|

시장보고서

상품코드

1740908

열가소성 접착 필름 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Thermoplastic Adhesive Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

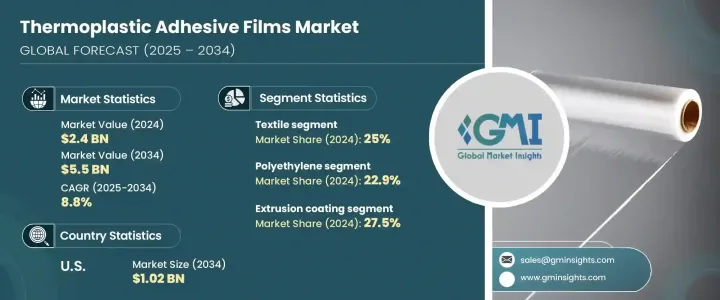

세계의 열가소성 접착 필름 시장은 2024년에는 24억 달러로 평가되었고 2034년에는 55억 달러에 이를 것으로 추정되며, CAGR 8.8%로 성장할 전망입니다.

이러한 상승 추세는 여러 최종 사용 산업, 특히 자동차 및 전자 제품 제조 분야에서 경량 소재에 대한 선호도가 높아짐에 따라 크게 촉진되고 있습니다. 열가소성 접착 필름은 전체 제품 무게를 크게 줄이면서 부품을 접착하는 데 점점 더 많이 사용되고 있습니다. 연비 목표를 지원하고 배기가스 배출량 감소에 기여하는 열가소성 접착 필름은 전 세계적으로 강화되는 환경 규제 및 지속 가능성 벤치마크와도 잘 부합합니다.

소형 전자제품과 웨어러블 기기에서 이 필름은 뛰어난 내열성을 제공하며, 이는 소형 고밀도 제품 설계에서 성능을 유지하는 데 필수적인 요소입니다. 스마트폰, 플렉서블 기기, 차세대 소비자 기기 등 공간 제약이 있는 용도에서 깔끔한 처리와 안정적인 접착을 가능하게 합니다. 또한 의료 기술 분야는 생체 적합성, 내화학성, 손쉬운 멸균이 필수적인 잠재력이 높은 분야로 부상하고 있습니다. 이러한 필름은 다양한 의료용 웨어러블 및 일회용 의료 제품에 사용되며 내구성이 뛰어나면서도 비침습적인 접착력을 제공합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 24억 달러 |

| 예측 금액 | 55억 달러 |

| CAGR | 8.8% |

지속 가능성은 수요 형성의 중심 테마가 되고 있습니다. 열가소성 접착 필름은 무용제 특성과 재활용 가능성으로 인해 환경을 고려한 솔루션으로 인식되어 VOC 배출을 최소화하고자 하는 산업에 적합합니다. 제조업체들은 규제 프레임워크와 환경, 사회, 거버넌스(ESG) 목표에 부합하기 위해 환경 친화적인 접착 대체재를 점점 더 많이 채택하고 있습니다. 필름 주조 및 핫멜트 적용과 같은 가공 기술의 발전으로 접착 필름의 열 거동, 밀봉 능력 및 점착성이 개선되어 산업용 라미네이트 및 광학 시스템과 같이 높은 정밀도가 요구되는 분야에서 사용이 확대되고 있습니다.

재료별로 2024년 시장에는 폴리에틸렌, 폴리아미드, 열가소성 폴리우레탄, 폴리에스테르, 폴리프로필렌, 폴리올레핀 및 기타 재료 유형이 포함됩니다. 2024년 시장 규모는 24억 달러로, 2034년에는 크게 성장하여 55억 달러에 달할 것으로 예상됩니다. 이 중 폴리에틸렌은 2024년 전체 점유율의 22.9%를 차지했는데, 이는 주로 경제성, 유연성, 다양한 기질과 잘 결합하는 능력 덕분입니다. 폴리에틸렌은 포장 및 자동차와 같은 분야에서 사용되지만, 산업이 고급 성능 필름으로 전환함에 따라 성장률은 완만하게 유지되고 있습니다. 열가소성 폴리우레탄은 탄성, 투명성, 우수한 내마모성 덕분에 상당한 성장세를 보이고 있습니다. 소형화되고 유연한 부품에 대한 수요가 증가함에 따라 새로운 용도 전반에 걸쳐 채택이 증가하고 있습니다.

