|

시장보고서

상품코드

1740860

제설차 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Snow Clearing Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

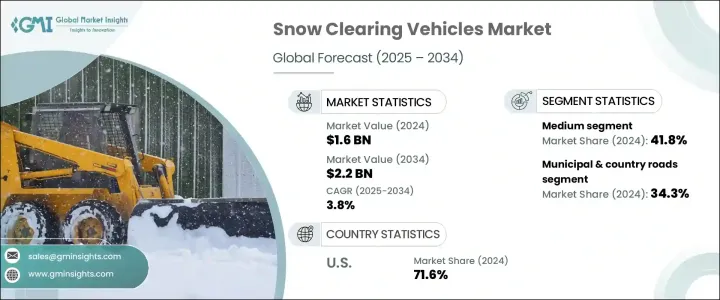

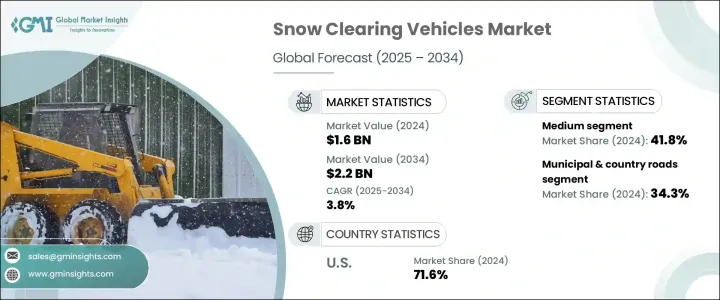

세계의 제설차 시장 규모는 2024년에 16억 달러에 달했고, CAGR 3.8%를 나타내 2034년에는 22억 달러에 이를 것으로 예측되고 있습니다.

이 성장은 공항 인프라의 지속적인 개발과 폭설에 휩쓸리기 쉬운 다양한 지역의 도로 교통망의 꾸준한 증가가 큰 요인이 되고 있습니다. 공항의 업그레이드와 확장에 따라, 특히 한랭지에서는 고성능 제설차 수요가 계속 증가하고 있습니다. 효율적인 제설 장비는 가혹한 겨울 상황에서 중단없는 서비스를 유지하는 데 필수적입니다. 시장은 또한 스마트 인프라로의 광범위한 변화를 보고 있으며, 시정촌과 서비스 제공업체는 안전성과 효율성을 모두 높이는 고도로 안정적인 제설 기술을 선호합니다. 지속가능성, 연료 효율성, 낮은 유지보수 솔루션에 대한 관심 증가는 도시와 농촌 모두에서 제설 작업을 관리하는 방식에 변화를 가져왔습니다.

용도별로 시장 세분화는 공항, 고속도로, 도로 및 국도 및 기타 용도의 네 가지 주요 부문으로 나뉩니다. 2024년에는 시정촌과 시골길 부문이 약 34.3% 시장 점유율로 1위를 차지했으며 예측 기간 동안 CAGR 3.5% 이상을 나타낼 것으로 예측됩니다. 이 부문은 지역 특유의 조건에 맞게 제설 기술을 적응시키고 규모를 확장하는 능력이 있기 때문에 매우 중요합니다. 지방정부는 내부식성 부품, 모듈식 시스템, 고급 제빙 기술을 갖춘 다기능 차량에 자주 투자하고 있습니다. 이러한 맞춤설정은 원격지나 액세스가 어려운 지역이나 악천후의 영향을 자주 받는 지역에서도 일관된 성능을 제공하는 데 도움이 됩니다. 지자체의 노선이나 시골길의 제설 작업에서는 험한 지형, 비포장의 노면, 좁은 길 등을 이동하는 경우가 자주 있습니다. 이로 인해 가혹한 환경 조건 하에서의 격렬한 작업에도 대응할 수 있는 다관절 블레이드, 강화 서스펜션, 전지형 대응 타이어 등의 견고한 하드웨어를 갖춘 차량 수요가 높아지고 있습니다. 도시와 마을이 보다 똑똑한 눈 관리 방법을 채택함에 따라 지속가능성과 효과를 향상시키기 위해 GPS 가이드가 포함된 제설 시스템, 자동 소금 뿌리기 기능, 하이브리드 추진 옵션을 갖춘 장비에 대한 관심이 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 16억 달러 |

| 예측 금액 | 22억 달러 |

| CAGR | 3.8% |

시장은 또한 차종별로 소형차, 중형차, 대형차로 구분됩니다. 또한 정확한 제설이 필요한 환경에서도 효율적으로 작동합니다. 많은 모델이 준비되어 있는 이러한 차량은 구매자가 지형, 강설 수준, 필요한 조종성에 따라 기기를 선택할 수 있게 되어 있습니다.

