|

시장보고서

상품코드

1741012

액화수소 저장 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Liquefied Hydrogen Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

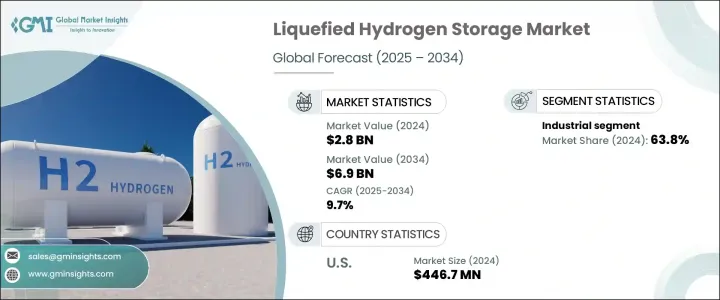

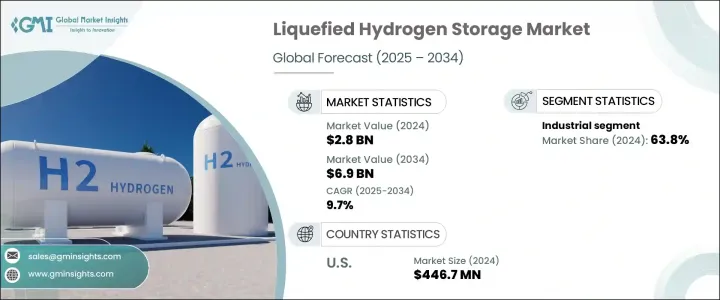

세계의 액화수소 저장 시장은 2024년에 28억 달러로 평가되었고, 보다 깨끗한 대체 에너지로의 세계 변화 증가를 배경으로 CAGR 9.7%로 성장할 전망이며, 2034년에는 69억 달러에 이를 것으로 예측됩니다.

탈탄소화에 대한 노력이 강화되는 가운데 액화수소는 미래의 에너지 전망을 재구성하는 중요한 요소가 되고 있습니다. 정부, 기업, 소비자는 보다 깨끗하고 효율적인 솔루션을 추구하며 수소 기술의 비옥한 토양을 만들어 가고 있습니다. 액화수소 저장은 이 변혁의 중심에 있으며, 신재생 에너지 통합을 위한 확장 가능하고 효율적이며 비용 효율적인 솔루션을 제공하고 있습니다. 극저온 기술, 보다 스마트한 감시 시스템, 콤팩트한 설계의 돌파는 업계를 보다 높은 신뢰성과 저렴한 가격으로 끌어올리고 있습니다. 잉여 재생에너지를 수소로 저장해 수요가 정점에 이르렀을 때 이용하는 능력은 간헐성과 송전망 안정성에 관한 중요한 과제를 해결하고 있습니다. 각국이 인프라 업그레이드 및 에너지 회복력에 고액의 투자를 실시하는 가운데, 액화수소 저장은 산업계 전체에서 불가결한 존재가 될 태세를 갖추고 있습니다. 민간의 기술 혁신, 공적 자금, 그리고 유리한 규제의 틀이 융합되어 전례 없는 성장 기회가 풀려가고 있으며, 세계 에너지 경제에서 매우 중요한 전환의 조짐을 보이고 있습니다.

액화수소로의 이행은 산업활동의 틀을 넘어 모빌리티, 에너지 저장, 분산형 발전으로 크게 퍼지고 있습니다. 세계 정부의 대처가 이 기세를 가속시켜, 보다 환경 친화적인 기술을 채용하기 위한 보조금이나 정책적 인센티브를 제공하고 있습니다. 배기가스 규제의 강화는 수송, 발전, 중공업의 각 분야에서 수소 솔루션의 매력을 높이고 있습니다. 액화수소 저장은 이러한 급속하게 진화하는 용도에서 강력한 견인력을 얻고 있으며, 세계 기후변화 목표에 따른 장기적이고 지속 가능한 에너지 솔루션의 무대를 갖추고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 28억 달러 |

| 예측 금액 | 69억 달러 |

| CAGR | 9.7% |

화학, 정유소, 고열 제조 등의 분야가 화석연료로부터의 탈각을 목표로 수소를 통합하고 있기 때문에 2024년 산업 분야의 점유율은 63.8%로 압도이었습니다. 액화수소는 에너지 밀도가 높기 때문에 대규모 저장이나 고효율 운전에 이상적이며 여전히 바람직한 선택지입니다. 대용량으로 장거리 에너지 저장의 필요성이 높아지고 있기 때문에 액화수소는 제로 0이미션 성능에 중점을 두는 수송 시스템에 있어서도 획기적인 존재가 되고 있습니다. 컴팩트한 저장 프레임워크로 장시간의 에너지 출력을 실현하는 액화수소의 능력은 산업계가 공간과 효율의 제약에 임하는데 매우 중요합니다. 간헐적인 재생에너지원 확대가 가속화되는 가운데 송전망의 안정성을 확보하기 위해 수요와 공급의 균형을 맞추는 수소의 역할은 더욱 중요해지고 있습니다.

