|

시장보고서

상품코드

1740969

오토인젝터 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Autoinjectors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

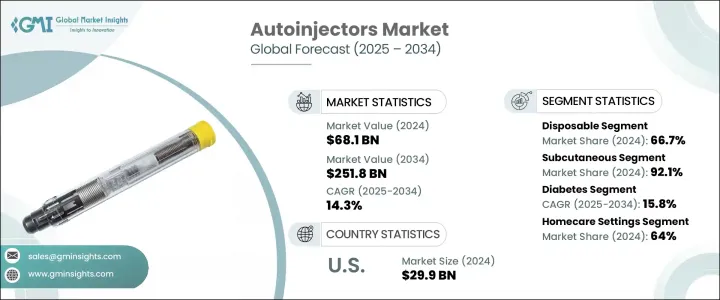

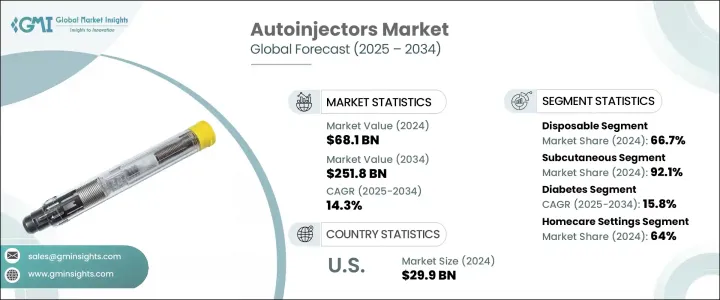

세계의 오토인젝터 시장 규모는 2024년에 681억 달러로 평가되었고, 2034년에는 2,518억 달러에 이를 것으로 예측되며, CAGR 14.3%로 성장할 전망입니다.

이이러한 성장에 기여하는 주요 요인으로는 당뇨병 및 아나필락시스와 같은 만성 질환의 유병률 증가와 일반 오토인젝터의 가용성 증가를 들 수 있습니다. 이러한 의료기기는 생명을 구하는 약물을 빠르고 안정적으로 투여하는 데 필수적이며, 이는 당뇨병이나 심각한 알레르기 반응과 같은 질환을 관리하는 데 매우 중요합니다.

전 세계적으로 당뇨병, 특히 제1형과 제2형 당뇨병 환자 수가 증가하는 것이 오토인젝터 수요의 주요 촉진요인 중 하나입니다. 이러한 장치는 효율적이고 환자 친화적인 인슐린 전달 방법을 제공하므로 정기적인 주사가 필요한 당뇨병 환자에게 선호되는 옵션입니다. 당뇨병과 더불어 일반적으로 알레르겐에 의해 유발되는 아나필락시스 반응의 발생이 증가하면서 에피네프린을 전달하는 오토인젝터에 대한 수요도 크게 증가했습니다. 오토인젝터의 휴대성, 사용 편의성, 정밀한 투약 기능 덕분에 신속한 응급 치료를 제공하는 데 매우 유용하게 사용되고 있습니다. 이러한 질환의 발생률이 증가함에 따라 오토인젝터 시장도 그에 따라 확대될 것으로 예상됩니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 681억 달러 |

| 예측 금액 | 2,518억 달러 |

| CAGR | 14.3% |

시장은 일회용 오토인젝터와 재사용 가능한 오토인젝터로 분류됩니다. 일회용 오토인젝터는 2024년 66.7%의 시장 점유율을 차지하며 지배적인 부문입니다. 이러한 일회용 장치는 편리함과 사용 편의성으로 인해 특히 매력적입니다. 최소한의 유지 관리가 필요하므로 환자가 특별한 지식이나 기술이 없어도 작동할 수 있습니다. 또한 이러한 오토인젝터는 1회용으로 설계되어 감염이나 오염의 위험이 줄어들어 환자의 안전을 보장합니다. 팬데믹 이후, 특히 당뇨병 환자의 경우 재택 치료로 전환하는 추세에 있습니다. 이러한 변화로 인해 환자들이 집에서 약물을 자가 투여할 때 휴대성과 사용 편의성을 중요하게 생각하면서 일회용 오토인젝터에 대한 선호도가 더욱 높아졌습니다.

또 다른 중요한 요인은 투여 경로이며, 피하 주사가 2024년 점유율 92.1%로 시장을 선도하고 있습니다. 피하 주사는 근육 주사보다 통증이 적고 집에서 자가 투여가 가능하기 때문에 당뇨병과 같은 만성 질환을 관리하는 환자에게 매우 적합합니다. 피하 주사는 인슐린 및 단일 클론 항체를 포함한 생물학적 제제에도 일반적으로 사용되어 이러한 기기에 대한 수요를 더욱 촉진하고 있습니다.