기술적인 관점에서 2024년 시장은 압출 코팅, 핫멜트 접착제, 수지 혼합, 필름 캐스팅, 기타 가공 기술로 구분됩니다. 강도가 안정되어 있기 때문에 전자나 위생 관련 제품을 중심으로 급속하게 확대하고 있습니다. 압출 코팅 방식은 고속 생산 능력과 다양한 기판에서 일관된 코팅 품질로 인해 27.5%의 시장 점유율로 이 부문을 주도하고 있습니다. 핫멜트 접착제는 용제를 사용하지 않고 환경 친화적인 특성과 신뢰할 수 있는 접착 강도로 인해 특히 전자 및 위생 관련 제품에서 빠르게 확대되고 있습니다. 레진 블렌딩은 점착력, 내열성 등 필름 특성을 맞춤화하는 데 유리하지만 복잡한 배합 요건과 생산 비용 상승으로 인해 제약이 있습니다. 필름 주조는 매끄럽고 결함 없는 필름이 필수적인 고정밀 환경, 특히 광학 및 의료용 용도에서 선호되고 있습니다.

2024년 시장을 최종 용도별로 분석하면 섬유, 자동차, 전기 및 전자, 의료, 탄도 보호, 건설 및 기타 부문으로 나뉩니다. 섬유 산업은 의류, 가정용 가구 및 스마트 섬유의 심리스 라미네이션에 대한 수요가 증가함에 따라 25%의 점유율로 선두를 달리고 있습니다. 접착 필름은 무용제 섬유 본딩 솔루션에서 핵심적인 역할을 하고 있습니다. 자동차 분야에서는 차량 경량화에 대한 요구와 소음, 진동 및 거칠기(NVH)를 완화해야 할 필요성으로 인해 이러한 필름의 중요성이 더욱 커지고 있습니다. 특히 건강 모니터링 장치와 진단 도구에 사용되는 피부 민감성 및 멸균 필름을 중심으로 의료 분야에서도 빠르게 발전하고 있습니다. 탄도 및 방위 분야에서는 보호 복합재의 레이어링 목적으로 고강도 필름을 활용합니다.

지역별로는 미국이 2024년 세계 시장에서 17.8%의 점유율을 차지하며, 그 시장 규모는 약 4억 3,000만 달러로, 2034년에는 10억 2,000만 달러로 성장할 것으로 예측되고 있습니다. 이러한 우위는 자동차, 항공우주, 의료, 전자 등 첨단 제조 부문에서 열가소성 접착 필름의 보급률이 높아진 데 기인합니다. 무용제 접착제에 대한 국가의 집중과 무역 규제 및 국내 소싱 전략의 조정을 포함한 지원 정책 환경이 현지 생산과 혁신을 촉진하고 있습니다.

이 업계의 경쟁을 견인하는 주요 기업은 다우, 3M, BASF SE, 헨켈 AG, 코베스트로 AG 등이 있으며, 각각 시장에서의 존재감을 높이기 위해 다른 접근법을 채택하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 공급자의 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 자동차 경량화 수요 증가

- 소비자 가전 및 웨어러블의 성장

- 의료기기 산업의 확장

- 지속 가능한 접착제에 대한 관심 증가

- 필름 캐스팅 및 핫멜트의 기술 발전

- 섬유 산업 혁신의 증가(예 : 스마트 섬유)

- 업계의 잠재적 위험 및 과제

- 높은 원자재 비용(예 : TPU, 폴리아미드)

