|

시장보고서

상품코드

1740931

사이드 로더 쓰레기 수거차 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Side Loader Refuse Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

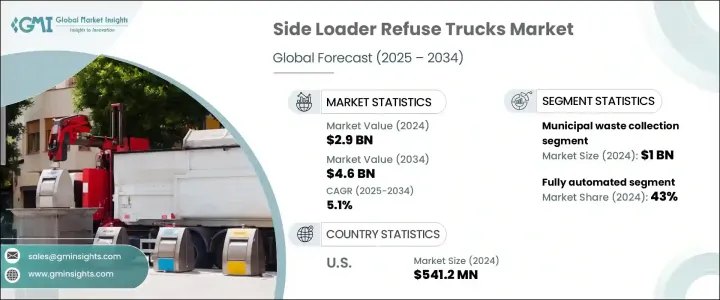

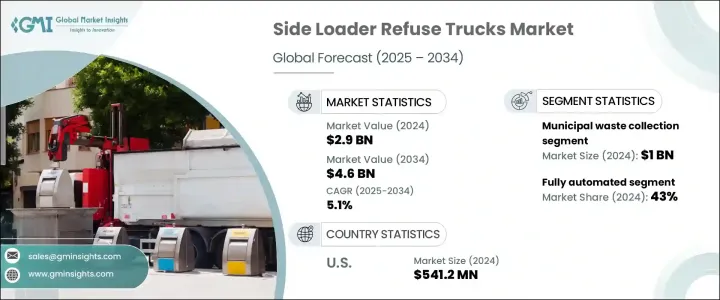

세계의 사이드 로더 쓰레기 수거차 시장은 2024년에는 29억 달러로 평가되었고, 2034년에는 46억 달러에 이를 것으로 추정되며, CAGR 5.1%로 성장할 전망입니다.

전 세계 도시가 계속 확장됨에 따라 효율적이고 공간을 절약하는 쓰레기 수거차에 대한 수요가 급증하고 있습니다. 도시 개발은 자연스럽게 인구 밀도를 높이고 고형 폐기물의 양을 증가시키므로 좁은 공간에서 폐기물 수거를 처리할 수 있는 시스템이 절실히 필요합니다. 사이드 로더 쓰레기 수거차는 좁은 도로와 번잡한 거리에서 기동할 수 있는 능력 덕분에 도시 지역에서 가장 적합한 솔루션이 되었습니다. 또한 표준화된 쓰레기통과의 호환성 덕분에 수거 프로세스를 간소화하려는 지자체에서 선호하는 옵션입니다. 도심은 더 깨끗하고 효율적인 폐기물 관리 방식을 지향하고 있으며, 이로 인해 사이드 로더 트럭의 도입이 크게 가속화되고 있습니다.

정부 규제 또한 이러한 차량의 채택이 늘어나는 데 중요한 역할을 하고 있습니다. 환경 및 안전 기준이 엄격해지면서 지방 당국과 민간 기업은 최신 저공해 기술에 투자하고 있습니다. 전기 및 하이브리드 시스템으로 구동되는 사이드 로더는 대기 질을 개선하고 탄소 배출을 줄이려는 도시의 목표에 따라 주목을 받고 있습니다. 이러한 차량은 환경 목표를 달성하는 데 도움이 될 뿐만 아니라 연료 소비를 줄이고 유지보수 시간을 단축하여 운영 성과를 개선합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 29억 달러 |

| 예측 금액 | 46억 달러 |

| CAGR | 5.1% |

용도별로 보면 시장은 산업 폐기물, 도시 폐기물, 상업 폐기물, 건설 및 철거 폐기물로 나뉩니다. 2024년에는 도시 폐기물 수거가 약 10억 달러의 시장 가치로 시장 점유율의 45% 이상을 차지하며 가장 큰 비중을 차지했습니다. 급속한 도시화로 인해 도시 지역에서 발생하는 폐기물은 계속 증가하고 있으며, 이러한 증가는 도시 수거 서비스에 대한 높은 수요로 반영되고 있습니다. 폐기물 양이 증가함에 따라 지자체는 위생 시스템에 대한 압력 증가를 처리하기 위해 사이드 로더 트럭으로 눈을 돌리고 있습니다.