또한 시장은 치료법에 따라 세분화되며, 당뇨병 부문은 예측 기간 동안 15.8%의 연평균 성장률(CAGR)을 기록하며 가장 높은 성장률을 보일 것으로 예상됩니다. 이러한 성장은 지속적인 치료가 필요한 당뇨병 환자가 전 세계적으로 증가하고 있기 때문입니다. 오토인젝터는 인슐린 투여를 위한 보다 편안하고 사용자 친화적인 방법을 제공하여 광범위한 사용을 촉진합니다. 또한 투약 정확도와 추적 기능이 향상된 스마트 오토인젝터와 같은 인슐린 전달 장치의 발전으로 환자 순응도가 향상되고 이 부문의 성장이 뒷받침되고 있습니다.

최종 사용자에 관해서는 재택 치료의 현장이 시장을 독점하고 있으며 2024년 시장 점유율의 64%를 차지했습니다. 환자의 독립성에 따른 자가 투여에 대한 수요 증가가 이러한 변화에 기여하는 주요 요인입니다. 오토인젝터를 사용하면 만성 질환을 앓고 있는 환자가 집에서 치료를 관리할 수 있어 의료 시설을 자주 방문할 필요가 줄어듭니다. 또한 원격 의료 및 원격 모니터링의 증가로 환자가 집에서 오토인젝터를 더 쉽게 사용할 수 있게 되었으며, 의료 전문가가 원거리에서 지도와 지원을 제공할 수 있게 되었습니다.

2024년에는 미국이 약 299억 달러의 수익으로 북미 시장을 리드했습니다. 이는 미국에서 당뇨병과 류마티스 관절염을 비롯한 만성 질환의 발병률이 높기 때문입니다. 자가 투여 치료 옵션을 찾는 환자가 늘어나면서 오토인젝터는 이러한 질환을 관리하기 위한 솔루션으로 점점 인기를 얻고 있습니다.

오토인젝터 시장은 글로벌 및 지역 기업들이 자가 투여 기기에 대한 수요 증가를 충족하기 위해 다양한 솔루션을 제공하면서 경쟁이 치열합니다. 주요 업체들이 전체 시장 점유율의 약 60%를 차지하며 시장을 지배하고 있습니다. 이러한 기업들은 환자 경험과 치료 순응도를 개선하기 위해 설계된 새로운 제품과 솔루션을 도입하여 시장 지위를 유지하기 위해 지속적으로 혁신하고 있습니다. 또한 신흥 시장에서 경제성이 주요 관심사로 떠오르면서 현지 제조업체들이 비용 효율적인 대안을 제시하고 있어 글로벌 기업들은 제품 안전과 규제 준수를 보장하면서 가격 전략을 조정해야 하는 상황에 처해 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 표적 치료법에 대한 수요 증가

- 전 세계적으로 일반 오토인젝터의 가용성

- 당뇨병 및 아나필락시스 발생률 증가

- 약물 자가 투여에 대한 환자 선호도 증가

- 업계의 잠재적 위험 및 과제

- 대체 치료 옵션의 가용성

- 자동 주입기의 높은 가격

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 일회용

- 재사용 가능

제6장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 피하

- 근육내

제7장 시장 추계 및 예측 : 치료별(2021-2034년)

- 주요 동향

- 류마티스 관절

- 다발성 경화증

- 아나필락시스

- 당뇨병

- 기타 치료법

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원 및 진료소

- 재택 치료

- 기타 용도

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AbbVie

- Amgen

- Antares Pharma

- Becton, Dickinson and Company

- Eli Lilly and Company

- GlaxoSmithKline

- Halozyme

- Johnson & Johnson

- Mylan

- Novo Nordisk

- Owen Mumford

- SHL Medical

- Teva pharmaceuticals

- West Pharmaceutical Services

- Ypsomed

The Global Autoinjectors Market was valued at USD 68.1 billion in 2024 and is estimated to grow at a CAGR of 14.3% to reach USD 251.8 billion by 2034. The primary factors contributing to this growth include the rising prevalence of chronic conditions such as diabetes and anaphylaxis, as well as the increased availability of generic autoinjectors. These medical devices are essential for the quick and reliable administration of life-saving medications, which is crucial for managing conditions like diabetes and severe allergic reactions.