- 열경화성 수지에 비해 제한된 내열성 및 내화학성

- 다층 구조의 복잡한 재활용성

- 성장 촉진요인

- 트럼프 정권의 관세 영향 - 구조화된 개요

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 폴리에틸렌

- 폴리아미드

- 열가소성 폴리우레탄

- 폴리에스테르

- 폴리프로필렌

- 폴리올렌

- 기타 재료

제6장 시장 추계 및 예측 : 테크놀로지별(2021-2034년)

- 주요 동향

- 압출 코팅

- 핫멜트 접착제

- 수지 혼합

- 필름 캐스팅

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 섬유

- 자동차

- 전기 및 전자공학

- 의료

- 탄도 보호

- 건설

- 기타 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- 3M Company

- Arkema SA

- Ashland Global

- Avery Dennison

- BASF SE

- Covestro AG

- Dow Inc.

- DuPont

- EMS-Chemie Holding AG

- HB Fuller

- Henkel AG

- Huntsman Corporation

- Mitsui Chemicals Inc.

- Sika AG

The Global Thermoplastic Adhesive Films Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 5.5 billion by 2034. This upward trend is largely fueled by the growing preference for lightweight materials across several end-use industries, especially in automotive and electronics manufacturing. Thermoplastic adhesive films are being increasingly used to bond components while significantly reducing overall product weight. Their ability to support fuel efficiency goals and contribute to reduced emissions aligns well with tightening environmental regulations and sustainability benchmarks globally.

In compact electronics and wearable devices, these films offer excellent thermal resistance, which is essential for maintaining performance in miniature, high-density product designs. They allow for clean processing and reliable bonding in space-constrained applications such as smartphones, flexible gadgets, and next-gen consumer devices. Additionally, the medical technology sector is emerging as a high-potential area, where biocompatibility, chemical resistance, and easy sterilization are vital. These films are used in a variety of medical wearables and disposable healthcare products, delivering durable yet non-invasive adhesion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.5 Billion |

| CAGR | 8.8% |

Sustainability is becoming a central theme in shaping demand. Thermoplastic adhesive films are seen as an eco-conscious solution due to their solvent-free nature and recyclability, making them suitable for industries seeking to minimize VOC emissions. Manufacturers are increasingly adopting environmentally friendly adhesive alternatives to align with regulatory frameworks and environmental, social, and governance (ESG) goals. Advances in processing technologies like film casting and hot melt applications have improved the thermal behavior, sealing ability, and tack properties of adhesive films, expanding their use in areas that demand high precision, such as industrial laminates and optical systems.

In terms of material segmentation, the market in 2024 includes polyethylene, polyamide, thermoplastic polyurethane, polyester, polypropylene, polyolefins, and other material types. With the market valued at USD 2.4 billion in 2024, it is forecast to grow substantially and reach USD 5.5 billion by 2034. Among these, polyethylene accounted for 22.9% of the total share in 2024, primarily due to its affordability, flexibility, and ability to bond well with various substrates. It is used in sectors like packaging and automotive, although its growth rate remains modest as industries shift toward more advanced performance films. Thermoplastic polyurethane is experiencing significant momentum thanks to its elasticity, transparency, and superior abrasion resistance. The growing need for miniaturized and flexible components is supporting its adoption across emerging applications.

From a technology standpoint, the 2024 market is segmented into extrusion coating, hot melt adhesives, resin blending, film casting, and other processing techniques. The extrusion coating method led the segment with a 27.5% market share due to its high-speed production capability and consistent coating quality across various substrates. Hot melt adhesives are expanding quickly, especially in electronics and hygiene-related products, driven by their solvent-free, environmentally sound properties and dependable bond strength. Resin blending, while advantageous for customizing film characteristics like tack and heat resistance, faces constraints due to complex formulation requirements and elevated production costs. Film casting is finding preference in high-precision environments where smooth, defect-free films are essential, particularly for optical and medical-grade applications.