이러한 트럭의 자동화된 설계는 인건비를 절감하고자 하는 도시 정부에 특히 유용하다는 것이 입증되었습니다. 사이드 로더는 자동화된 암과 쓰레기통을 들어올리는 메커니즘을 갖추고 있어 작업자 수가 적어 비용 효율성과 효율성이 뛰어납니다. 이 트럭은 사람의 개입을 최소화하면서 일관되고 중단 없이 쓰레기를 수거할 수 있어 인력 관리와 생산성 향상으로 이어집니다. 폐기물 관리 시스템의 효율성을 개선하기 위해 공공 자금이나 보조금을 지원받아 이러한 기술을 도입하는 도시 정부가 점점 더 많아지고 있습니다.

적재 메커니즘의 경우 시장은 완전 자동화, 반자동, 수동 시스템으로 세분화됩니다. 2024년에는 완전 자동화된 사이드 로더 트럭이 전체 점유율의 약 43%를 차지하며 시장을 주도할 것으로 예상됩니다. 이러한 트럭은 한 명의 운전자만으로 쓰레기통 들어올리기, 적재, 비우기 등 모든 핵심 기능을 수행할 수 있습니다. 이러한 자동화는 노동력을 줄일 뿐만 아니라 수거 프로세스의 속도를 높이고, 가동 중단 시간을 최소화하며, 정확도를 높입니다. 기술이 계속 발전함에 따라 이러한 완전 자동화된 시스템은 대도시 환경에서 더욱 안정적이고 필수적인 요소가 되고 있습니다.

연료 유형은 디젤, 전기, CNG, 하이브리드 및 기타 연료 유형이 혼합되어 있는 또 다른 중요한 세분화입니다. 2024년에는 디젤 구동 트럭이 시장을 주도할 것으로 예상됩니다. 대체 연료의 인기가 높아지고 있음에도 불구하고 디젤은 여전히 많은 지자체와 민간 사업자에게 가장 실용적이고 비용 효율적인 선택입니다. 디젤 트럭은 내구성이 뛰어나고 유지보수가 쉬우며 주유 인프라가 잘 구축되어 있는 것으로 유명합니다. 장거리 노선과 고강도 작업의 경우, 디젤은 전기 또는 CNG 동력 대체 연료에 비해 탁월한 신뢰성과 낮은 초기 비용을 제공합니다.

최종 사용자 측면에서 시장은 지자체 서비스, 전문 폐기물 처리업체, 민간 폐기물 관리 회사 등으로 세분화됩니다. 2024년에는 지자체 서비스가 선두를 차지할 것으로 예상됩니다. 지방 정부는 도시 지역, 특히 인구 밀도가 높은 지역에서 대부분의 폐기물 수거를 처리합니다. 사이드 로더 트럭은 컴팩트한 디자인과 자동화된 기능으로 이러한 지역에 효율적으로 서비스를 제공합니다. 정부 보조금과 예산 배정을 통해 지자체는 환경 목표를 지원하는 최신의 비용 효율적인 폐기물 수거 기술에 투자할 수 있는 유리한 위치에 있습니다.

지역적으로는 북미가 2024년 35% 이상의 점유율을 차지하며 시장의 대부분을 차지했습니다. 미국에서만 약 5억 4,120만 달러의 시장 가치를 기록했습니다. 미국의 높은 도시 인구와 엄격한 주 정부 차원의 규제로 인해 자동화되고 깨끗한 폐기물 수거 기술은 필수가 되었습니다. 폐기물 수거 당국은 배기가스 배출 의무를 준수하는 동시에 전반적인 운영 비용을 절감하기 위해 전기 및 하이브리드 모델에 대한 투자를 늘리고 있습니다.

