|

시장보고서

상품코드

1740958

자동차 도어 실 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automotive Door Sills Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

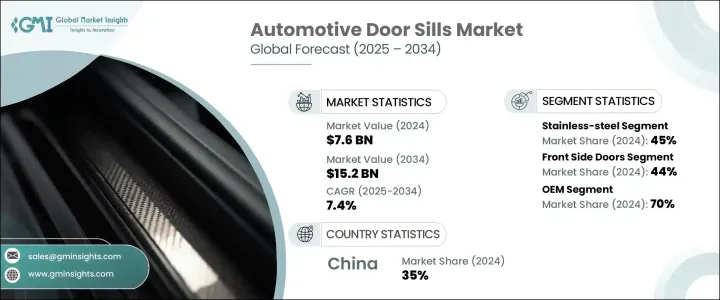

세계의 자동차 도어 실 시장 규모는 2024년에 76억 달러로 평가되었고, 2034년에는 152억 달러에 이를 것으로 예측되며, CAGR 7.4%로 성장할 전망입니다.

이러한 확장을 촉진하는 주요 요인은 차량 진입 시스템에 대한 관심이 높아지고 전 세계 자동차 생산량이 지속적으로 증가하고 있다는 점입니다. 차량이 더욱 스마트한 기술과 세련된 미학으로 진화함에 따라 도어실은 더 이상 단순한 보호 트림이 아니라 디자인과 기능을 모두 향상시키는 다기능 부품으로 간주되고 있습니다. 자동차 제조업체는 조명 시스템, 근접 감지, 고강도 소재와 같은 고급 기능을 통합하여 사용자 경험, 내구성 및 시각적 매력을 개선하고 있습니다. 경량 설계는 전기차와 하이브리드 자동차에서 특히 중요하기 때문에 무게를 늘리지 않으면서도 강도를 제공하는 소재에 대한 수요가 증가하고 있습니다. 탄소 섬유, 알루미늄, 내충격성 폴리머는 성능과 스타일링 기준을 모두 충족하는 현대적인 실을 제작하는 데 필수적인 소재가 되고 있습니다. 이러한 소재는 복잡한 디자인, 향상된 구조적 성능, 환경 조건에 대한 더 나은 저항성을 가능하게 하여 에너지 효율과 장기 사용이라는 광범위한 목표를 지원합니다.

또한 자동차 도어 실은 인터랙티브 요소를 도입한 센서 기반 혁신을 통해 변화하고 있습니다. 제조업체들은 사람의 접근에 반응하고 주변 조명과 조화를 이루며 터치 또는 제스처 제어까지 가능한 스마트 도어실을 연구하고 있습니다. 이러한 기능을 통해 도어실은 최신 차량의 지능형 아키텍처의 일부로 자리매김하여 차량의 광범위한 인포테인먼트 및 엔트리 시스템과 원활하게 통합됩니다. 기술이 자동차 인테리어와 계속 융합됨에 따라 이러한 향상된 도어실은 고품질의 맞춤형 주행 경험을 제공하는 데 매우 중요해지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 76억 달러 |

| 예측 금액 | 152억 달러 |

| CAGR | 7.4% |

2024년 스테인리스 스틸은 약 45%를 차지하며 시장에서 가장 큰 점유율을 차지했으며 2034년까지 7% 이상의 CAGR로 성장할 것으로 예상됩니다. 이러한 우위는 스테인리스 스틸의 탁월한 내구성, 비용 효율성, 내충격성 덕분입니다. 특히 SUV나 플릿카와 같이 교통량이 많은 차량에서 반복적인 입출고에도 잘 견딥니다. 또한 내식성이 뛰어나 혹독한 날씨나 도로 조건에서도 시각적, 구조적으로 온전한 상태를 유지할 수 있습니다. 전기 및 하이브리드 모델의 경우 스테인리스 스틸은 차체 무결성을 지원하는 데 필요한 구조적 강도를 제공하는 동시에 조명 로고, 다이내믹 조명 또는 스마트 액세스 모듈과 같은 최신 기능을 수용할 수 있습니다.

용도별로는 전면 도어 부문은 2024년 44%의 점유율로 시장을 주도했으며 2025년부터 2034년까지 7% 이상의 연평균 성장률로 확대될 것으로 예상됩니다. 전면 도어실은 운전자와 승객 모두의 상호작용이 가장 많기 때문에 보호 및 장식용 업그레이드의 주요 초점이 되고 있습니다. 자동차 제조업체는 차량에 탑승할 때 주요 시각 및 촉각 접점을 형성하기 때문에 이 부분을 활용하여 브랜딩 요소와 사용자 중심 기능을 도입합니다. 첫인상을 남기고 차량의 전반적인 디자인 품질을 강조하기 위해 일루미네이티드 실과 로고가 강화된 트림이 여기에 통합되는 경우가 많습니다.