미국의 액화수소 저장 2024년 수소 시장은 4억 4,670만 달러에 이르렀으며, 수소 인프라, 특히 연료 공급 스테이션과 대규모 저장 프로젝트에 대한 왕성한 투자가 그 원동력이 되고 있습니다. 고도의 제조 능력과 전기차 및 수소차 산업의 성장이 수요를 뒷받침하고 있습니다. 에너지부를 비롯한 연방정부의 이니셔티브는 미래를 위해 저장의 확장성과 신뢰성을 높이기 위한 연구개발 노력을 적극적으로 지원하고 있습니다.

경쟁력을 유지하기 위해 FuelCell Energy, Cockerill Jingli, ITM Power, SSE, Air Products and Chemicals, ENGIE, Linde, McPhy Energy, Air Liquide, Gravitricity, GKN, Nel 등의 기업은 기술 혁신 및 전략적 파트너십을 강화하고 있습니다. 주요 전략으로는 생산 능력 확대, 극저온 단열기술의 진보, 장기적 연구에 대한 투자, 전개와 제품 다양화를 신속하게 진행하기 위한 공동사업 형성 등이 있습니다. 정부 지원 프로그램에 대한 적극적인 참여도 이들 기업이 신흥 시장에서 자금을 확보하고 선행자 이익을 쌓는 데 도움이 되고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 무역관리 관세분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 전략적 전망

- 혁신 및 지속가능성의 정세

제5장 시장 규모 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 산업

- 교통기관

- 거치형

- 기타

제6장 시장 규모 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 네덜란드

- 러시아

- 아시아태평양

- 중국

- 일본

- 인도

제7장 기업 프로파일

- Air Liquide

- Air Products and Chemicals

- Cockerill Jingli

- ENGIE

- FuelCell Energy

- GKN

- Gravitricity

- ITM Power

- Linde

- McPhy Energy

- Nel

- SSE

The Global Liquefied Hydrogen Storage Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 6.9 billion by 2034, driven by the growing worldwide shift toward cleaner energy alternatives. As decarbonization efforts intensify, liquefied hydrogen is becoming a key player in reshaping the future energy landscape. Governments, corporations, and consumers are aligning to demand cleaner, more efficient solutions, creating fertile ground for hydrogen technologies. Liquefied hydrogen storage is at the heart of this transformation, providing a scalable, efficient, and cost-effective solution for renewable energy integration. Breakthroughs in cryogenic technologies, smarter monitoring systems, and compact designs are pushing the industry toward higher reliability and affordability. The ability to store excess renewable energy as hydrogen and utilize it when demand peaks is solving critical challenges related to intermittency and grid stability. As nations invest heavily in infrastructure upgrades and energy resilience, liquefied hydrogen storage is poised to become indispensable across industries. Private-sector innovation, public funding, and favorable regulatory frameworks are converging to unlock unprecedented growth opportunities, signaling a pivotal shift in the global energy economy.

The transition to liquefied hydrogen is extending beyond industrial operations and making strong inroads into mobility, energy storage, and distributed power generation. Worldwide government initiatives are accelerating the momentum, offering subsidies and policy incentives to adopt greener technologies. Tightening emission regulations are making hydrogen solutions increasingly attractive across transportation, power generation, and heavy industry. Liquefied hydrogen storage is gaining strong traction in these fast-evolving applications, setting the stage for long-term, sustainable energy solutions that align with global climate targets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 9.7% |

The industrial sector accounted for a dominant 63.8% share in 2024 as sectors like chemicals, refineries, and high-heat manufacturing integrate hydrogen to phase out fossil-based fuels. Liquefied hydrogen remains the preferred choice due to its higher energy density, making it ideal for large-scale storage and high-efficiency operations. The growing need for high-capacity, long-range energy storage is also making liquefied hydrogen a game-changer for transportation systems focused on zero-emission performance. Its ability to deliver extended energy outputs within compact storage frameworks is critical as industries tackle space and efficiency constraints. As the expansion of intermittent renewable energy sources accelerates, hydrogen's role in balancing supply and demand is becoming even more vital to ensuring grid stability.

The United States Liquefied Hydrogen Storage Market reached USD 446.7 million in 2024, fueled by robust investment in hydrogen infrastructure, especially in fueling stations and large storage projects. Advanced manufacturing capabilities and the growing electric and hydrogen vehicle industries are propelling demand. Federal initiatives, including those led by the Department of Energy, are aggressively supporting R&D efforts to enhance storage scalability and reliability for the future.

To stay competitive, companies like FuelCell Energy, Cockerill Jingli, ITM Power, SSE, Air Products and Chemicals, ENGIE, Linde, McPhy Energy, Air Liquide, Gravitricity, GKN, and Nel are doubling down on innovation and strategic partnerships. Key strategies include expanding production capacities, advancing cryogenic insulation technologies, investing in long-term research, and forming collaborative ventures to fast-track deployment and product diversification. Active participation in government-backed programs is also helping these players secure funding and build early-mover advantages across emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trade administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034, (USD Million)

- 5.1 Key trends

- 5.2 Industrial

- 5.3 Transportation

- 5.4 Stationary

- 5.5 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034, (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Netherlands

- 6.3.6 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

Chapter 7 Company Profiles

- 7.1 Air Liquide

- 7.2 Air Products and Chemicals

- 7.3 Cockerill Jingli

- 7.4 ENGIE

- 7.5 FuelCell Energy

- 7.6 GKN

- 7.7 Gravitricity

- 7.8 ITM Power

- 7.9 Linde

- 7.10 McPhy Energy

- 7.11 Nel

- 7.12 SSE