|

시장보고서

상품코드

1740890

우유 포장 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Milk Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

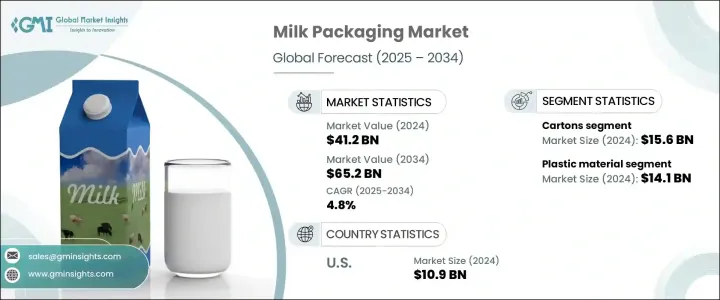

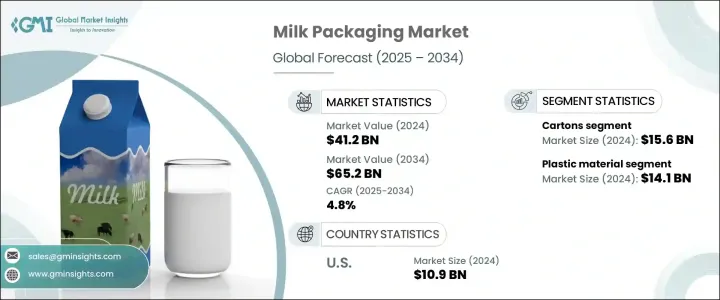

세계의 우유 포장 시장은 2024년에는 412억 달러에 달했고, CAGR 4.8%를 나타내 2034년에는 652억 달러에 이를 것으로 추정됩니다.

이 시장은 유제품 소비 증가, 조직 소매업의 급성장, 전자상거래의 폭발적 확대에 의해 강력한 기세를 보여주고 있습니다. 드 인지도를 높이고 소비자의 관심을 높이는 포장에 대한 요구는 지금까지 없을 정도로 높아지고 있습니다.

지속가능하고 가볍고 재활용하기 쉬운 소재에 대한 수요가 증가함에 따라 경쟁 구도를 재구성하고 있으며 포장는 더 이상 비용 요인이 아니라 전략적 브랜드 자산으로 간주됩니다. 식품의 안전성, 추적성, 원재료의 원산지에 대한 의식이 높아짐에 따라 포장의 역할이 더욱 향상되고 있습니다. 이 시프트는 또한 QR 코드와 스마트 라벨과 같은 기능을 제공하여 소비자가 더 나은 정보를 기반으로 선택할 수 있도록 하는 스마트 포장 기술의 기회를 만들어 냅니다. 소매업체와 전자상거래 플랫폼이 시각적으로 매력적이고 기능적이며 환경 친화적인 포장을 추구하기 때문에 테트라팩과 친환경 판지와 같은 형태가 온라인과 오프라인 채널 모두에서 널리 지원됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 412억 달러 |

| 예측 금액 | 652억 달러 |

| CAGR | 4.8% |

우유 포장 시장은 포장 유형별로 병, 카톤, 파우치, 캔, 그 밖에 구분됩니다. 카톤은 공간 효율도 높고, 운송 비용과 배출량을 삭감하고, 종래의 플라스틱를 대체하는 환경 친화적인 선택이 되고 있습니다.

시장은 소재별로, 플라스틱, 유리, 금속, 판지, 기타에 구분됩니다.소재별로는 플라스틱이 우세하고, 2024년 시장 규모는 141억 달러였습니다. 리시러블 캡이나 인체공학에 근거한 디자인 등의 유저의 편리성을 높여 부패를 최소한으로 억제합니다.

2024년 독일의 우유 포장 시장 규모는 23억 달러였으며, 이는 강력한 규제 기준과 재활용 가능하고 생분해성이 있는 포장에 대한 소비자의 기호 증가를 반영합니다.

세계 시장의 주요 기업으로는 Tetra Pak, SIG, Smurfit Kappa, WestRock, Sonoco Products, Elopak, Ecolean, Berry Global, CDF Corporation, Alfipa 등이 있습니다. 경쟁력을 유지하기 위해 이러한 기업은 지속 가능한 포장 혁신에 많은 투자를하고 있으며, 생분해성 복합재, 재활용 가능한 판지, 전자상거래 물류에 맞춘 솔루션 연구 개발의 초점은 유통 기한의 연장, 환경 실적의 삭감, 유기 유제품 및 고급 유제품 등 틈새 시장을 위한 커스터마이징 포장의 제공이며, 최종적으로는 브랜드 로얄티의 강화에 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 유제품 소비량 증가

- 조직화된 소매업 및 전자상거래 확대

- 식물 유래의 대체 우유의 인기 증가

- 편리하고 사용하기 쉬운 포장 수요

- 포장 기술의 진보

- 업계의 잠재적 위험 및 과제

- 환경 문제와 규제 압력

- 원재료 가격 변동

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 포장 형태별(2021-2034년)

- 주요 동향

- 병

- 카톤

- 파우치

- 캔

- 기타

제6장 시장 추계·예측 : 재료별(2021-2034년)

