|

시장보고서

상품코드

1740899

플렉서블 보호 포장 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Flexible Protective Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

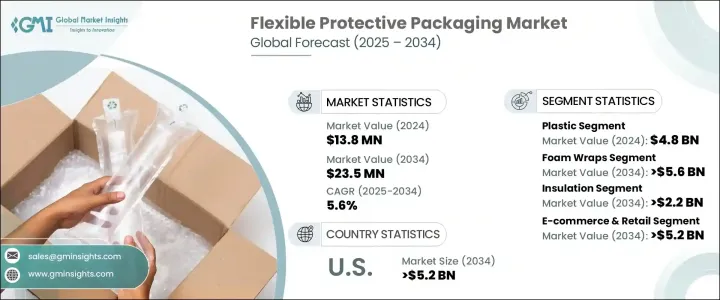

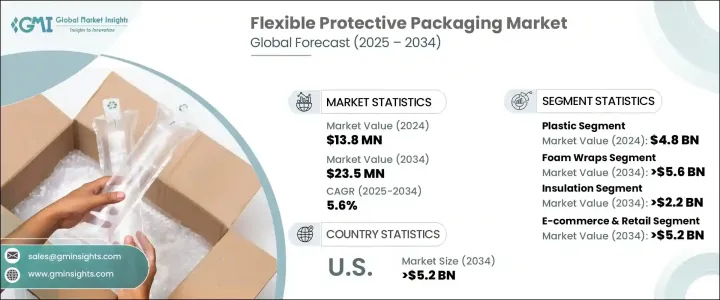

세계의 플렉서블 보호 포장 시장은 2024년에는 138억 달러로 평가되었으며, 전자상거래 분야의 확대와 라스트마일 배송 네트워크의 진보로 CAGR 5.6%를 나타내 2034년에는 235억 달러에 이를 것으로 예측되고 있습니다.

세계 산업이 비용 효율적이고 높은 제품 보호를 제공하는 가볍고 내구성이 뛰어나고 지속 가능한 대체 포장에 기울기 때문에 시장은 급속한 변화를 경험하고 있습니다. 제품의 보관, 배송, 배송 방법이 변화하고 운송중의 상품을 완충할 뿐만 아니라 다양한 제품의 형상과 크기에 용이하게 적응하는 포장에 대한 요구가 높아지고 있습니다. 보다 신속한 배송을 요구하고 있으며 플렉서블 보호 포장은 성능과 지속가능성의 균형을 추구하는 기업에게 선호되는 솔루션입니다. 케이지의 혁신은 꾸준히 진행되고 있으며, 브랜드는 규제 기준과 소비자의 기대에 부응하고 있습니다.

플라스틱 폐기물 감소와 환경 친화적인 관행 추진에 대한 규제 압력 증가는 시장의 주요 성장 촉매가 되고 있습니다. 급증에 따라 보호성과 경제성을 겸비한 포장에 대한 수요가 가속하고 있습니다. 보다 적은 재료 소비로 강력한 완충성을 제공하기 위해 인기를 모으고 있습니다. 공간 절약이라는 특성은 물류 비용을 낮추는 것뿐만 아니라 운송시의 이산화탄소 배출량의 삭감에도 공헌하고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 138억 달러 |

| 예측 금액 | 235억 달러 |

| CAGR | 5.6% |

미국 이전의 통상 정권 하에서 도입된 지속적인 관세 정책은 수입 원재료에 의존하는 국내 제조업체에 비용 압력을 가했습니다. 이를 통해 제조업체는 비용 효율성을 최적화하면서 탄력성을 높이고 있습니다. 경쟁 구도에서 경쟁력이 중요합니다.

재료의 유형 중에서 플라스틱은 계속 플렉서블 보호 포장 분야를 지배하고 있으며, 2024년에는 48억 달러를 기록했습니다. 이러한 재료는 에어 베개, 발포 인서트, 쁘띠 쁘띠 등의 포장 솔루션에 널리 사용되고 있으며, 장거리 수송 중 깨지기 쉬운 물품의 보호에 필수적입니다.

