 냉각 플레이트 시장의 유력 기업은 Sanhua Group, Boyd, BorgWarner, Modine Manufacturing Company, Nippon Light Metal, Dana, Senior Flexonics, MAHLE, Sogefi Group, Valeo 등이 있습니다. 이러한 기업은 액냉 기술의 혁신, 제품 포트폴리오의 확대, 자동차 제조업체와의 제휴, 환경 친화적인 소재의 탐구, 정부 기관과의 제휴 등, 시장에서의 존재감을 높이고, 세계의 지속가능성의 동향에 대응하기 위해서 다액의 투자를 실시했습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 부품 제조업체

- 배터리 제조업체

- 원재료 공급자

- 부품 공급자

- 애프터마켓 서비스 제공업체

- 도매업체

- 최종 용도

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 무역에 미치는 영향

- 이익률 분석

- 기술과 혁신의 상황

- 특허 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 전기자동차의 보급 증가

- 배터리 냉각 기술의 진보

- 정부 인센티브와 정책

- 급속 충전 수요 증가

- 업계의 잠재적 위험 및 과제

- 제조 비용이 높아

- 복잡한 설계 통합

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 차량별, 2021-2034년

- 주요 동향

- 전기자동차

- PHEV

- 하이브리드 자동차

제6장 시장 추계 및 예측 : 기술별, 2021-2034년

- 주요 동향

- 액체

- 공기

- PCM

제7장 시장 추계 및 예측 : 재료별, 2021-2034년

- 주요 동향

- 알루미늄

- 구리

- 스테인레스 스틸

제8장 시장 추계 및 예측 : 판매채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- Aavid Thermalloy

- Alfa Laval

- Boyd

- BorgWarner

- CapTherm Systems

- Dana

- Granges

- Koolance

- MAHLE

- Modine Manufacturing Company

- Nemak

- Nippon Light Metal

- Samsung SDI

- Sanhua Holding Group

- Senior Flexonics

- SGL Carbon SE

- Sogefi

- Valeo

- Zhejiang Yinlun Machinery

The Global Electric Vehicle Battery Cooling Plate Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 16.3% to reach USD 9.4 billion by 2034, driven by the accelerating shift toward electric mobility, stricter global emission regulations, government incentives supporting EV production, and aggressive decarbonization goals. As electric vehicle adoption becomes mainstream, the demand for highly efficient thermal management systems is surging. With EV batteries becoming more powerful and complex, maintaining optimal temperatures has become critical for performance, safety, and battery lifespan. Cooling plates, especially liquid-cooled systems, have emerged as essential components in battery packs to handle high thermal loads during fast charging and heavy usage.

As the EV ecosystem matures, thermal management solutions are no longer just optional add-ons but integral to achieving competitive vehicle range, battery durability, and consumer trust. Growing consumer awareness about EV safety, the rising popularity of long-range electric models, and the expansion of fast-charging networks worldwide are further pushing automakers and battery manufacturers to invest heavily in advanced cooling technologies. Additionally, the push for vehicle lightweighting and space optimization has led to innovations in compact, high-efficiency battery cooling designs, making them indispensable in next-gen EV platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $9.4 Billion |

| CAGR | 16.3% |

Governments across the world are playing a crucial role in advancing EV technologies, particularly in battery thermal management systems. By making substantial investments in research and development, countries are fueling innovations aimed at enhancing the performance, safety, and energy efficiency of EVs. Funding initiatives are frequently directed toward the development of advanced cooling systems like liquid-cooled battery plates, which help optimize battery health and extend driving range. Through financial incentives and subsidies for manufacturers and research institutions, governments are fast-tracking the development of more efficient cooling solutions essential for the rapid expansion of the EV market.

The electric vehicle battery cooling plate market is segmented by vehicle type into BEV, PHEV, and HEV. In 2024, BEVs accounted for a dominant 65% share and are expected to expand at a CAGR of 17.1% through 2034. Since BEVs rely entirely on electric batteries and lack internal combustion engines, they demand superior thermal management systems to ensure optimal performance and battery longevity. The surging growth of BEVs, supported by tightening emission regulations and increasing consumer interest, is driving significant demand for advanced cooling solutions.

By technology, the market is segmented into air cooling, liquid cooling, and PCM cooling. Liquid cooling captured a commanding 76% share in 2024 and is set to maintain dominance due to its superior ability to manage high thermal loads. Liquid-cooled systems offer better temperature control than air cooling, enabling faster charging and longer battery life, making them the preferred choice for long-range, high-performance EVs.

China led the global market in 2024 with a 68% share, generating around USD 840 million in revenue. Its leadership is fueled by robust EV manufacturing capabilities, strong battery production infrastructure, and proactive government policies promoting electric mobility.

Prominent players in the Global Electric Vehicle Battery Cooling Plate Market include Sanhua Group, Boyd, BorgWarner, Modine Manufacturing Company, Nippon Light Metal, Dana, Senior Flexonics, MAHLE, Sogefi Group, and Valeo. These companies are heavily investing in innovations around liquid cooling technologies, expanding product portfolios, collaborating with automakers, exploring eco-friendly materials, and forming partnerships with government bodies to strengthen their market presence and align with global sustainability trends.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component manufacturers

- 3.2.2 Battery manufacturers

- 3.2.3 Raw material supplier

- 3.2.4 Component supplier

- 3.2.5 Aftermarket service provider

- 3.2.6 Distributor

- 3.2.7 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (selling price)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Strategic industry responses

- 3.3.3.1 Supply chain reconfiguration

- 3.3.3.2 Pricing and product strategies

- 3.3.1 Impact on trade

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising adoption of electric vehicles

- 3.9.1.2 Advancements in battery cooling technology

- 3.9.1.3 Government incentives and policies

- 3.9.1.4 Rising demand for fast charging

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High manufacturing cost

- 3.9.2.2 Complex design integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 BEV

- 5.3 PHEV

- 5.4 HEV

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Liquid

- 6.3 Air

- 6.4 PCM

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Aluminium

- 7.3 Copper

- 7.4 Stainless steel

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Aavid Thermalloy

- 10.2 Alfa Laval

- 10.3 Boyd

- 10.4 BorgWarner

- 10.5 CapTherm Systems

- 10.6 Dana

- 10.7 Granges

- 10.8 Koolance

- 10.9 MAHLE

- 10.10 Modine Manufacturing Company

- 10.11 Nemak

- 10.12 Nippon Light Metal

- 10.13 Samsung SDI

- 10.14 Sanhua Holding Group

- 10.15 Senior Flexonics

- 10.16 SGL Carbon SE

- 10.17 Sogefi

- 10.18 Valeo

- 10.19 Zhejiang Yinlun Machinery