추진력 유형별로 분류하면 시장에는 내연기관차(ICE), 전기자동차, 하이브리드차가 포함됩니다. 제설차나 살포기와 같은 무게가 있는 제설기기를 운전할 때의 성능으로, 오퍼레이터에게 지지되고 있습니다.

지역별로는 미국이 2024년 제설차 시장을 선도해 약 5억 달러를 창출했고 북미 전체 점유율의 약 71.6%를 차지했습니다. 이는 제설 솔루션에 대한 일관된 강한 수요를 창출하고 있습니다. 확립된 공급망과 지속적인 기술의 발전으로 미국은 제설차과 장비의 주요 시장입니다.

업계가 계속 진화하는 동안 제조업체는 제설차의 소재와 기술을 향상시킨 디자인에 힘을 쏟고 있습니다. 경화강, 경량 합금, 고급 복합재 등의 고성능 부품은 극단적인 날씨와 가혹한 환경에서의 조종성을 높이고, 연료 소비량을 줄이고, 구조 내구성을 향상시키기 위해 점점 통합되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 부품 공급자

- 제조업체

- 기술 공급자

- 서비스 제공업체

- 유통 채널

- 최종 용도

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(고객에 대한 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 이익률 분석

- 기술과 혁신의 상황

- 특허 분석

- 주요 뉴스와 대처

- 규제 상황

- 가격 분석

- 추진

- 지역

- 영향요인

- 성장 촉진요인

- 이상 기상 빈도 증가

- 공항 인프라 확장

- 도시화와 지자체의 투자

- 도로 수송망의 성장

- 업계의 잠재적 위험 및 과제

- 높은 자본 비용과 유지비

- 환경규제와 연비기준

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 공항

- 고속도로

- 지방도 및 시골도로

- 기타

제6장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 소형

- 중형

- 대형

제7장 시장 추계·예측 : 추진력별(2021-2034년)

- 주요 동향

- ICE

- 전기

- 하이브리드

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 정부 및 지방자치단체

- 민간 계약자

- 농업 부문

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- Aebi Schmidt Holding

- Alamo

- Boschung Holding

- Caterpillar

- Daimler(Mercedes-Benz Trucks)

- Doosan Bobcat

- Faymonville

- Hako Group

- John Deere

- Kassbohrer Gelandefahrzeug

- Kodiak America

- MB Companies

- Montana Manufacturing

- Oshkosh

- Rosenbauer International

- Schmidt Group

- Swarco

- Ventrac

- Wausau Equipment Company

- Zoomlion

The Global Snow Clearing Vehicles Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 3.8% to reach USD 2.2 billion by 2034. This growth is largely fueled by the ongoing development of airport infrastructure and the steady rise in road transportation networks across various regions prone to heavy snowfall. As airports upgrade and expand, especially in colder areas, the demand for high-performance snow removal vehicles continues to grow. Efficient snow clearing equipment is essential to maintaining uninterrupted services during severe winter conditions. The market is also seeing a broader shift toward smart infrastructure, where municipalities and service providers are prioritizing advanced and reliable snow clearing technologies that enhance both safety and efficiency. A growing focus on sustainability, fuel efficiency, and low-maintenance solutions is transforming how snow removal operations are managed in both urban and rural settings.