폼랩 분야는 2034년까지 56억 달러를 창출할 것으로 예측되고 있으며, 플렉서블 보호 포장에서 가장 급성장하고 있는 분야 중 하나가 되고 있습니다. 불규칙한 형상에도 피트하기 위해, 부피가 커지지 않고 완충성을 유지할 수 있습니다.

미국에서는 강력한 전자상거래 에코시스템과 지속가능한 포장을 중시하는 국가의 고조에 힘입어 플렉서블 보호 포장 시장은 2034년까지 52억 달러를 창출할 것으로 예측되고 있습니다. 수요를 충족시키기 위해 생분해성 랩, 종이 기반 완충재 및 재활용 가능한 폴리메일러를 신속하게 채택하고 있습니다.

경쟁력을 유지하기 위해 Amcor, Smurfit Kappa, Mondi, Sealed Air, Pregis 등의 업계 선두는 연구개발, 지속가능성 혁신, 커스터마이즈된 포장 시스템에 많은 투자를 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전자상거래 확대

- 지속가능성과 규제 준수

- 비용과 운영 효율

- 재료과학의 진보

- 가전제품과 신선식품의 성장

- 업계의 잠재적 위험 및 과제

- 재활용 인프라의 갭

- 원재료 가격 변동

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 재료 유형별(2021-2034년)

- 플라스틱

- 종이 및 판지

- 폼

- 알루미늄 포일

제6장 시장 추계·예측 : 제품 유형별(2021-2034년)

- 에어 쿠션

- 버블 랩

- 폼 랩

- 메일러

- 수축 랩

- 스트레치 필름

- 기타

제7장 시장 추계·예측 : 기능별(2021-2034년)

- Void Fill

- 블로킹 및 브레이싱

- 래핑

- 단연

- 쿠션

- 표면 보호

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 전자상거래 및 소매

- 식품 및 음료

- 의약품 및 헬스케어

- 소비자

- 자동차

- 산업

- 기타

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Sealed Air Corporation

- Pregis LLC

- Smurfit Kappa Group

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Sonoco Products Company

- ProAmpac LLC

- Storopack Hans Reichenecker GmbH

- DS Smith Plc

- Winpak Ltd.

- Mondi Flexible Packaging

- Rengo Co.Ltd.

- AptarGroup, Inc.

- Toray Plastics(America), Inc.

- Schur Flexibles Group

The Global Flexible Protective Packaging Market was valued at USD 13.8 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 23.5 billion by 2034, driven by the expanding e-commerce sector and advancements in last-mile delivery networks. The market is experiencing a rapid shift as industries across the globe lean toward lightweight, durable, and sustainable packaging alternatives that offer cost-efficiency and high product protection. The growing penetration of online shopping platforms has transformed how goods are stored, shipped, and delivered-fueling a strong need for packaging that not only cushions items in transit but also adapts easily to varying product shapes and sizes. Consumers are demanding faster deliveries with minimal environmental impact, making flexible protective packaging a preferred solution for businesses looking to strike a balance between performance and sustainability. Innovations in recyclable, compostable, and biodegradable packaging are emerging at a steady pace, helping brands meet regulatory benchmarks and consumer expectations alike. As retailers prioritize omnichannel fulfillment, flexible packaging is offering a strategic advantage-reducing shipping weights, limiting waste, and enhancing overall operational agility.

Rising regulatory pressure on reducing plastic waste and promoting eco-friendly practices has become a key growth catalyst for the market. Many businesses are proactively shifting from rigid, heavy-duty formats to smarter, flexible options that can be easily customized and shipped at lower costs. Across emerging economies-especially in Asia-Pacific-these trends are even more pronounced, where the spike in online retail activity is accelerating demand for packaging that is both protective and economical. Flexible protective packaging formats such as bubble wraps, foam inserts, padded mailers, and air pillows are gaining traction because they offer strong cushioning with less material consumption. Their space-saving nature not only drives down logistics costs but also helps reduce carbon emissions during transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.8 billion |

| Forecast Value | $23.5 billion |

| CAGR | 5.6% |

Ongoing tariff policies introduced during earlier U.S. trade administrations have added cost pressures on domestic manufacturers relying on imported raw materials. These tariffs have prompted companies to rethink their supply chains, leading to a shift in sourcing strategies and investments in regional manufacturing hubs. In doing so, manufacturers are enhancing their resilience while optimizing cost-efficiency. Flexible protective packaging plays a vital role in this landscape-it helps reduce material usage, lowers dimensional shipping costs, and allows easy scalability across product lines, giving businesses a competitive edge in an evolving market.

