|

시장보고서

상품코드

1740831

주사기 및 주사제 포장 시장 : 기회, 촉진요인, 업계 동향 분석, 예측(2025-2034년)Syringes and Injectable Drugs Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

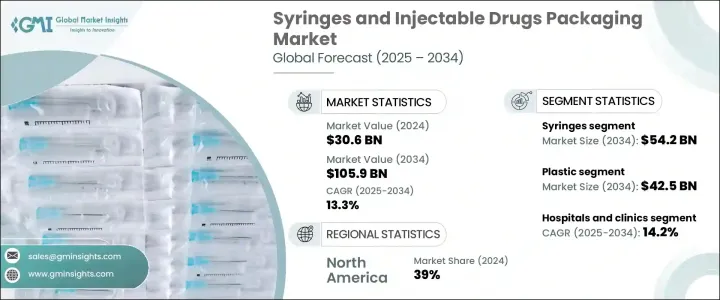

세계의 주사기 및 주사제 포장 시장은 2024년에 306억 달러로 평가되었으며, 특히 만성 질환과 감염증의 증례가 증가하는 가운데 주사요법에 대한 수요 증가에 견인되어 CAGR 13.3%로 성장해 2034년까지 1,059억 달러에 이를 것으로 추정되고 있습니다.

헬스케어 업계에서는 즉각적이고 정확한 투여가 가능한 약물전달로의 이동이 급속히 진행되고 있습니다. 이 이동은 의약품 포장의 전망을 재구성하고 제조업체에 혁신과 진화하는 의료 요구에 적응하도록 촉구합니다. 낮은 침습 치료의 급증, 생물 제제의 확대, 자가 투여 약물에 대한 선호도 증가는 고급 패키징 시스템의 중요한 역할을 강화하고 있습니다. 제약회사가 주사제 포트폴리오를 지속적으로 확대하고 있는 가운데 무균성, 사용 용이성, 규제 준수를 보장하는 패키징에 대한 수요는 그 어느 때보다 긴급성을 늘리고 있습니다. 또한 세계의 건강 위기와 인구의 고령화로 인해 특히 응급, 외래 및 재택치료 현장에서 효과적이고 안전하며 확장 가능한 약물전달에 대한 요구가 더욱 커지고 있습니다.

특히 외래 및 응급의료에서는 신속한 약물 투여를 위해 주사제의 사용이 증가하고 있으며, 약물의 무결성과 환자의 안전성을 유지하는 안전하고 무균 포장에 대한 요구가 증가하고 있습니다. 주사기 및 주사제 포장이 엄격한 안전 기준을 충족하는지 확인하는 것은 오염을 방지하고, 약물의 안정성을 유지하며, 임상 현장의 의료 규정을 준수하는 데 필수적입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 306억 달러 |

| 예측 금액 | 1,059억 달러 |

| CAGR | 13.3% |

급속한 성장에도 불구하고 시장은 주목할만한 과제에 직면하고 있습니다. 업계 각 회사는 원재료를 비축하고 단계적인 정책 전환을 추진함으로써 대응하고 있지만, 품질이나 비용 효율을 떨어뜨리지 않고 수요 증가에 대응하려고 하는 제조업체에 있어서, 공급 체인의 혼란은 여전히 큰 장애물이 되고 있습니다.

제품 유형별로 보면 시장은 주사기 및 주사제에 맞춘 포장 형태로 구분됩니다. 주사기만으로도 2034년까지 542억 달러의 매출이 전망되고 있습니다.

소재별로는 플라스틱, 유리, 기타 특수 기판이 시장에 포함됩니다. 플라스틱은 경량으로 깨지기 어렵고, 가격도 적당한 것으로부터, 2034년 시장 규모는 425억 달러로 추정되어 리드할 것으로 예측되고 있습니다.

북미는 2024년에 39% 시장 점유율을 차지해 강력한 의약품 제조 인프라와 선진적인 헬스 케어 시스템 덕분에, 계속 우위를 유지하고 있습니다.

Nipro Europe Group Companies, Gerresheimer, West Pharmaceutical Services, Inc., Schott AG, BD등의 주요 기업은 연구개발에 대한 투자, 제조 거점의 확대, 생산 라인의 자동화, 전략적 파트너십의 구축을 실시해, 제품의 안전성의 향상, 생산 효율의 향상, 세계 시장에서의 규제 준수를 유지하기 위해 노력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 주사 약물전달 수요 증가

- 소비자용 백신 및 기타 의약품의 성장

- 포장에 있어서의 기술의 진보

- 지속가능성과 환경에 대한 압력

- 인구 고령화와 세계의 헬스케어 액세스 확대

- 업계의 잠재적 위험 및 과제

- 디바이스의 호환성과 약제의 안정성의 문제

- 원재료 공급의 제약

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 주사기

- 프리필드 주사기

- 기존 주사기

- 주사제

- 바이알

- 앰풀

- 카트리지

- 병

제6장 시장 추계 및 예측 : 재질별, 2021-2034년

- 주요 동향

- 플라스틱

- 폴리프로필렌(PP)

- 폴리에틸렌(PE)

- 폴리카보네이트(PC)

- 기타

- 유리

- 기타

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원 및 진료소

- 외래수술센터(ASC)

- 제약 및 바이오테크놀러지 기업

- 재택 헬스케어 환경

- 백신 접종 센터

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- BD

- AptarGroup, Inc.

- Bormioli Pharma SpA

- Catalent, Inc

- Credence MedSystems, Inc.