When analyzed by end use in 2024, the market is divided into textiles, automotive, electrical and electronics, medical, ballistic protection, construction, and other sectors. The textile industry led with a 25% share, as demand rises for seamless lamination in garments, home furnishings, and smart textiles. Adhesive films are playing a key role in solvent-free textile bonding solutions. In the automotive domain, the push for lighter vehicles and the need to mitigate noise, vibration, and harshness (NVH) have reinforced the relevance of these films. Medical uses are also advancing rapidly, particularly in skin-sensitive and sterilizable films for health-monitoring devices and diagnostic tools. Ballistic and defense applications leverage high-strength films for layering purposes in protective composites.

Regionally, the United States held a 17.8% share in the global market in 2024, valued at approximately USD 430 million, and is projected to grow to USD 1.02 billion by 2034. This dominance is attributed to the increasing penetration of thermoplastic adhesive films in advanced manufacturing sectors like automotive, aerospace, medical, and electronics. The country's focus on solvent-free adhesives and its supportive policy environment, including adjustments in trade regulations and domestic sourcing strategies, are boosting local production and innovation.

Major players driving competition in the industry include companies like Dow Inc., 3M Company, BASF SE, Henkel AG, and Covestro AG, each adopting different approaches to strengthen their market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand in automotive lightweighting

- 3.6.1.2 Growth in consumer electronics and wearables

- 3.6.1.3 Expansion of the medical device industry

- 3.6.1.4 Increasing preference for sustainable adhesives

- 3.6.1.5 Technological advancements in film casting and hot melt

- 3.6.1.6 Rising textile industry innovations (e.g., smart textiles)

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High raw material costs (e.g., TPU, polyamide)

- 3.6.2.2 Limited heat and chemical resistance compared to thermosets

- 3.6.2.3 Complex recyclability of multi-layer structures

- 3.6.1 Growth drivers

- 3.7 Impact of trump administration tariffs – structured overview

- 3.7.1 Impact on trade

- 3.7.1.1 Trade volume disruptions

- 3.7.1.2 Retaliatory measures

- 3.7.2 Impact on the industry

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.2.1.1 Price volatility in key materials

- 3.7.2.1.2 Supply chain restructuring

- 3.7.2.1.3 Production cost implications

- 3.7.2.2 Demand-side impact (selling price)

- 3.7.2.2.1 Price transmission to end markets

- 3.7.2.2.2 Market share dynamics

- 3.7.2.2.3 Consumer response patterns

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.3 Key companies impacted

- 3.7.4 Strategic industry responses

- 3.7.4.1 Supply chain reconfiguration

- 3.7.4.2 Pricing and product strategies

- 3.7.4.3 Policy engagement

- 3.7.4.4 Outlook and future considerations

- 3.7.1 Impact on trade

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene

- 5.3 Polyamide

- 5.4 Thermoplastics polyurethane

- 5.5 Polyester

- 5.6 Polypropylene

- 5.7 Polyolens

- 5.8 Other materials

Chapter 6 Market Estimates and Forecast, By Technologies, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Extrusion coating

- 6.3 Hot melt adhesive

- 6.4 Resin blending

- 6.5 Film casting

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Textile

- 7.3 Automotive

- 7.4 Electrical and electronics

- 7.5 Medical

- 7.6 Ballistic protection

- 7.7 Construction

- 7.8 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 Arkema SA

- 9.3 Ashland Global

- 9.4 Avery Dennison

- 9.5 BASF SE

- 9.6 Covestro AG

- 9.7 Dow Inc.

- 9.8 DuPont

- 9.9 EMS-Chemie Holding AG

- 9.10 H.B. Fuller

- 9.11 Henkel AG

- 9.12 Huntsman Corporation

- 9.13 Mitsui Chemicals Inc.

- 9.14 Sika AG