차량 유형별로 분류하면 승용차 부문은 세단, 해치백, 소형 SUV의 높은 글로벌 생산량으로 인해 계속해서 우위를 점하고 있습니다. 구매자들이 시각적으로 매력적이고 기능적인 인테리어 업그레이드를 선호함에 따라 제조업체들은 이러한 차량에 보호 기능과 고급스러움을 겸비한 스테인리스 스틸 및 조명 실 플레이트를 장착하고 있습니다. 전기 및 자율주행 모델로의 전환이 증가함에 따라 도어실 부품도 통합 전자 시스템과 호환되도록 진화하고 있으며, 단순한 외형적 역할을 넘어 그 중요성이 강화되고 있습니다.

아시아태평양 지역에서는 중국이 2024년 약 7억 달러의 매출과 약 35%의 지역 점유율을 기록하며 시장을 주도하는 국가로 부상했습니다. 세계 최대 자동차 생산국으로서의 지위와 전기자동차에 대한 국내 수요 증가가 이러한 리더십에 크게 기여하고 있습니다. 한국의 탄탄한 제조 생태계는 첨단 도어실 시스템의 효율적인 생산과 수출을 가능하게 합니다.

이 시장은 사용자 중심의 인체공학, 고성능 소재, 주변 통합과 같은 자동차 산업 트렌드에 의해 형성되고 있습니다. 기계적 스트레스, 날씨 노출, 전자 부품 안정성 등의 문제를 해결하기 위해 제조업체들은 내충격성이 뛰어난 열가소성 플라스틱, 자외선 안정 마감재, 방수 LED 시스템을 채택하고 있습니다. 이러한 업그레이드는 특히 프리미엄 차량 부문에서 극한의 기후와 지속적인 사용 환경에서 실의 내구성을 향상시킵니다.

특히 조명과 센서가 통합된 모델의 경우 첨단 제조 기술을 통해 장착 정확도가 향상되고 있습니다. 빠른 조립 접착제 및 클립 잠금 시스템을 사용하여 진동으로 인한 손상을 최소화하고 보다 깔끔한 설치를 보장합니다. 또한 EMI 차폐 배선과 최적화된 케이블 라우팅으로 조명이 설치된 실에서 신호 간섭을 방지할 수 있습니다. 이제 AI 및 3D 시각화 기반의 지능형 설계 플랫폼을 통해 실 모듈을 신속하게 프로토타이핑하고 맞춤화할 수 있습니다. 이러한 도구를 사용하면 브랜딩 목표, 사용자 인터페이스 기대치, 차량 미학에 정확하게 맞출 수 있으므로 도어실은 차세대 차량 실내에서 상호 작용의 핵심 지점이 될 수 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 제조업자

- 원자재 공급자

- 자동차 OEM

- 유통 채널

- 최종 용도

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(고객에 대한 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 이익률 분석

- 기술과 혁신의 상황

- 특허 분석

- 주요 뉴스와 대처

- 규제 상황

- 가격 동향 분석

- 제품

- 지역

- 코스트 내역 분석

- 영향요인

- 성장 촉진요인

- 차량 맞춤화에 대한 수요 증가

- 실내 보호에 대한 인식 증가

- 전기 및 고급 차량 판매 증가

- 세계 자동차 생산 증가

- 업계의 잠재적 위험 및 과제

- 고급 설계의 높은 제조 비용

- 열악한 환경에서의 내구성 문제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 스테인리스 스틸

- 알루미늄

- 고무

- 플라스틱

- 탄소 섬유

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 전면 도어

- 후면 도어

- 테일 게이트

제7장 시장 추계 및 예측 : 차량 유형별(2021-2034년)

- 주요 동향

- 승용차

- 상용차

- 소형 상용차

- 중형 상용차

- 대형 상용차

제8장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- AC Schnitzer

- BMW

- Bosch

- Galio

- Gestamp

- Gronbach

- Hangzhou Green Offroad Auto Parts

- Honda Access

- Innotec

- Key Safety Systems(KSS)

- Mahle

- Mopar(FCA)

- Normic Industries

- Prius Auto Industries

- Rugged Ridge

- Shenzhen ATR Industry

- Shenzhen Yanming Plate Process

- SKS Kontakttechnik

- STEProtect(Sliplo)

- Zealio Electronics

The Global Automotive Door Sills Market was valued at USD 7.6 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 15.2 billion by 2034. A key factor fueling this expansion is the heightened focus on vehicle entry systems and the consistent rise in global automobile production. As vehicles evolve with smarter technologies and more refined aesthetics, door sills are no longer viewed as simple protective trims but as multifunctional components that enhance both design and functionality. Automakers are integrating advanced features like lighting systems, proximity detection, and high-strength materials to improve user experience, durability, and visual appeal. Lightweight designs are especially important in electric and hybrid vehicles, driving the demand for materials that provide strength without adding extra weight. Carbon fiber, aluminum, and impact-resistant polymers are becoming essential in creating modern sills that meet both performance and styling standards. These materials allow for intricate designs, improved structural performance, and better resistance to environmental conditions, all of which support the broader goals of energy efficiency and long-term use.