Among material types, plastic continues to dominate the flexible protective packaging space, generating USD 4.8 billion in 2024. Common plastic resins such as polyethylene, polypropylene, and polystyrene remain popular due to their low cost, durability, and high impact resistance. These materials are extensively used in packaging solutions like air pillows, foam inserts, and bubble wraps, which are essential for protecting fragile items during long-haul shipments. With the rise of digital retail, particularly in sectors like consumer electronics and cosmetics, the demand for these lightweight, high-performance materials shows no signs of slowing down.

The foam wraps segment is projected to generate USD 5.6 billion by 2034, making it one of the fastest-growing areas in flexible protective packaging. Foam wraps are widely used due to their lightweight nature and strong cushioning properties, which are ideal for safeguarding delicate items during transit. These wraps effortlessly mold to irregular shapes, ensuring that items remain securely cushioned without adding excessive bulk. Industries handling precision equipment-such as medical devices, electronics, and luxury glassware-are increasingly depending on foam wraps to reduce the risk of breakage, returns, and customer dissatisfaction.

In the U.S., the flexible protective packaging market is forecasted to generate USD 5.2 billion by 2034, fueled by a strong e-commerce ecosystem and the nation's growing emphasis on sustainable packaging. As online shopping habits intensify, businesses are rapidly adopting biodegradable wraps, paper-based cushioning, and recyclable poly mailers to meet demand across industries such as food, pharmaceuticals, and consumer goods. These sectors require packaging solutions that not only protect product integrity but also align with eco-conscious values and compliance requirements.

To maintain a competitive edge, industry leaders like Amcor, Smurfit Kappa, Mondi, Sealed Air, and Pregis are heavily investing in R&D, sustainability innovation, and customized packaging systems. They are also expanding their regional manufacturing footprint to better serve omnichannel retail models and address complex logistics demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 E-commerce expansion

- 3.3.1.2 Sustainability and regulatory compliance

- 3.3.1.3 Cost and operational efficiency

- 3.3.1.4 Advancements in material science

- 3.3.1.5 Growth in consumer electronics and perishables

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Recycling infrastructure gaps

- 3.3.2.2 Volatility in raw material prices

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Million and Units)

- 5.1 Plastic

- 5.2 Paper & paperboard

- 5.3 Foam

- 5.4 Aluminum foil

Chapter 6 Market estimates & forecast, By Product Type, 2021 - 2034 (USD Billion and Units)

- 6.1 Air cushions

- 6.2 Bubble wraps

- 6.3 Foam wraps

- 6.4 Mailers

- 6.5 Shrink wraps

- 6.6 Stretch films

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Function, 2021 - 2034 (USD Billion and Units)

- 7.1 Void Fill

- 7.2 Blocking & bracing

- 7.3 Wrapping

- 7.4 Insulation

- 7.5 Cushioning

- 7.6 Surface protection

Chapter 8 Market estimates & forecast, By End Use, 2021 - 2034 (USD Billion and Units)

- 8.1 E-commerce & retail

- 8.2 Food & beverages

- 8.3 Pharmaceuticals & healthcare

- 8.4 Consumer

- 8.5 Automotive

- 8.6 Industrial

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion and Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Sealed Air Corporation

- 10.2 Pregis LLC

- 10.3 Smurfit Kappa Group

- 10.4 Amcor plc

- 10.5 Mondi Group

- 10.6 Huhtamaki Oyj

- 10.7 Sonoco Products Company

- 10.8 ProAmpac LLC

- 10.9 Storopack Hans Reichenecker GmbH

- 10.10 DS Smith Plc

- 10.11 Winpak Ltd.

- 10.12 Mondi Flexible Packaging

- 10.13 Rengo Co., Ltd.

- 10.14 AptarGroup, Inc.

- 10.15 Toray Plastics (America), Inc.

- 10.16 Schur Flexibles Group