- 주요 동향

- 유리

- 플라스틱

- 금속

- 판지

- 기타

제7장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주 및 뉴질랜드

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제8장 기업 프로파일

- Alfipa

- Berry Global

- CDF Corporation

- CKS Packaging

- Ecolean

- Elopak

- Global Polybags Industries

- IPI

- Jagannath Polymers

- 일본 Paper Industries

- Parksons Packaging

- SIG

- Smurfit Kappa

- Sonoco Products

- Stanpac

- Stora Enso

- Tetra Pak

- WestRock

The Global Milk Packaging Market was valued at USD 41.2 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 65.2 billion by 2034. The market is witnessing strong momentum driven by rising dairy product consumption, rapid growth in organized retail, and the explosive expansion of e-commerce. As consumers increasingly opt for online shopping for fresh and packaged dairy goods, packaging is evolving to meet new standards of durability, leak resistance, and ease of transport. The need for packaging that ensures product safety while enhancing brand visibility and consumer engagement is now at an all-time high. In a consumer-driven environment where preferences revolve around convenience, sustainability, and transparency, packaging plays a critical role in shaping purchasing decisions. Companies are investing in innovative packaging formats that can stand out on physical shelves and in digital storefronts alike.

The growing demand for sustainable, lightweight, and easily recyclable materials is reshaping the competitive landscape, with packaging no longer seen as a cost factor but as a strategic brand asset. Increasing awareness around food safety, traceability, and the origin of ingredients further elevates the role of packaging. This shift has also created opportunities for smart packaging technologies, offering features such as QR codes and smart labels that empower consumers to make better-informed choices. As retailers and e-commerce platforms seek packaging that is visually appealing, functional, and environmentally responsible, formats like tetra packs and eco-friendly cartons are gaining widespread traction across both online and offline channels.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $41.2 Billion |

| Forecast Value | $65.2 Billion |

| CAGR | 4.8% |

The milk packaging market is segmented by packaging type into bottles, cartons, pouches, cans, and others. The cartons segment remains the largest, valued at USD 15.6 billion in 2024. Its growth is fueled by rising consumer demand for aseptic packaging solutions that extend shelf life while utilizing sustainable materials such as renewable paperboard. Cartons are also space-efficient, cutting down on transportation costs and emissions, making them a greener alternative to traditional plastic options. They are especially preferred for premium and value-added milk products like lactose-free and fortified milk, where strong light and oxygen barrier properties are critical.

Based on material, the market is segmented into plastic, glass, metal, paperboard, and others. Plastic dominates the material segment, with a market value of USD 14.1 billion in 2024. Materials like HDPE and PET remain top choices for their lightweight structure, impact resistance, and superior ease of handling across long-distance logistics and e-commerce distribution. Features such as resealable caps and ergonomic designs enhance user convenience and minimize spoilage. A growing focus on recycling is pushing manufacturers toward using recycled plastics (rPET), addressing environmental concerns while maintaining functionality.

Germany Milk Packaging Market was valued at USD 2.3 billion in 2024, reflecting strong regulatory standards and heightened consumer preference for recyclable and biodegradable packaging. The growing trend of organic dairy consumption further drives demand for premium, sustainable packaging solutions. Technological innovations such as smart labels and enhanced barrier materials are making a tangible impact on shelf life and traceability.

Key players in the global market include Tetra Pak, SIG, Smurfit Kappa, WestRock, Sonoco Products, Elopak, Ecolean, Berry Global, CDF Corporation, and Alfipa. To stay competitive, these companies are heavily investing in sustainable packaging innovations, developing biodegradable composites, recyclable paperboards, and solutions tailored for e-commerce logistics. Research and development efforts are focused on extending shelf life, reducing environmental footprint, and offering customized packaging for niche markets such as organic and premium dairy segments, ultimately strengthening brand loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (Raw Materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (Selling Price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (Raw Materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing consumption of dairy products

- 3.3.1.2 Expansion of organized retail and e-commerce

- 3.3.1.3 Rising popularity of plant-based milk alternatives

- 3.3.1.4 Demand for convenient and user-friendly packaging

- 3.3.1.5 Advancements in packaging technology

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Environmental concerns and regulatory pressures

- 3.3.2.2 Fluctuating raw material prices

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Packaging Type, 2021 – 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Bottles

- 5.3 Cartons

- 5.4 Pouches

- 5.5 Cans

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Glass

- 6.3 Plastic

- 6.4 Metal

- 6.5 Paperboard

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 ANZ

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 Middle East and Africa

- 7.6.1 UAE

- 7.6.2 Saudi Arabia

- 7.6.3 South Africa

Chapter 8 Company Profiles

- 8.1 Alfipa

- 8.2 Berry Global

- 8.3 CDF Corporation

- 8.4 CKS Packaging

- 8.5 Ecolean

- 8.6 Elopak

- 8.7 Global Polybags Industries

- 8.8 IPI

- 8.9 Jagannath Polymers

- 8.10 Nippon Paper Industries

- 8.11 Parksons Packaging

- 8.12 SIG

- 8.13 Smurfit Kappa

- 8.14 Sonoco Products

- 8.15 Stanpac

- 8.16 Stora Enso

- 8.17 Tetra Pak

- 8.18 WestRock