The increase in the number of diabetes cases worldwide, particularly type 1 and type 2, is one of the key drivers for the demand for autoinjectors. These devices offer an efficient and patient-friendly method for insulin delivery, making them a preferred option for people with diabetes who need regular injections. Alongside diabetes, the growing occurrence of anaphylactic reactions, typically triggered by allergens, has significantly boosted the demand for autoinjectors that deliver epinephrine. The portability, ease of use, and precise dosing capabilities of autoinjectors have made them invaluable in providing rapid emergency treatment. As the incidence of these conditions rises, the market for autoinjectors is expected to expand accordingly.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $68.1 Billion |

| Forecast Value | $251.8 Billion |

| CAGR | 14.3% |

The market is categorized into disposable and reusable autoinjectors. Disposable autoinjectors are the dominant segment, holding a market share of 66.7% in 2024. These single-use devices are particularly appealing due to their convenience and ease of use. They require minimal maintenance, which eliminates the need for patients to have special knowledge or skills to operate them. The fact that these autoinjectors are designed for one-time use also reduces the risk of infection or contamination, ensuring patient safety. Following the pandemic, there has been a shift toward home-based care, particularly for diabetic patients. This change has further driven the preference for disposable autoinjectors, as patients value portability and ease of use in self-administering their medications at home.

Another important factor is the route of administration, with subcutaneous autoinjectors leading the market with a share of 92.1% in 2024. Subcutaneous injections are less painful than intramuscular ones, and they can be self-administered at home, making them highly suitable for patients managing chronic diseases like diabetes. Subcutaneous injections are also commonly used for biologics, including insulin and monoclonal antibodies, further driving the demand for these devices.

The market is also segmented based on therapy, with the diabetes segment expected to see the highest growth rate, reaching a CAGR of 15.8% during the forecast period. This growth is attributed to the increasing number of diabetes cases globally, which necessitate ongoing treatment. Autoinjectors offer a more comfortable and user-friendly method for insulin administration, promoting their widespread use. Moreover, advancements in insulin delivery devices, such as smart autoinjectors with improved dosing accuracy and tracking features, are enhancing patient adherence and supporting the growth of this segment.

When it comes to end users, homecare settings dominate the market, accounting for 64% of the market share in 2024. The rising demand for self-administration, driven by patient independence, is a major factor contributing to this shift. Autoinjectors allow patients with chronic conditions to manage their treatment at home, reducing the need for frequent visits to healthcare facilities. Additionally, the rise of telemedicine and remote monitoring has made it easier for patients to use autoinjectors at home, with healthcare professionals providing guidance and support from a distance.

In 2024, the U.S. led the North American market with a revenue of approximately USD 29.9 billion. This is largely due to the high incidence of chronic diseases, including diabetes and rheumatoid arthritis, in the country. As more patients seek self-administered treatment options, autoinjectors have become an increasingly popular solution for managing these conditions.

The autoinjectors market is highly competitive, with global and regional companies offering a range of solutions to meet the growing demand for self-administration devices. Key players dominate the market, contributing approximately 60% of the overall market share. These companies continually innovate to maintain their market position, introducing new products and solutions designed to improve patient experience and treatment adherence. Furthermore, as affordability becomes a key concern in emerging markets, local manufacturers are stepping in to offer cost-effective alternatives, forcing international companies to adjust their pricing strategies while ensuring product safety and regulatory compliance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for targeted therapies

- 3.2.1.2 Availability of generic autoinjectors globally

- 3.2.1.3 Increasing incidence of diabetes and anaphylaxis

- 3.2.1.4 Rising patient preference towards self-administration of medication

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative treatment options

- 3.2.2.2 High pricing of the autoinjectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Disposable

- 5.3 Reusable

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Subcutaneous

- 6.3 Intramuscular

Chapter 7 Market Estimates and Forecast, By Therapy, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Rheumatoid arthritis

- 7.3 Multiple sclerosis

- 7.4 Anaphylaxis

- 7.5 Diabetes

- 7.6 Other therapies

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital and clinics

- 8.3 Homecare settings

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Amgen

- 10.3 Antares Pharma

- 10.4 Becton, Dickinson and Company

- 10.5 Eli Lilly and Company

- 10.6 GlaxoSmithKline

- 10.7 Halozyme

- 10.8 Johnson & Johnson

- 10.9 Mylan

- 10.10 Novo Nordisk

- 10.11 Owen Mumford

- 10.12 SHL Medical

- 10.13 Teva pharmaceuticals

- 10.14 West Pharmaceutical Services

- 10.15 Ypsomed