이 분야의 주요 제조업체들은 스마트 자동화, 전기 드라이브 트레인, 진단 기능을 갖춘 모델을 제공하며 경쟁하면서 지속 가능성에 집중하고 있습니다. 저공해 또는 무공해 차량을 제공할 수 있는 기업들은 특히 북미와 유럽 등 친환경 조달 정책을 시행하는 지역에서 더 많은 기회를 찾고 있습니다. 경쟁력은 성능, 연비, 안전, 환경 규정 준수가 균형을 이루는 차량을 비용 효율적인 패키지로 제공하는 데 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원자재 및 부품 공급업체

- 트럭 및 기기 제조업체

- 기술 및 텔레매틱스 제공업체

- 최종 용도

- 이익률 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 기술과 혁신의 상황

- 특허 분석

- 가격 분석

- 지역

- 추진

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 도시화 및 인구 증가

- 깨끗하고 효율적인 폐기물 수거을 위한 규제 추진

- 민간 폐기물 관리 회사의 성장

- 쓰레기 수거차의 기술 발전

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용

- 높은 유지 보수 및 수리 비용

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 적재 메커니즘별(2021-2034년)

- 주요 동향

- 완전 자동화

- 반자동

- 수동

제6장 시장 추계 및 예측 : 용량별(2021-2034년)

- 주요 동향

- 10,000파운드 미만

- 10,000-20,000 파운드

- 20,000-30,000 파운드

- 30,000 파운드 이상

제7장 시장 추계 및 예측 : 연료별(2021-2034년)

- 주요 동향

- 디젤

- 전기

- CNG

- 하이브리드

- 기타

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 지자체의 폐기물 수거

- 산업 폐기물 수거

- 상업 폐기물 수거

- 건설 폐기물 및 해체 폐기물

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 시정 서비스

- 민간 폐기물 관리 회사

- 전문 폐기물 처리 업자

- 기타

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- Amrep

- Autocar

- Bridgeport Manufacturing

- Bucher Municipal

- BYD

- Curbtender

- Dennis Eagle

- FAUN Zoeller(UK)

- Foton Motor

- Freightliner(Daimler)

- Fujian Longma Environmental Sanitation Equipment

- Heil

- Isuzu

- Labrie Trucks

- Mack Trucks

- McNeilus Truck and Manufacturing

- New Way Refuse Trucks

- NTM

- Pak-Mor

- Peterbilt Motors Company

The Global Side Loader Refuse Trucks Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 4.6 billion by 2034. As cities around the world continue to expand, the demand for efficient and space-conscious waste collection vehicles has surged. Urban development naturally brings with it higher population densities and increased volumes of solid waste, creating an urgent need for systems that can handle waste collection in tight spaces. Side loader refuse trucks have become the go-to solution in urban areas, thanks to their ability to maneuver through narrow roads and busy streets. Their compatibility with standardized waste bins also makes them a preferred option for municipalities aiming to streamline collection processes. Urban centers are moving towards cleaner and more efficient waste management practices, which has significantly accelerated the adoption of side loader trucks.

Government regulations are also playing a critical role in the growing adoption of these vehicles. Stricter environmental and safety standards are pushing local authorities and private firms to invest in modern, low-emission technologies. Side loaders powered by electric and hybrid systems are gaining traction as cities aim to improve air quality and reduce carbon emissions. These vehicles not only help meet environmental goals but also improve operational performance by consuming less fuel and reducing maintenance time.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 5.1% |

In terms of application, the market is divided into industrial waste, municipal waste, commercial waste, and construction and demolition waste. Municipal waste collection dominated in 2024, with a market value of around USD 1 billion, representing over 45% of the market share. With rapid urbanization, waste generated in city areas continues to rise, and this increase is reflected in the higher demand for municipal collection services. As waste volumes grow, municipalities are turning to side loader trucks to handle rising pressure on their sanitation systems.

The automated design of these trucks has proven to be especially valuable for city governments looking to reduce labor costs. With automated arms and bin-lifting mechanisms, side loaders require fewer operators, making them more cost-effective and efficient. These trucks allow consistent and uninterrupted waste collection with minimal human intervention, leading to better workforce management and productivity gains. City governments are increasingly adopting such technologies, often supported by public funding or grants, to improve the effectiveness of their waste management systems.