Automotive door sills are also being transformed through sensor-based innovations that bring interactive elements into the mix. Manufacturers are exploring smart sills that can respond to human proximity, coordinate with ambient lighting, and even enable touch or gesture controls. These features position the door sill as part of the intelligent architecture of modern vehicles, seamlessly integrating with the car's broader infotainment and entry systems. As technology continues to merge with automotive interiors, these enhanced sills are becoming crucial for delivering a high-quality, customized driving experience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.6 billion |

| Forecast Value | $15.2 Billion |

| CAGR | 7.4% |

In 2024, stainless steel held the largest share of the market, accounting for approximately 45%, and is projected to grow at a CAGR exceeding 7% through 2034. This dominance is due to stainless steel's unmatched durability, cost-effectiveness, and impact resistance. It holds up well under repeated entry and exit, especially in high-traffic vehicles like SUVs and fleet cars. Its corrosion resistance also ensures that it remains visually and structurally intact even under harsh weather or road conditions. For electric and hybrid models, stainless steel offers the structural strength needed to support vehicle body integrity while accommodating modern features like illuminated logos, dynamic lighting, or smart access modules.

From an application perspective, the front side doors segment led the market with a 44% share in 2024 and is expected to expand at a CAGR of over 7% between 2025 and 2034. Front door sills see the highest interaction from both drivers and passengers, making them the primary focus for protective and decorative upgrades. Auto manufacturers leverage this section to introduce branding elements and user-centric features, as it forms a major visual and tactile contact point when entering the vehicle. Illuminated sills and logo-enhanced trims are frequently integrated here to leave a lasting first impression and emphasize the vehicle's overall design quality.

When classified by vehicle type, the passenger cars segment continues to dominate due to the high global production volumes of sedans, hatchbacks, and compact SUVs. As buyers lean toward visually appealing and functional interior upgrades, manufacturers are equipping these vehicles with stainless steel and lighted sill plates that combine protection with a touch of luxury. With the increasing shift toward electric and autonomous models, door sill components are also evolving to be compatible with integrated electronic systems, reinforcing their importance beyond just cosmetic roles.

In the Asia-Pacific region, China emerged as the dominant market player in 2024, generating approximately USD 700 million and holding around 35% of the regional share. Its position as the world's largest vehicle producer and growing domestic appetite for electric vehicles contribute significantly to this leadership. The country's robust manufacturing ecosystem enables efficient production and export of advanced door sill systems.

The market is being shaped by automotive industry trends such as user-focused ergonomics, high-performance materials, and ambient integration. To address challenges like mechanical stress, weather exposure, and electronic component stability, manufacturers now employ thermoplastics with high impact resistance, UV-stable finishes, and waterproof LED systems. These upgrades enhance the sills' durability in extreme climates and under constant use, especially in premium vehicle segments.

Advanced manufacturing techniques are improving fitment accuracy, particularly for models featuring integrated lights and sensors. The use of quick-assembly adhesives and clip-lock systems minimizes vibration damage and ensures cleaner installations. Meanwhile, EMI-shielded wiring and optimized cable routing helps avoid signal interference in illuminated sills. Intelligent design platforms powered by AI and 3D visualization are now enabling rapid prototyping and customization of sill modules. These tools allow for precise alignment with branding goals, user interface expectations, and vehicle aesthetics, making door sills a key point of interaction in next-generation vehicle cabins.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Distribution channel

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing trend analysis

- 3.9.1 Product

- 3.9.2 Region

- 3.10 Cost breakdown analysis

- 3.11 Impact on forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising demand for vehicle customization

- 3.11.1.2 Growing awareness of interior protection

- 3.11.1.3 Growth in electric and luxury vehicle sales

- 3.11.1.4 Increasing automotive production globally

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High manufacturing costs of advanced designs

- 3.11.2.2 Durability concerns in harsh environments

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Stainless steel

- 5.3 Aluminum

- 5.4 Rubber

- 5.5 Plastic

- 5.6 Carbon fiber

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Front side doors

- 6.3 Back side door

- 6.4 Tailgate

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles

- 7.3.2 Medium commercial vehicles

- 7.3.3 Heavy commercial vehicles

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AC Schnitzer

- 10.2 BMW

- 10.3 Bosch

- 10.4 Galio

- 10.5 Gestamp

- 10.6 Gronbach

- 10.7 Hangzhou Green Offroad Auto Parts

- 10.8 Honda Access

- 10.9 Innotec

- 10.10 Key Safety Systems (KSS)

- 10.11 Mahle

- 10.12 Mopar (FCA)

- 10.13 Normic Industries

- 10.14 Prius Auto Industries

- 10.15 Rugged Ridge

- 10.16 Shenzhen ATR Industry

- 10.17 Shenzhen Yanming Plate Process

- 10.18 SKS Kontakttechnik

- 10.19 STEProtect (Sliplo)

- 10.20 Zealio Electronics