- DWK Life Sciences.

- Gerresheimer

- J.Penner Corporation

- Laboratorios Farmaceuticos Rovi SA

- Nipro Europe Group Companies

- Schott AG

- SGD Pharma

- Shandong Province Medicinal Glass Co., Ltd.

- Stevanato Group

- Terumo Europe NV

- USIN Advance Co.,Ltd.

- Weigao Group

- West Pharmaceutical Services, Inc.

The Global Syringes and Injectable Drugs Packaging Market was valued at USD 30.6 billion in 2024 and is estimated to grow at a CAGR of 13.3% to reach USD 105.9 billion by 2034, driven by the rising demand for injectable therapies, especially amid increasing cases of chronic and infectious diseases. The healthcare industry is experiencing a rapid shift toward injectable drug delivery due to its ability to provide fast-acting relief and precise dosing. This shift is reshaping the pharmaceutical packaging landscape, pushing manufacturers to innovate and adapt to evolving medical needs. The surge in minimally invasive treatments, expansion of biologics, and growing preference for self-administered drugs are reinforcing the critical role of advanced packaging systems. As pharmaceutical companies continue to expand their injectable portfolios, the demand for packaging that ensures sterility, ease of use, and regulatory compliance is becoming more urgent than ever. Moreover, global health crises and aging populations are further intensifying the need for effective, safe, and scalable drug delivery solutions, particularly in emergency, ambulatory, and home-based care settings.

The increasing use of injectables for quick drug administration, especially in outpatient and emergency care, has created a heightened need for secure, sterile packaging that upholds drug integrity and patient safety. Ensuring the packaging of syringes and injectable drugs meets strict safety standards is essential to prevent contamination, maintain drug stability, and comply with healthcare regulations across clinical settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.6 Billion |

| Forecast Value | $105.9 Billion |

| CAGR | 13.3% |

Despite its rapid growth, the market is facing notable challenges. Shifting trade policies and tariffs on medical components are complicating pricing structures and limiting product availability. Recent tariff hikes on imported materials have driven up manufacturing costs, especially for sterile injectables and low-cost therapies where affordability is critical. Industry players are responding by stockpiling raw materials and pushing for phased policy shifts, but supply chain disruptions remain a significant hurdle for manufacturers aiming to meet rising demand without compromising quality or cost-efficiency.

Based on product type, the market is segmented into syringes and packaging formats tailored to injectable drugs. Syringes alone are expected to generate USD 54.2 billion by 2034 as hospitals, clinics, and home care settings increasingly adopt pre-sterilized, tamper-evident solutions to reduce contamination risks and enhance drug delivery safety. The expanding use of injectable therapies across vaccines, diabetes, and autoimmune diseases is also driving the adoption of single-use, safety-enhanced syringe systems.

In terms of material, the market includes plastic, glass, and other specialized substrates. Plastic is projected to lead with an estimated market size of USD 42.5 billion by 2034 due to its lightweight, break-resistant, and affordable properties. Plastic is the material of choice for prefilled syringes and self-injection devices, supporting designs with integrated safety features like retractable needles and dose-tracking systems.

North America held a 39% market share in 2024 and continues to dominate, thanks to its strong pharmaceutical manufacturing infrastructure and advanced healthcare systems. The demand for prefilled and disposable injectable packaging is rising fast as hospitals and home care providers seek to reduce infection rates and streamline drug administration.

Leading companies, including Nipro Europe Group Companies, Gerresheimer, West Pharmaceutical Services, Inc., Schott AG, and BD, are investing in R&D, expanding manufacturing footprints, automating production lines, and building strategic partnerships to improve product safety, boost production efficiency, and maintain regulatory compliance across global markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increased demand for injectable drug delivery

- 3.3.1.2 Growth in consumer vaccination and other drugs

- 3.3.1.3 Technological advancements in packaging

- 3.3.1.4 Sustainability and environmental pressures

- 3.3.1.5 Aging population and increasing global healthcare access

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Device compatibility and drug stability issues

- 3.3.2.2 Raw material supply constraints

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Syringes

- 5.2.1 Prefilled syringes

- 5.2.2 Conventional syringes

- 5.3 Injectable drugs packaging

- 5.3.1 Vials

- 5.3.2 Ampoules

- 5.3.3 Cartridges

- 5.3.4 Bottles

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Plastic

- 6.2.1 Polypropylene (PP)

- 6.2.2 Polyethylene (PE)

- 6.2.3 Polycarbonate (PC)

- 6.2.4 Others

- 6.3 Glass

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers (ASCs)

- 7.4 Pharmaceutical & biotechnology companies

- 7.5 Home healthcare settings

- 7.6 Vaccination centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BD

- 9.2 AptarGroup, Inc.

- 9.3 Bormioli Pharma S.p.A.

- 9.4 Catalent, Inc

- 9.5 Credence MedSystems, Inc.

- 9.6 DWK Life Sciences.

- 9.7 Gerresheimer

- 9.8 J.Penner Corporation

- 9.9 Laboratorios Farmaceuticos Rovi S.A.

- 9.10 Nipro Europe Group Companies

- 9.11 Schott AG

- 9.12 SGD Pharma

- 9.13 Shandong Province Medicinal Glass Co., Ltd.

- 9.14 Stevanato Group

- 9.15 Terumo Europe NV

- 9.16 USIN Advance Co., Ltd.

- 9.17 Weigao Group

- 9.18 West Pharmaceutical Services, Inc.