When it comes to loading mechanisms, the market is segmented into fully automated, semi-automated, and manual systems. Fully automated side loader trucks led the market in 2024, holding around 43% of the total share. These trucks are capable of performing all core functions - including lifting, loading, and emptying bins - with just one operator. This automation not only helps reduce the labor force but also speeds up collection processes, minimizes downtime, and increases accuracy. As technology continues to advance, these fully automated systems are becoming more reliable and essential in large urban settings.

Fuel type is another critical segmentation, with diesel, electric, CNG, hybrid, and other fuel types in the mix. Diesel-powered trucks led the market in 2024. Despite the growing popularity of alternative fuels, diesel remains the most practical and cost-effective choice for many municipalities and private operators. Diesel trucks are known for their durability, easier maintenance, and well-established refueling infrastructure. For long-haul routes and heavy-duty operations, diesel continues to offer unmatched reliability and lower upfront costs compared to electric or CNG-powered alternatives.

In terms of end users, the market is segmented into municipal services, specialized waste handlers, private waste management companies, and others. Municipal services took the lead in 2024. Local governments handle the majority of waste collection in urban areas, especially in densely populated neighborhoods. Side loader trucks serve these regions efficiently due to their compact design and automated capabilities. With access to government subsidies and budget allocations, municipalities are better positioned to invest in updated and cost-efficient waste collection technologies that support their environmental goals.

Geographically, North America held a major share of the market, accounting for over 35% in 2024. The U.S. alone reached a market value of approximately USD 541.2 million. The country's high urban population, combined with strict state-level regulations, has made automated and clean waste collection technologies a necessity. Waste collection authorities are increasingly investing in electric and hybrid models to comply with emission mandates while reducing overall operating costs.

Major manufacturers in this space are now focusing heavily on sustainability, competing by offering models with smart automation, electric drivetrains, and diagnostic features. Companies that can provide low or zero-emission vehicles are finding more opportunities in regions with green procurement policies, especially in North America and Europe. The competitive edge lies in offering vehicles that balance performance, fuel efficiency, safety, and environmental compliance in a cost-effective package.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material and component supplier

- 3.2.2 Truck and equipment manufacturer

- 3.2.3 Technology and telematics providers

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Impact of trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Price analysis

- 3.7.1 Region

- 3.7.2 Propulsion

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Urbanization and population growth

- 3.10.1.2 Regulatory push for clean and efficient waste collection

- 3.10.1.3 Growth of private waste management companies

- 3.10.1.4 Technological advancements in refuse trucks

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost

- 3.10.2.2 High maintenance and repair costs

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Loading Mechanism, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Fully automated

- 5.3 Semi-automated

- 5.4 Manual

Chapter 6 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Less than 10,000 lbs

- 6.3 10,000 to 20,000 lbs

- 6.4 20,000 to 30,000 lbs

- 6.5 More than 30,000 lbs

Chapter 7 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Electric

- 7.4 CNG

- 7.5 Hybrid

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Municipal waste collection

- 8.3 Industrial waste collection

- 8.4 Commercial waste collection

- 8.5 Construction and demolition waste

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Municipal services

- 9.3 Private waste management companies

- 9.4 Specialized waste handlers

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Amrep

- 11.2 Autocar

- 11.3 Bridgeport Manufacturing

- 11.4 Bucher Municipal

- 11.5 BYD

- 11.6 Curbtender

- 11.7 Dennis Eagle

- 11.8 FAUN Zoeller (UK)

- 11.9 Foton Motor

- 11.10 Freightliner (Daimler)

- 11.11 Fujian Longma Environmental Sanitation Equipment

- 11.12 Heil

- 11.13 Isuzu

- 11.14 Labrie Trucks

- 11.15 Mack Trucks

- 11.16 McNeilus Truck and Manufacturing

- 11.17 New Way Refuse Trucks

- 11.18 NTM

- 11.19 Pak-Mor

- 11.20 Peterbilt Motors Company