In terms of application, the snow clearing vehicles market is divided into four main segments: airports, highways, municipal and country roads, and other uses. In 2024, the municipal and country roads segment took the lead with an approximate 34.3% market share and is projected to grow at over 3.5% CAGR throughout the forecast period. This segment is pivotal due to its ability to adapt and scale snow clearing technologies to suit unique regional conditions. Local governments frequently invest in multi-functional vehicles equipped with corrosion-resistant parts, modular systems, and advanced de-icing technology. These customizations help deliver consistent performance even in areas that are remote, hard to reach, or frequently impacted by adverse weather. Clearing snow from municipal routes and country roads often involves navigating steep terrain, unpaved surfaces, and narrow paths. This has led to a growing demand for vehicles built with rugged hardware like articulated blades, reinforced suspensions, and all-terrain tires that can handle intense workloads under harsh environmental conditions. As cities and towns adopt smarter snow management practices, there is a growing interest in equipment with GPS-guided plow systems, automated salting features, and hybrid propulsion options to improve both sustainability and effectiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 3.8% |

The market is also segmented by vehicle type into compact, medium, and heavy vehicles. The medium vehicle segment emerged as the largest in 2024, accounting for approximately 41.8% of the market, and is expected to grow at a CAGR of over 4.3% through 2034. These vehicles play a critical role in snow clearing operations, particularly in urban areas and large commercial zones. Their balance of power and size allows them to operate efficiently in environments that require frequent and precise snow removal. Available in numerous models, these vehicles allow purchasers to select equipment based on terrain, snowfall levels and required maneuverability. Buyers now benefit from greater transparency in pricing, which includes optional features and attachments, making it easier for municipalities and contractors to invest wisely within limited budgets.

When classified by propulsion type, the market includes internal combustion engine (ICE), electric, and hybrid-powered vehicles. ICE vehicles remain the dominant choice in 2024 due to their proven ability to deliver high torque, consistent reliability, and long operational endurance in freezing and rugged conditions. These vehicles are favored by operators for their performance in driving heavy snow removal equipment such as plows and spreaders. Although ICE-based systems are still the most common, there's a gradual shift toward enhancing them with modern fuel management systems, low-emission technology, and navigation features to meet evolving performance and environmental standards.

Regionally, the United States led the snow clearing vehicles market in 2024, generating around USD 500 million and holding nearly 71.6% of the total share in North America. The country's diverse winter climate and emphasis on maintaining road safety during snow events have created a strong and consistent demand for snow clearing solutions. A well-established supply chain, coupled with ongoing technological advancements, has allowed the U.S. to remain a leading market for snow clearing vehicles and equipment.

As the industry continues to evolve, manufacturers are focusing on designing snow clearing vehicles with improved materials and technology. Reinforced hydraulics, corrosion-resistant surfaces, and high-torque drive systems are becoming standard. These updates not only extend vehicle life but also ensure top-tier performance in demanding winter operations. High-performance components such as hardened steel, lightweight alloys, and advanced composites are being increasingly integrated to boost maneuverability, reduce fuel consumption, and enhance structural durability in extreme weather and challenging landscapes.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component Suppliers

- 3.2.3 Manufacturers

- 3.2.4 Technology Providers

- 3.2.5 Service Providers

- 3.2.6 Distribution channel

- 3.2.7 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing analysis

- 3.9.1 Propulsion

- 3.9.2 Region

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing frequency of extreme weather events

- 3.10.1.2 Expansion of airport infrastructure

- 3.10.1.3 Urbanization and municipal investments

- 3.10.1.4 Growth in road transportation networks

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High capital and maintenance costs

- 3.10.2.2 Environmental regulations and fuel efficiency standards

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Airports

- 5.3 Highways

- 5.4 Municipal & country roads

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Compact

- 6.3 Medium

- 6.4 Heavy

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Government & municipalities

- 8.3 Private contractor

- 8.4 Agricultural sector

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Aebi Schmidt Holding

- 10.2 Alamo

- 10.3 Boschung Holding

- 10.4 Caterpillar

- 10.5 Daimler (Mercedes-Benz Trucks)

- 10.6 Doosan Bobcat

- 10.7 Faymonville

- 10.8 Hako Group

- 10.9 John Deere

- 10.10 Kassbohrer Gelandefahrzeug

- 10.11 Kodiak America

- 10.12 M-B Companies

- 10.13 Montana Manufacturing

- 10.14 Oshkosh

- 10.15 Rosenbauer International

- 10.16 Schmidt Group

- 10.17 Swarco

- 10.18 Ventrac

- 10.19 Wausau Equipment Company

- 10.20 Zoomlion